Guides

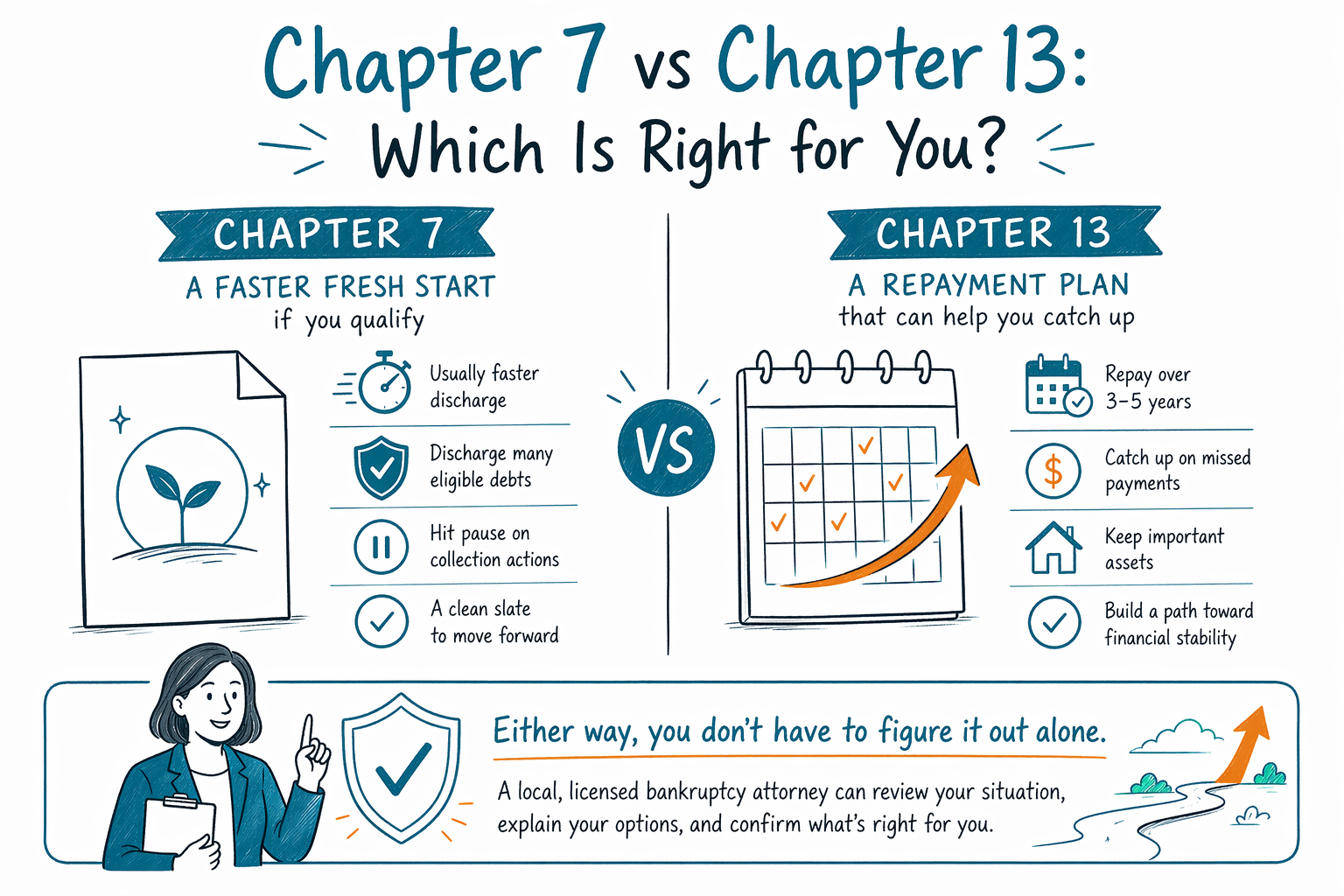

Chapter 7 vs Chapter 13: Which Is Right for You?

Feeling overwhelmed is normal—choosing between Chapter 7 and Chapter 13 is a common next step. This guide explains the difference in plain terms and how a licensed bankruptcy attorney helps you decide.

The honest answer first: there isn’t one “best” chapter

Chapter 7 and Chapter 13 are two different ways the court handles consumer debt. Which one fits you depends on your income, your debts, your goals (like keeping a home or car), and rules in your state and bankruptcy court.

Because bankruptcy rules and exemptions vary, this is general education—not legal advice. A licensed bankruptcy attorney can review your situation and explain realistic outcomes in your area. (CleanSlate Match is a free matching service, not a law firm and not your lawyer.)

Chapter 7 (often called “fresh start”)—how it usually works

Chapter 7 is commonly used when a person’s income is low enough that they may qualify, and they want to discharge (erase) certain eligible debts.

In many Chapter 7 cases, eligible property is protected by exemptions—meaning you may be able to keep key assets depending on what you own and your state’s exemption rules. Some debts typically do not go away in Chapter 7 (for example, most student loans, many recent income taxes, child support/alimony, many fines, and debts tied to fraud).

Whether you qualify can depend on the means test and other eligibility requirements. These rules vary by state and judicial district and can change over time, so confirm details with a licensed bankruptcy attorney.

Chapter 13 (often called “repayment plan”)—how it usually works

Chapter 13 is a court-approved payment plan, usually spread over 3 to 5 years, based on your income and allowed expenses. Instead of asking the court to discharge right away, Chapter 13 can reorganize certain debts and let you make payments through the plan.

This chapter is often considered when people need more time to catch up on things like past-due mortgage or car payments, or when they have disposable income that the law requires them to use for repayment. In many situations, people can keep property by staying in the plan.

Like Chapter 7, some debts usually survive bankruptcy (for example, many taxes, student loans, child support/alimony, and debts involving fraud). The exact outcome depends on the specific debt and your individual case.

A practical comparison: which situation points toward which chapter

Many people compare chapters by focusing on goals:

- If your main goal is a faster reset and you may qualify for Chapter 7, Chapter 7 is often discussed first.

- If your main goal is to catch up on missed payments, protect your home or car through a plan, or your income makes Chapter 7 harder, Chapter 13 is often considered.

- If you’re facing foreclosure, wage garnishment, or a lawsuit, filing can trigger an automatic stay in most cases—this can pause many collection actions while the case proceeds. Your attorney will explain what the stay does in your specific situation.

Because rules vary by state and bankruptcy court district, the “right” chapter is not the same for everyone.

Means test and eligibility: why your income matters

Chapter 7 eligibility commonly involves a means test and other requirements. The means test is not a simple “amount of money” rule—it uses calculations that can include your income type, household situation, and allowed expenses. Those calculations can differ depending on your district and the facts of your case.

Chapter 13 has its own eligibility requirements, including limits on certain debts and the ability to make plan payments. Your attorney will look at your income, expenses, debts, and timing (for example, whether a foreclosure sale is scheduled) and then explain which chapter is likely to fit.

This is one reason it’s important to talk to a licensed bankruptcy attorney rather than choosing based on online comparisons alone.

What bankruptcy can and can’t erase (so you’re not misled)

Bankruptcy can help you with many types of consumer debt, but it does not erase every obligation. Common debts that often survive include:

- Student loans (usually difficult to discharge; outcomes depend on the case)

- Most recent income taxes (often not dischargeable)

- Child support and alimony

- Many court fees/fines

- Debts tied to fraud or certain misconduct

If you have specific debts, your attorney will review each one. The goal is clarity: you should understand what may be discharged, what may be restructured, and what usually remains.

Rules and outcomes vary by state and district, and the details depend on your situation—so confirm everything with a licensed bankruptcy attorney.

Chapter 7 is often for a faster fresh start if you qualify, while Chapter 13 is a repayment plan that can help you catch up—either way, a local licensed bankruptcy attorney should confirm what applies to your state and debts.

Common questions

If I file Chapter 7, will my mortgage and credit cards be erased?

Sometimes credit card debt and certain other unsecured debts may be discharged in Chapter 7, but your mortgage depends on whether you’re behind and what options are available in your case. Some debts typically survive bankruptcy (like most student loans and many recent taxes). A licensed bankruptcy attorney can tell you what is likely in your specific situation.

Does Chapter 13 stop foreclosure or wage garnishment?

In many cases, once a bankruptcy case is filed, an automatic stay pauses many collection actions, including foreclosure activity and wage garnishment, while the court reviews the case. However, the stay can vary based on prior filings, timing, and the facts of your case—so confirm details with a licensed bankruptcy attorney.

How does a lawyer help me decide between the two chapters?

A lawyer reviews your debts, income, expenses, property, and goals, then explains eligibility, likely outcomes, and how exemptions may help you keep assets. They can also confirm what each chapter can and can’t do in your specific district. CleanSlate Match is a free matching service, not a law firm.

Are the rules the same everywhere in the United States?

No. Bankruptcy rules, exemptions, and how courts apply them vary by state and judicial district, and they can change over time. The best next step is to speak with a licensed bankruptcy attorney in your area.

Related help

Which debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open → The Automatic Stay: How Bankruptcy Stops CollectionsHow filing instantly pauses garnishment, foreclosure, lawsuits, and collection calls.

Open →