Guides

The Bankruptcy Means Test

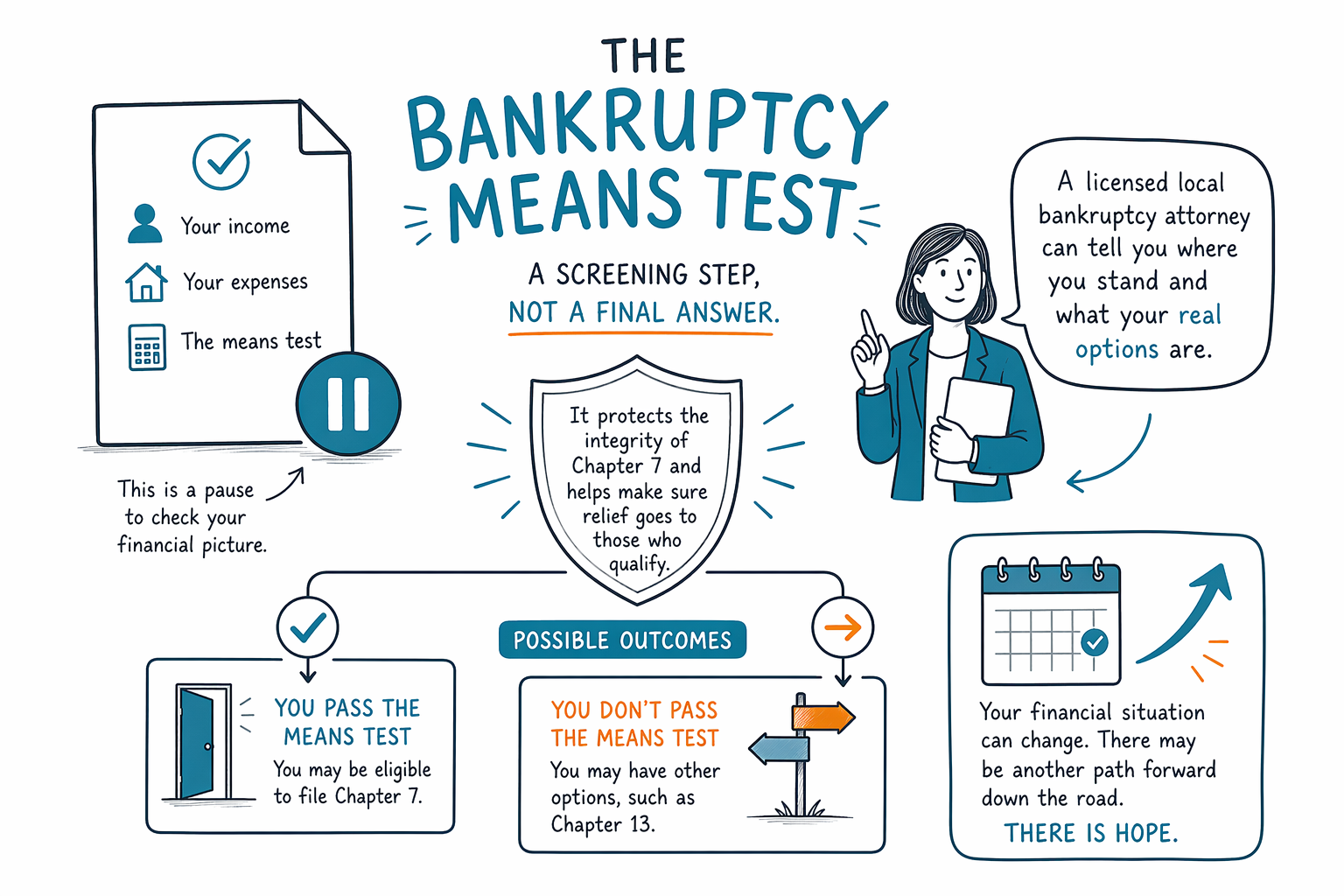

The means test is the main screening tool for Chapter 7. It compares your income to your state’s median and looks at certain allowed expenses, but it does not decide your whole case by itself.

What the bankruptcy means test is

If you are thinking about bankruptcy, the means test is the part that asks a basic question: does your income look low enough for Chapter 7, or do you need a closer review? In simple terms, it compares your income to the median income for a household of your size in your state.

If your income is below that median, many people pass this first part of the test. If it is above, that does not automatically mean you cannot file bankruptcy. It usually means there is a second step that looks at certain allowed living expenses and other factors.

This is one reason the means test feels confusing. It is not just “what you earn” or “what you owe.” It uses legal formulas, time periods, and expense categories that may not match your real monthly life exactly. The rules also vary by state and judicial district and can change over time, so only a licensed bankruptcy attorney in your area can tell you how the test applies to your case.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We do not file bankruptcy. We help connect you with a licensed bankruptcy attorney near you for a real case review.

What the means test does — and does not do

The means test mainly helps decide whether Chapter 7 is available. Chapter 7 is the type of consumer bankruptcy that can erase many unsecured debts, such as credit card debt and many medical bills, if you qualify and if those debts are dischargeable.

But the means test does not decide every part of your case. It does not tell you which property you can keep, whether a creditor will object, whether Chapter 13 may be better for you, or whether a specific debt will be erased. It also does not replace legal advice.

It is also important to be honest about what bankruptcy cannot usually erase. Some debts often survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts caused by fraud. Outcomes depend on the facts of the individual case.

If you are not sure whether Chapter 7 or Chapter 13 fits your situation, start with our bankruptcy services overview or learn about the chapters.

How the means test works in plain English

The test usually starts by looking at your "current monthly income," which is based on a set period before filing, not just what you are making today. For many people, that means recent changes matter. A job loss, reduced hours, overtime, bonuses, or seasonal work can change the picture.

Then your income is compared with the median income for your state and household size. If you are under the median, that is often a strong sign you may qualify for Chapter 7. If you are over, the second part of the test may subtract certain allowed expenses to see whether there is enough disposable income left to raise a legal concern about filing Chapter 7.

Those allowed expenses are not simply your actual bills. Some are based on government standards. Others depend on facts such as secured debts, priority debts, or family size. This is why two people with similar pay can get different results.

A licensed bankruptcy attorney can review timing, household size, income sources, and deductions carefully. Small details can matter a great deal.

Who the means test may affect most

The means test matters most for people looking at Chapter 7. If your income is low, irregular, or recently changed, the test may be especially important. It also matters if your household has multiple earners, self-employment income, overtime, commission income, or support from others.

If you do not appear to qualify for Chapter 7, that does not mean you have no option. Chapter 13 may still help. Chapter 13 uses a repayment plan, often three to five years, and can help people catch up on mortgage arrears, deal with car payments, or protect property that might be at risk in Chapter 7.

For some people, bankruptcy is not the only path. Other debt-relief options may exist depending on the type of debt, lawsuits, garnishments, and whether you are behind on a home or car. A local licensed attorney can explain the tradeoffs clearly and tell you what is realistic in your state.

If wage garnishment, a foreclosure sale, or collection lawsuits are adding pressure, speak with a lawyer quickly. Once a bankruptcy case is filed, the automatic stay usually pauses most collections, garnishments, foreclosures, and lawsuits right away, but timing and exceptions matter.

Common means test mistakes to avoid

A very common mistake is guessing. People often assume they earn too much for Chapter 7, or they assume they qualify because they feel broke. The legal test is more specific than that, and feelings alone do not answer it.

Another mistake is filing too fast or waiting too long without understanding timing. Because the test looks back at a set period, the month you file can matter. Recent overtime, a bonus, a layoff, or a second job can change the result.

People also get in trouble by using internet checklists that are too simple, by counting the household the wrong way, or by leaving out important facts. Full and honest information matters. So does using a lawyer who handles consumer bankruptcy regularly in your area.

A few good steps can help:

1. Gather recent pay information and a simple list of your debts.

2. Write down changes in income, job status, family size, or major expenses.

3. Ask how your state’s median-income figures and local rules apply.

4. Confirm the attorney is licensed in your state and in good standing with the state bar.

5. Get matched for a consultation through CleanSlate Match, free.

- Do not rely on a rough online guess alone.

- Do not hide income or transfers of property.

- Do not assume above-median income means "no bankruptcy."

What it may cost to get help

CleanSlate Match is free for the person looking for help. We collect only contact information and general intent, such as your name, phone, optional email, state, preferred language, and a basic description of what is going on. We do not ask for a Social Security number, bank-account numbers, credit-card numbers, or detailed account balances.

If you hire a lawyer, most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. For Chapter 7, attorney flat fees often fall around $1,000 to $2,500, and the court filing fee is commonly a few hundred dollars. For Chapter 13, attorney flat fees are often higher, sometimes around $3,000 to $6,000 or more depending on the district and complexity, plus the court filing fee and course fees. These are general ranges, not quotes.

What drives cost up or down? Your chapter, your state and district, whether you own a home, whether you have a business, how many creditors you have, whether your income is irregular, whether there are lawsuits or garnishments, and whether your case may involve disputes about property or dischargeability.

Ask for the total expected cost in writing, what the flat fee covers, what filing and course fees are extra, and whether any part of the fee can be paid over time where allowed. Then compare that information carefully with your options.

The means test is a screening step for Chapter 7, not a final answer, and a licensed local bankruptcy attorney can tell you where you stand and what your real options are.

Common questions

If I make too much money, am I automatically denied bankruptcy?

No. Higher income may mean a closer means-test review or that Chapter 13 should be considered instead of Chapter 7. A licensed bankruptcy attorney can tell you how the rules apply in your state and district.

Does passing the means test mean all my debts will be erased?

No. The means test is only one part of a bankruptcy case. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud.

Can the means test help stop garnishment or foreclosure?

The means test itself does not stop collection. Filing a bankruptcy case usually triggers the automatic stay, which pauses most garnishments, foreclosures, lawsuits, and collection actions, but timing and exceptions matter.

What information do I need to get matched?

Usually just your name, phone, optional email, state, preferred language, and a general description of your situation. CleanSlate Match is a free matching service, not a law firm, and we do not ask for Social Security numbers or bank or credit-card account numbers.

Should I talk to a lawyer even if I think I do not qualify for Chapter 7?

Yes. Many people assume the wrong thing about the means test. A local licensed bankruptcy attorney can review Chapter 7, Chapter 13, and other debt-relief options and explain what is realistic for your case.

Related help

Filing bankruptcy triggers the automatic stay, which can pause a foreclosure — here is how that works and which chapter helps you keep your home.

Open → Stopping Wage Garnishment & Bank LeviesBankruptcy's automatic stop can halt wage garnishment and bank levies — here is what happens and how fast.

Open → Debt Relief OptionsBankruptcy isn't the only path — here is an honest look at the main debt-relief options and when bankruptcy is the right fit.

Open →