Guides

The Automatic Stay: How Bankruptcy Stops Collections

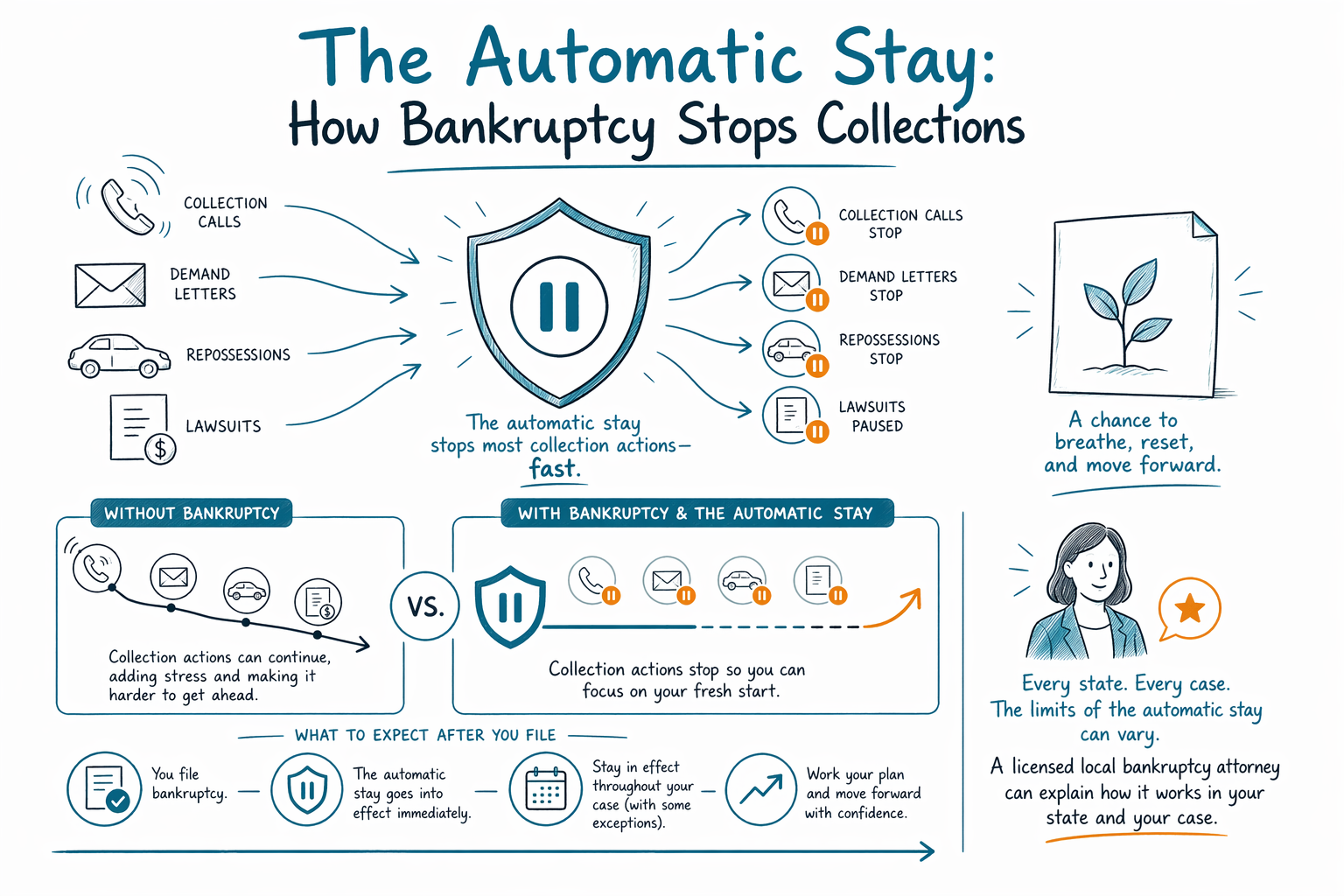

Filing bankruptcy can create an automatic stay, which usually stops most collection actions right away. It can pause wage garnishment, foreclosure, lawsuits, and collection calls, but there are important limits.

What the automatic stay does

The automatic stay is a court protection that usually begins the moment a bankruptcy case is filed. In many cases, it tells most creditors to stop trying to collect from you while the case is pending.

That can include stopping collection calls and letters, pausing many lawsuits, stopping most wage garnishments going forward, and delaying or stopping a foreclosure or repossession. For many people, this is the first real breathing room they have had in a long time.

But the stay is not magic, and it is not forever. It does not mean every debt disappears. It is a pause that gives the court and your attorney time to deal with your situation under Chapter 7 or Chapter 13. You can learn more about the two main consumer chapters at chapters.

What it usually stops right away

If the stay applies in your case, it often stops many common collection actions as soon as the case is filed with the court. Timing matters. If a paycheck was already processed or a sheriff's sale already happened before filing, the stay may not undo what already happened.

Common actions the automatic stay often pauses include:

- collection calls, letters, and many other collection efforts

- most wage garnishments going forward

- many debt collection lawsuits

- many bank levies or account freezes, depending on timing and local practice

- foreclosure actions and scheduled sales

- vehicle repossessions, if the car has not already been sold

- utility shutoffs in some situations, for at least a limited time

The exact effect can depend on the facts, the timing, and where you live. Bankruptcy rules, local court procedures, and exemption laws vary by state and judicial district, so a licensed bankruptcy attorney in your area is the right person to confirm what the stay will and will not stop in your case.

What the automatic stay does not always stop

Some debts and actions are treated differently. The automatic stay has real limits, and it is important to know them so you are not misled.

It often does not stop or fully stop certain family court matters, criminal cases, or efforts to collect debts that usually survive bankruptcy. For example, child support and alimony obligations are treated differently and often continue. Some tax matters can also continue. If a creditor asks the court for permission, the court may also lift the stay in some situations.

Just as important, bankruptcy does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts related to fraud. Whether a debt is discharged depends on the type of debt, the facts of the case, and sometimes whether a creditor objects.

This is one reason it helps to speak with a licensed bankruptcy attorney before filing. A lawyer can explain not only what may stop right away, but also what may still be owed later.

How it works in Chapter 7 and Chapter 13

Both Chapter 7 and Chapter 13 usually create an automatic stay when the case is filed. The difference is what comes next.

In Chapter 7, the stay can give you short-term relief while the court process moves forward. Chapter 7 is often used when a person cannot realistically repay unsecured debt like credit cards or medical bills, but it does not give everyone a way to catch up on missed mortgage or car payments over time.

In Chapter 13, the stay can be especially helpful for people trying to save a home or car. Chapter 13 involves a repayment plan, often lasting three to five years, that may let someone catch up on arrears over time while keeping property they want to keep.

Many people do keep their home or car in bankruptcy, often through exemptions, reaffirmation or redemption options in some Chapter 7 cases, or a Chapter 13 plan. But outcomes depend on income, equity, missed payments, loan terms, and local rules. If you want a broader overview first, start with our guides.

Important exceptions and repeat-filing limits

If you filed bankruptcy before, the automatic stay may be limited or may not last as long in a new case. In some repeat filings, it may stop after a short time unless the court extends it. In other situations, it may not go into effect at all unless the court allows it.

Also, secured creditors sometimes ask the court to lift the stay. This can happen if payments are far behind, insurance is missing, or the property is not protected by the bankruptcy process. If the court grants that request, the creditor may be allowed to continue foreclosure, repossession, or another action.

This is why speed matters when there is a sale date, eviction issue, garnishment, or repossession risk. The sooner you speak with a licensed attorney, the more clearly you can understand your options and timing.

Getting help: what to expect and what it may cost

CleanSlate Match is a free matching service, not a law firm, not a lawyer, and not your legal representative. We do not file bankruptcy cases and using our service does not create an attorney-client relationship. We help connect people with a licensed bankruptcy attorney near them.

If you choose to speak with an attorney, most consumer bankruptcy lawyers charge a flat fee, plus the court filing fee and a small required credit-counseling fee. These are general ranges, not quotes. In many areas, Chapter 7 attorney flat fees often range from about $1,000 to $2,500, plus a court filing fee that is usually a few hundred dollars and a small counseling fee. Chapter 13 attorney flat fees are often higher, sometimes around $3,000 to $6,000 or more depending on the district, with a court filing fee and counseling fee as well. The real cost depends on the chapter, your state and district, and how simple or complex the case is.

Costs can go up if there are lawsuits, business issues, nonexempt property, recent transfers, tax questions, multiple parcels of real estate, or disputes about income or fraud. A local attorney can tell you what applies in your situation.

If you want to get connected, get matched. We only need basic contact and general intent information, such as your name, phone number, optional email, state, preferred language, and a simple description of what is happening. We do not ask for a Social Security number, bank account numbers, or credit card numbers through the matching form. When you speak with any attorney, you can also confirm that the lawyer is licensed with your state bar.

The automatic stay can give you fast relief from many collection actions, but it has limits, and a licensed local bankruptcy attorney can tell you how it works in your state and your case.

Common questions

Does bankruptcy stop wage garnishment immediately?

Often, yes. In many cases the automatic stay stops most wage garnishments going forward as soon as the case is filed, but money already taken may not be returned, and timing matters.

Can the automatic stay stop a foreclosure sale?

It often can if the bankruptcy case is filed before the sale happens. But the lender may later ask the court to lift the stay, and the best long-term option may depend on whether Chapter 7 or Chapter 13 fits your situation.

Will collection calls and lawsuits stop too?

Usually, most creditors must stop collection calls, letters, and many lawsuits once the automatic stay is in effect. If contacts continue after filing, tell your attorney right away.

Does the automatic stay erase my debt?

No. The automatic stay is a pause, not a debt eraser. Also, some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud.

What if I filed bankruptcy before?

The stay may be limited in a repeat filing. In some cases it lasts only a short time or does not start automatically, so it is very important to speak with a licensed bankruptcy attorney quickly.

Is CleanSlate Match my lawyer?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We provide general educational information and can help connect you with a licensed bankruptcy attorney near you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →