Guides

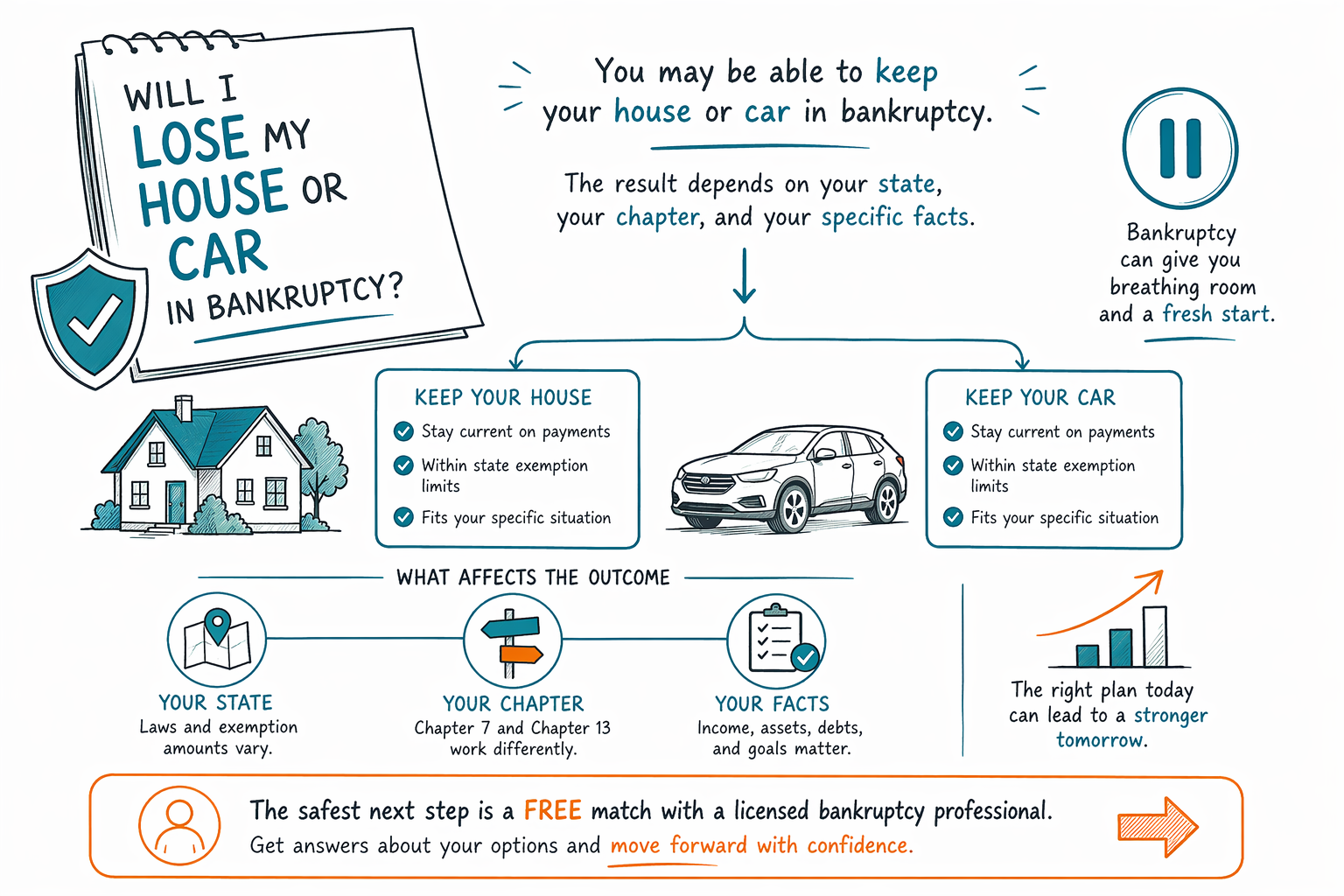

Will I Lose My House or Car in Bankruptcy?

Many people keep their home or car in bankruptcy. Whether you can depends on your state, the chapter you file, and your specific situation — and a licensed attorney in your area can explain the options clearly.

The short answer

You do not automatically lose your house or car just because you file bankruptcy. In many cases, people protect a home, a car, or both using exemptions, payment plans, or the right chapter.

What happens next depends on where you live, whether you file Chapter 7 or Chapter 13, and how much equity you have in the property. Bankruptcy laws and exemption rules vary by state and by federal court district, so there is no single rule that fits everyone.

If you are behind on payments, bankruptcy can sometimes pause a foreclosure or repossession right away through the automatic stay. That pause is real help — but it is not a guarantee that you can keep the property forever. A lawyer can tell you what your local rules allow.

- Bankruptcy does not mean “lose everything.”

- State and district rules matter a lot.

- The automatic stay can stop collection action quickly, but only while the case is active and only if the court allows it.

How Chapter 7 can affect a home or car

Chapter 7 is often called a “liquidation” case, but that does not mean every person loses property. Many filers keep exempt property, and in some cases a house or car can be protected if the equity is covered by an exemption.

If a mortgage or car loan is still owed, you usually must stay current if you want to keep the property. If payments are far behind, the lender may still be able to move forward after bankruptcy protections change or end.

Chapter 7 can also involve a choice: keep the car and continue paying, or surrender it and deal with the remaining loan balance as allowed by law. The details vary widely by state and by the facts of the case.

- Exemptions may protect some or all equity.

- Keeping the property usually means keeping up with payments.

- If the loan is more than the property is worth, the options can be different.

How Chapter 13 can help protect property

Chapter 13 is a repayment plan. For many people, it is the chapter that gives them the best chance to keep a home when they are behind on payments, because it can spread missed payments over time while they keep making the regular monthly payment.

It can also help with a car loan by letting you catch up over time, and in some situations it may help lower the practical pressure of a repossession or foreclosure. That said, you must be able to make the plan payments, and the court will review whether the plan is workable.

If you are trying to save a house or car, Chapter 13 is often worth discussing with a bankruptcy attorney. Learn more about the chapters.

- It may help you catch up on missed house or car payments.

- It is a plan, so regular payments matter.

- It is not automatic — the plan has to work under the local rules.

What bankruptcy usually does not erase

It helps to be honest about limits. Bankruptcy can help with many debts, but it usually does not erase everything.

Some debts often survive, including most student loans, recent income taxes, child support and alimony, many court fines, and debts tied to fraud. A secured debt, like a mortgage or car loan, is also different from a credit card balance because the lender may still have rights in the property.

That is why the question is not only “Will I lose my house or car?” but also “What debts do I have, what is secured, and what protections apply where I live?” A licensed attorney can walk through that with you in plain language.

- Most student loans usually survive.

- Recent taxes often survive.

- Child support, alimony, fines, and fraud-related debts are often not wiped out.

What to expect before you file

You do not need to figure this out alone. A bankruptcy attorney can look at your home, car, payment status, and local exemption rules and explain whether Chapter 7 or Chapter 13 may fit better.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We collect only basic contact information and general intent — like your state, your preferred language, and whether you are worried about foreclosure, a car, wage garnishment, or other debt. We do not ask for Social Security numbers, bank numbers, or credit-card numbers.

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The exact cost depends on the chapter, the district, and how complex the case is, so any range you hear is not a quote. If you want a licensed attorney near you, you can get matched.

- Bring a list of your debts and property, if you have it.

- Ask whether your state uses federal or state exemptions.

- Always confirm the attorney’s bar license in your state.

You may be able to keep your house or car in bankruptcy, but the result depends on your state, your chapter, and your specific facts — so the safest next step is a free match with a licensed bankruptcy attorney near you.

Common questions

Can bankruptcy stop a foreclosure or repossession right away?

Often, yes — filing can trigger the automatic stay, which pauses most collections, foreclosure steps, repossession efforts, and lawsuits. But the stay is not a permanent guarantee, and the lender may ask the court for permission to continue in some cases.

If I am behind on my mortgage or car payment, will I definitely lose it?

No, not definitely. Many people keep their home or car, especially when exemptions, Chapter 13, or continued payments make that possible. The answer depends on your state, your equity, and how far behind you are.

Should I file Chapter 7 or Chapter 13 if I want to keep my home?

There is no one best answer for everyone. Chapter 13 is often more helpful for catching up on missed payments, but Chapter 7 may still work in some situations if your equity is protected and you can stay current.

Does CleanSlate Match decide whether I keep my house or car?

No. CleanSlate Match is a free matching service, not a law firm, and we do not give legal advice. We connect you with a licensed bankruptcy attorney near you who can review your situation and explain your options.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → The Automatic Stay: How Bankruptcy Stops CollectionsHow filing instantly pauses garnishment, foreclosure, lawsuits, and collection calls.

Open →