Guides

What Debt Bankruptcy Can and Can't Erase

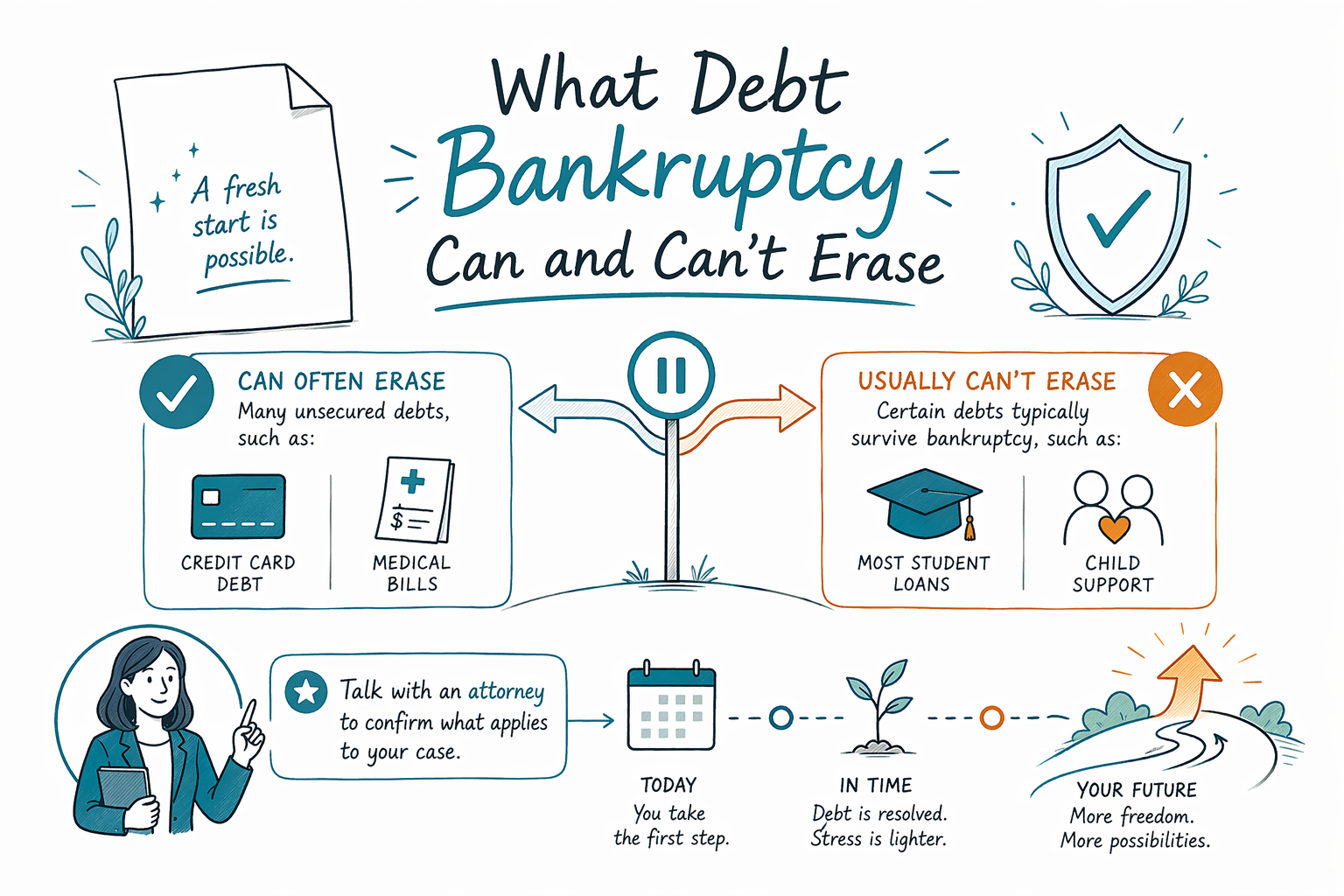

Bankruptcy can give many people a fresh start, but it doesn’t erase every type of debt. Below is a clear, plain list of what often gets wiped out and what usually survives—so you can plan realistically.

The direct answer: what bankruptcy can’t promise to erase

Bankruptcy outcomes depend on your exact debts, your income, your state, and your court. A licensed bankruptcy attorney can review your situation and explain what is likely to be discharged in your area.

As a general rule, bankruptcy may eliminate many “consumer debts” (like many credit cards and many medical bills), but some debts usually survive even after filing. Also, some debts are dischargeable but only if they’re handled correctly in the case.

Important: CleanSlate Match is a FREE matching service—not a law firm and not a lawyer. We provide general education and help you get connected with a licensed bankruptcy attorney near you, but we can’t tell you what your specific case will do.

Debts that are often erased in consumer bankruptcy (Chapter 7 or Chapter 13)

Many people file to stop pressure from bills that are unsecured and not tied to special legal exceptions. In many cases, bankruptcy helps most with debts like:

- Credit card debt

- Medical bills

- Personal loans

- Many past-due utility bills

- Some collection balances from these types of debts

Even when a debt is the “kind” bankruptcy often helps with, it can still be affected by details (for example, if a creditor argues a debt fits an exception, or if you miss required steps). That’s why an attorney review matters.

Debts that commonly survive bankruptcy (or often survive)

Some debts are treated differently under federal law and usually cannot be erased through a consumer bankruptcy. Common examples include:

- Most student loans (even though there are limited, specific exceptions—an attorney can explain whether any apply)

- Child support and alimony

- Most recent income tax debts that don’t meet legal “age” and other requirements

- Court fines, criminal penalties, and certain restitution orders

- Debts from fraud or willful wrongdoing (and other “non-dischargeable” categories)

Because rules vary, some debts may be partially addressed in a plan or may require special motions. But it’s safest to assume these categories may survive.

Why the “can it be erased?” answer depends on Chapter 7 vs. Chapter 13

Chapter 7 and Chapter 13 are both bankruptcy, but they work differently.

1) Chapter 7 is often used when someone’s income is low enough and they need relief from unsecured debt. Depending on your state’s rules and exemptions, you may be able to keep certain property.

2) Chapter 13 is a repayment plan. It may allow you to catch up on certain debts (like mortgage arrears) over time while keeping other property. The plan can also help address some unsecured debts, depending on the math of your case and the plan rules.

In both chapters, whether a particular debt is erased depends on the debt type and the legal exceptions that apply. And remember: rules vary by state and federal judicial district.

The “rules vary” reminder (state + district differences that affect outcomes)

Bankruptcy law is federal, but key parts of the process can vary—especially exemptions (what property you can keep), local procedures, and how courts apply certain details.

For example, exemption options can differ dramatically by state, which may affect what happens to assets. Local court rules can also affect timelines and what paperwork is required.

That’s why the best next step is to talk with a licensed bankruptcy attorney in your state (and ideally in your district) and confirm what your specific debts are likely to do.

What to do next: confirm what your debts are likely to do, and what it will cost

A good first consultation usually focuses on: (1) what type of debts you have, (2) whether Chapter 7 or Chapter 13 fits your situation, (3) whether any key debts may survive, and (4) what you can keep and what collection activity might pause.

- Gather basic information about your debts (debt type names are helpful; no account numbers are needed).

- Ask which debts are likely to be discharged and which ones are likely to survive.

- Ask whether any creditor could claim an exception (for example, fraud-related claims).

- Ask what chapter your attorney recommends and why.

About cost: most consumer bankruptcy attorneys charge a FLAT-FEE, plus the required court filing fee and a small required credit-counseling fee. Total attorney costs can vary based on the chapter (Chapter 7 vs. Chapter 13), the complexity of your case, and the district. Ranges are often offered, but they are not quotes—only an attorney review can confirm your likely range. CleanSlate Match does not charge you and does not take a share of attorney fees or your debt.

If you want, you can get matched with a licensed bankruptcy attorney for a consultation near you—free to you—through get-matched. Be sure they are licensed in your state; you can confirm their bar status.

Bankruptcy can often erase many credit card and medical debts, but some debts—like most student loans and child support—usually survive, so you’ll want an attorney to confirm what applies to your case.

Common questions

Will bankruptcy wipe out my credit cards and medical bills?

Often, many credit card and medical debts can be discharged, but not always. Exact outcomes depend on your chapter, your income, how the debts are categorized, and any exceptions a creditor may claim.

What debts usually survive bankruptcy even if I file?

Common examples include most student loans, child support/alimony, many court fines or restitution, and certain tax debts that don’t meet legal discharge rules. Fraud-related debts can also be non-dischargeable. Your attorney can review your list and tell you what’s likely in your case.

Does filing bankruptcy stop collections and foreclosure right away?

In many cases, once a bankruptcy case is filed, the automatic stay can pause many collections, lawsuits, wage garnishments, and foreclosure actions. The details can depend on your situation and prior filings, so confirm with a licensed attorney.

How much does a bankruptcy consultation and case usually cost?

Many consumer bankruptcy attorneys charge a flat-fee, plus the court filing fee and a small required credit-counseling fee. The total can vary by chapter and complexity, and ranges are not guarantees—only an attorney review can confirm likely costs.

Are the rules the same in every state and court?

No. While bankruptcy is federal, exemptions and some procedures vary by state and federal judicial district. That’s why it matters to speak with a licensed bankruptcy attorney in your area.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open → The Automatic Stay: How Bankruptcy Stops CollectionsHow filing instantly pauses garnishment, foreclosure, lawsuits, and collection calls.

Open →