Guides

Stopping Foreclosure With Bankruptcy

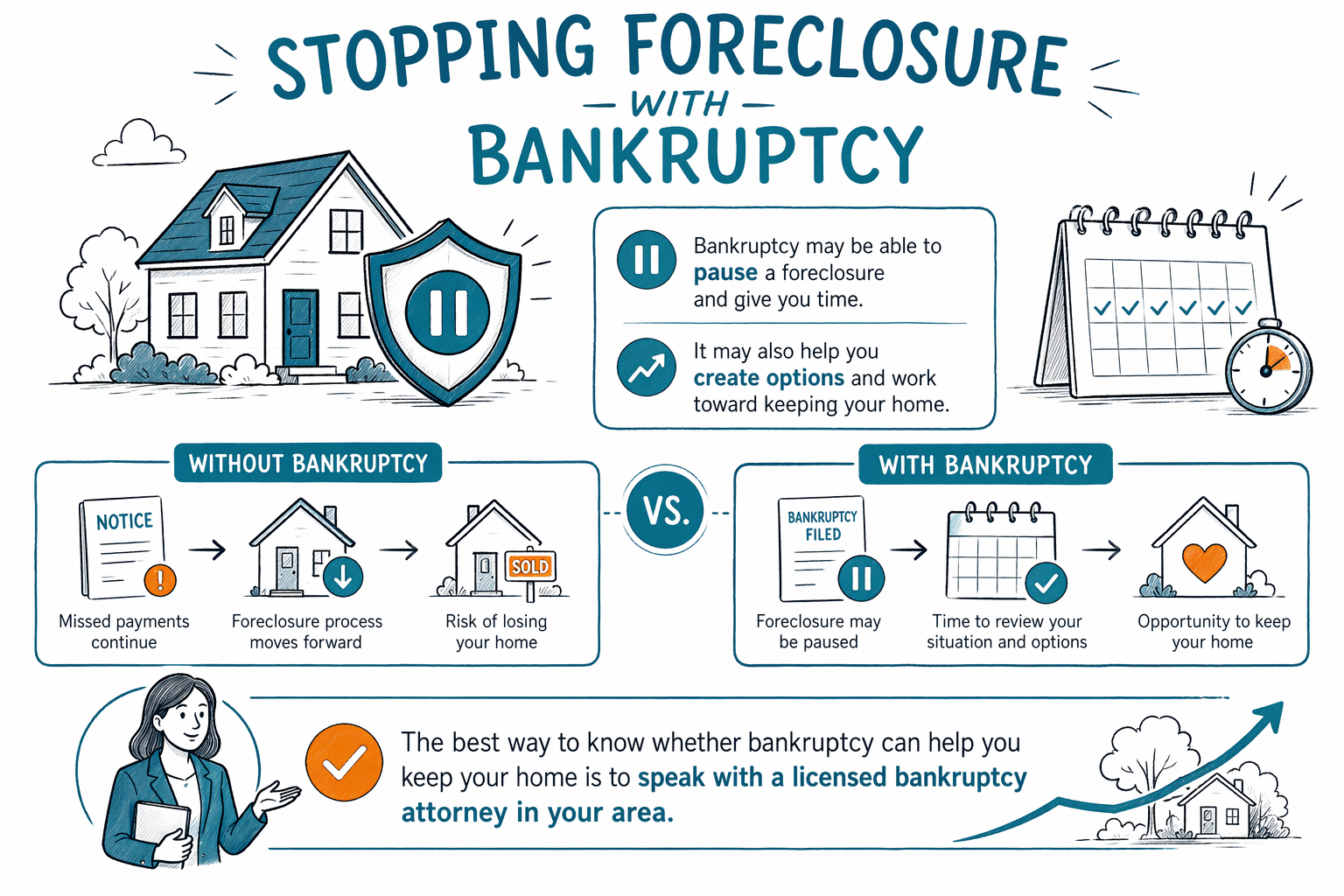

If a foreclosure sale is getting close, bankruptcy may be able to pause it through the automatic stay. Here is the plain-language version of how that works, what it can and cannot do, and how to get help fast.

How bankruptcy can stop a foreclosure

When a bankruptcy case is filed, a legal protection called the automatic stay usually starts right away. In many cases, that stay pauses most collection actions, including a pending foreclosure, wage garnishment, collection lawsuits, and collection calls.

That pause can give you breathing room. It may stop a scheduled foreclosure sale while the court case moves forward. But bankruptcy is not a magic reset button, and it does not automatically make missed mortgage payments disappear.

What happens next depends on which chapter is filed, how far along the foreclosure is, whether you want to keep the home, and the rules in your state and court district. Bankruptcy law, exemptions, and local procedures vary by state and district, so a licensed bankruptcy attorney in your area should review the timing and the facts of your case.

Chapter 7 vs. Chapter 13 if you are behind on your mortgage

For many people, the key question is whether Chapter 7 or Chapter 13 is the better fit. You can learn more about both in our chapters overview, but here is the short version.

Chapter 7 is often used when a person cannot afford the home long-term, wants time to stop the sale and plan the next step, or needs relief from other debts such as credit cards and medical bills. Chapter 7 may pause the foreclosure for a time, but it usually does not give you a structured way to catch up on missed mortgage payments over several years. If you are far behind and want to keep the home, Chapter 7 is often not the long-term foreclosure solution.

Chapter 13 is often the chapter people look at when they want to keep their home and catch up over time. In many cases, it lets a person repay mortgage arrears through a 3- to 5-year repayment plan while keeping up with current mortgage payments going forward. Many people keep their home and car through exemptions or a Chapter 13 plan, but success depends on having enough income to support the plan and on the details of the case.

Neither chapter guarantees that you will keep your home. If payments are not affordable, if deadlines are missed, or if the lender asks the court for permission to continue foreclosure, the stay may end. A local bankruptcy attorney can explain what is realistic in your district.

What bankruptcy does not do

It is important to be honest here: bankruptcy can pause a foreclosure, but it does not erase the mortgage lien on your home just because a case was filed. If you want to keep the house, you usually must deal with the missed payments and any ongoing payments in a way the law and the court allow.

Bankruptcy also does not erase every kind of debt. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. Outcomes depend on the individual case.

Also, timing matters. If a foreclosure sale already happened, bankruptcy may not undo it. And if someone has filed bankruptcy cases before, the automatic stay may be limited or may not go into effect the same way. These are reasons to speak with a licensed bankruptcy attorney as early as possible, not the night before a sale if you can avoid it.

Who this option may fit

Bankruptcy may be worth discussing if you are behind on your mortgage and also dealing with other debt problems, such as credit cards, medical bills, a lawsuit, or wage garnishment. Sometimes reducing pressure from other debts makes it possible to focus on the home.

It may also fit if you need a fast legal pause while you review your options, especially if a foreclosure sale date has been set. Chapter 13 is often discussed when a person has regular income and wants a structured way to catch up on missed payments.

It may be a poor fit if the home is far beyond what you can realistically afford, if there is no income to support future payments, or if another option would meet your goal better. Depending on the situation, people may also look at non-bankruptcy services or simply use bankruptcy to create an orderly exit rather than keep the property.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We give general educational information only and can help you get connected with a licensed bankruptcy attorney near you.

Common mistakes people make before a foreclosure filing

People under stress often wait too long because they feel embarrassed, hope the problem will somehow fix itself, or are afraid to ask questions in English. You are not alone. But foreclosure deadlines are real, and waiting can shrink your options.

Other common mistakes include ignoring court papers, assuming Chapter 7 and Chapter 13 do the same thing, borrowing retirement money too quickly, transferring property to family, or paying one creditor while falling further behind on the mortgage. Actions like these can create new problems in a bankruptcy case.

If you are trying to save your home, do not guess. A local attorney can look at the sale date, the mortgage history, any prior filings, and your full debt picture. If you want help finding someone, you can get matched for free.

- Gather your foreclosure notices and any court papers.

- Write down your sale date, if one has been scheduled.

- Make a simple list of your debts and monthly bills.

- Ask whether Chapter 13, Chapter 7, or another option seems most realistic.

- Confirm that the attorney is licensed in your state.

- Do not send Social Security numbers or bank account numbers through our matching form.

- We only need contact details and a general sense of your situation and preferred language.

What bankruptcy usually costs in foreclosure cases

Attorney fees in consumer bankruptcy are often charged as a flat fee, plus the court filing fee and a small required credit-counseling course fee. The real cost depends on the chapter, the complexity of the case, and the court district. These are general ranges, not quotes.

For Chapter 7, many consumer cases fall around $1,000 to $2,500 in attorney flat fees, plus the court filing fee, which is commonly a few hundred dollars, and a small credit-counseling fee. Cases involving urgent foreclosure timing, prior bankruptcy filings, business issues, or disputed property questions may cost more.

For Chapter 13, attorney flat fees are often higher, commonly about $3,000 to $6,500 or more depending on the district and complexity, plus the court filing fee and the small course fee. In some districts, part of the attorney fee may be paid through the Chapter 13 plan, but the structure varies by court and lawyer.

Ask for a clear written explanation of the fee, what services are included, what court costs are separate, and what might raise the price. CleanSlate Match is free to use for people seeking help. Participating attorneys pay a flat fee to take part, and it is always free for you to get matched.

Bankruptcy may be able to pause a foreclosure and give you time, but the best way to know whether it can help you keep your home is to speak with a licensed bankruptcy attorney in your area.

Common questions

Will filing bankruptcy definitely stop the foreclosure sale?

It often pauses a foreclosure right away through the automatic stay, but not in every situation and not forever. Prior cases, timing, and local court rules can affect what happens, so a licensed bankruptcy attorney should review your case quickly.

Which chapter is better if I want to keep my home?

Many people look to Chapter 13 when they want time to catch up on missed mortgage payments through a repayment plan. Chapter 7 may pause the sale, but it usually does not give a long-term way to cure mortgage arrears.

Can bankruptcy erase my mortgage?

Usually no. Bankruptcy may help with the debt pressure around the mortgage and may pause foreclosure, but it does not simply make the mortgage lien vanish because you filed a case.

Can bankruptcy erase all my other debts too?

No. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud. The result depends on the facts of the case.

How fast should I talk to a lawyer if I got a foreclosure notice?

As soon as you can. The earlier you get legal advice from a licensed bankruptcy attorney, the more options you may have.

What does CleanSlate Match do?

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We collect basic contact information, your state, preferred language, and a general sense of the problem so we can help connect you with a licensed bankruptcy attorney near you.

Related help

The means test decides whether you qualify for Chapter 7 — here is how it compares your income to your state's median, in plain language.

Open → Stopping Wage Garnishment & Bank LeviesBankruptcy's automatic stop can halt wage garnishment and bank levies — here is what happens and how fast.

Open → Debt Relief OptionsBankruptcy isn't the only path — here is an honest look at the main debt-relief options and when bankruptcy is the right fit.

Open →