Your situation

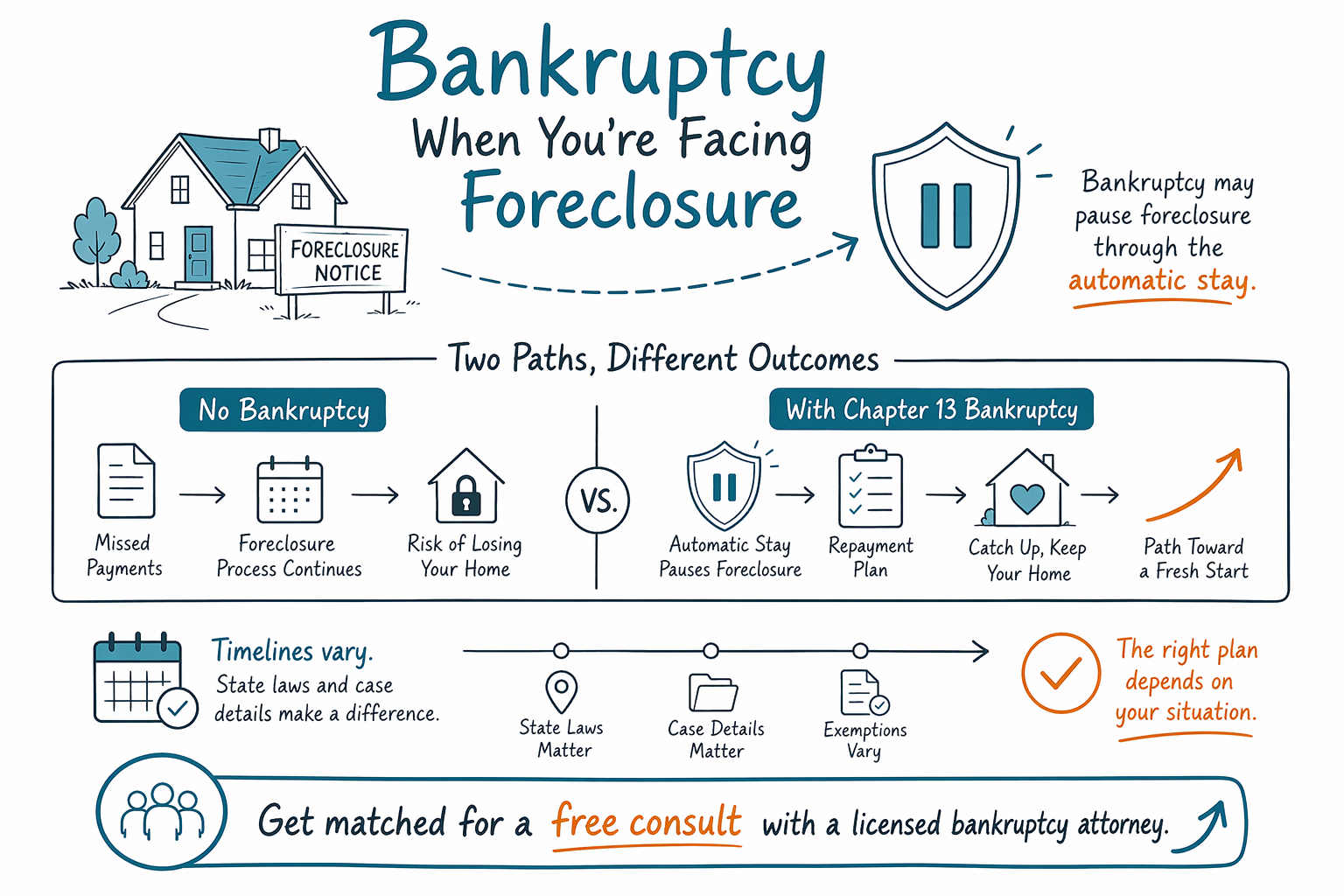

Bankruptcy When You're Facing Foreclosure

Facing foreclosure can feel terrifying, but there may be options. This page explains how bankruptcy can sometimes pause foreclosure and how to get matched for a free consult with a licensed attorney near you.

If you’re facing foreclosure, act quickly—but you’re not out of options

Foreclosure timelines can move fast, and the next notice you receive may matter. Still, you don’t have to figure this out alone.

At a high level, bankruptcy is sometimes used to pause foreclosure and create a path to catch up, keep the home, or move on with less chaos. What’s possible depends on your state, your court district, and your exact mortgage situation.

CleanSlate Match is a FREE matching service. We connect you with a licensed bankruptcy attorney near you for an educational consultation—but we do not file bankruptcy and we are not your lawyer.

How bankruptcy can affect foreclosure (the “automatic stay” in plain terms)

When someone files a bankruptcy case, an automatic stay usually goes into effect. The stay is a legal pause that can stop many collection actions, including most foreclosure activity and some related lawsuits.

That pause can create time—time to review the mortgage, understand your options, and work with an attorney on the right chapter. It does not automatically solve everything. Some debts and situations may still proceed depending on timing and specific facts.

Rules about the stay and foreclosure vary by case history and location. A licensed bankruptcy attorney can tell you what’s realistic in your situation.

Chapter 13 vs. Chapter 7 when foreclosure is involved

Chapter 7 is often about discharging certain unsecured debts. It may or may not help you keep a home, because it usually doesn’t “restructure” ongoing mortgage payments the way Chapter 13 can.

Chapter 13 commonly helps people facing foreclosure because it can set up a court-approved repayment plan. In many cases, a Chapter 13 plan can allow you to catch up on certain arrears over time while continuing ongoing mortgage payments.

This is general education. Your mortgage type, your arrears amount, whether you already have a judgment, and how your state treats exemptions and foreclosure procedures all affect the best path. See Chapters and the basics for a clearer overview.

What to ask a foreclosure-focused bankruptcy attorney (questions that bring clarity)

A good first consultation should help you understand (1) whether bankruptcy could pause the foreclosure in your specific case, and (2) what chapter makes sense. It should also be honest about limits.

Use these questions to guide your conversation:

- Has foreclosure already reached a stage where bankruptcy may not pause it?

- Will the automatic stay likely apply in my case, and are there any reasons it could be limited?

- If I file Chapter 13, what would a typical repayment plan require, and would it include the mortgage arrears?

- What debts usually survive bankruptcy, especially related to the home or past-due amounts?

- What documents should I gather for the meeting (without sending sensitive account details to anyone not representing you)?

- What is your fee structure, and what court and credit-counseling fees are expected?

If you want a calmer starting point, you can begin with the Get matched flow so a licensed attorney can explain your options for your state.

Costs and process: what it usually looks like (no surprises, no promises)

Most consumer bankruptcy attorneys charge a flat fee for the work of filing, plus the required court filing fee and a small required credit-counseling fee. The all-in total depends on the chapter (Chapter 7 vs. Chapter 13), the complexity of your case, and your court district.

As a broad planning guide, many people see attorney fees that can fall roughly in the low thousands to several thousand dollars, plus court costs. These ranges are not quotes and can vary. Ask the attorney to clearly explain what the fee covers and what additional costs may apply.

Also, remember: outcomes are not guaranteed. Bankruptcy may pause foreclosure and may help create a repayment plan, but it does not guarantee you will keep the home in every case, and it does not erase every type of debt.

Common questions people ask when foreclosure is scheduled

It’s normal to have the same worries you’re carrying right now. Here are clear, honest answers to common questions.

- “Will bankruptcy stop my foreclosure sale right away?” In many cases, a bankruptcy filing can trigger the automatic stay and pause many foreclosure actions. Timing, your case history, and your location matter.

- “Will it wipe out my mortgage?” Usually, bankruptcy does not simply “erase” a mortgage. The mortgage generally continues under its own terms, and catch-up depends on whether you use Chapter 13, your situation, and court rules.

- “What debts usually survive?” Many types of obligations often survive bankruptcy, including most student loans, recent income taxes, child support/alimony, many court fines/penalties, and debts connected to fraud or similar conduct. Your foreclosure-related arrears and other home-related costs are case-specific.

- “What if I’m being sued by the lender or have notices from the court?” An attorney can help you understand whether filing will pause the lawsuit or how to respond. Do not ignore court deadlines.

If you’re unsure what’s happening next, the safest move is to speak with a licensed bankruptcy attorney. Start with situations to find the most relevant help topic, then get matched for a free consultation.

Bankruptcy may pause foreclosure through the automatic stay—especially with Chapter 13—but the details are state- and case-specific, so get matched for a free consult with a licensed bankruptcy attorney.

Common questions

I have a foreclosure sale date. Should I wait or file immediately?

Because foreclosure deadlines can move quickly, it’s important to talk to a licensed bankruptcy attorney as soon as possible. In many situations, filing can trigger the automatic stay and pause foreclosure, but it depends on your specific facts and local rules.

Does Chapter 13 always let people keep their home?

Not always. Chapter 13 may help you catch up on mortgage arrears through a repayment plan, but keeping the home depends on eligibility, your budget, mortgage details, and what you qualify to do in your district. An attorney can explain your realistic options.

Will bankruptcy erase my mortgage balance or stop the lender from collecting?

Bankruptcy usually does not “erase” a mortgage in the simple way people hope for. The mortgage typically continues, and how arrears are handled depends on the chapter and your case. Some other related debts may also survive.

What information should I share to get matched and schedule a consult?

To protect your privacy, you generally only need contact info and a general description of your situation and preferred language. Do not send Social Security numbers, bank-account numbers, or credit-card details. A licensed attorney will tell you what documentation is needed.

How can I confirm I’m speaking with a licensed bankruptcy attorney?

Before you hire anyone, confirm their bar license status through your state’s attorney licensing resources and ask about their experience with consumer bankruptcy and cases in your federal court district.

Related help

How filing can stop a garnishment quickly and protect your paycheck.

Open → Bankruptcy When You're Buried in Medical DebtHow bankruptcy treats medical bills and why it's one of the most common reasons people file.

Open → Bankruptcy When You're Being Sued for a DebtHow the automatic stay can pause a debt lawsuit and what to do if you've been served.

Open →