Chapter 7 vs 13

Chapter 7 Bankruptcy

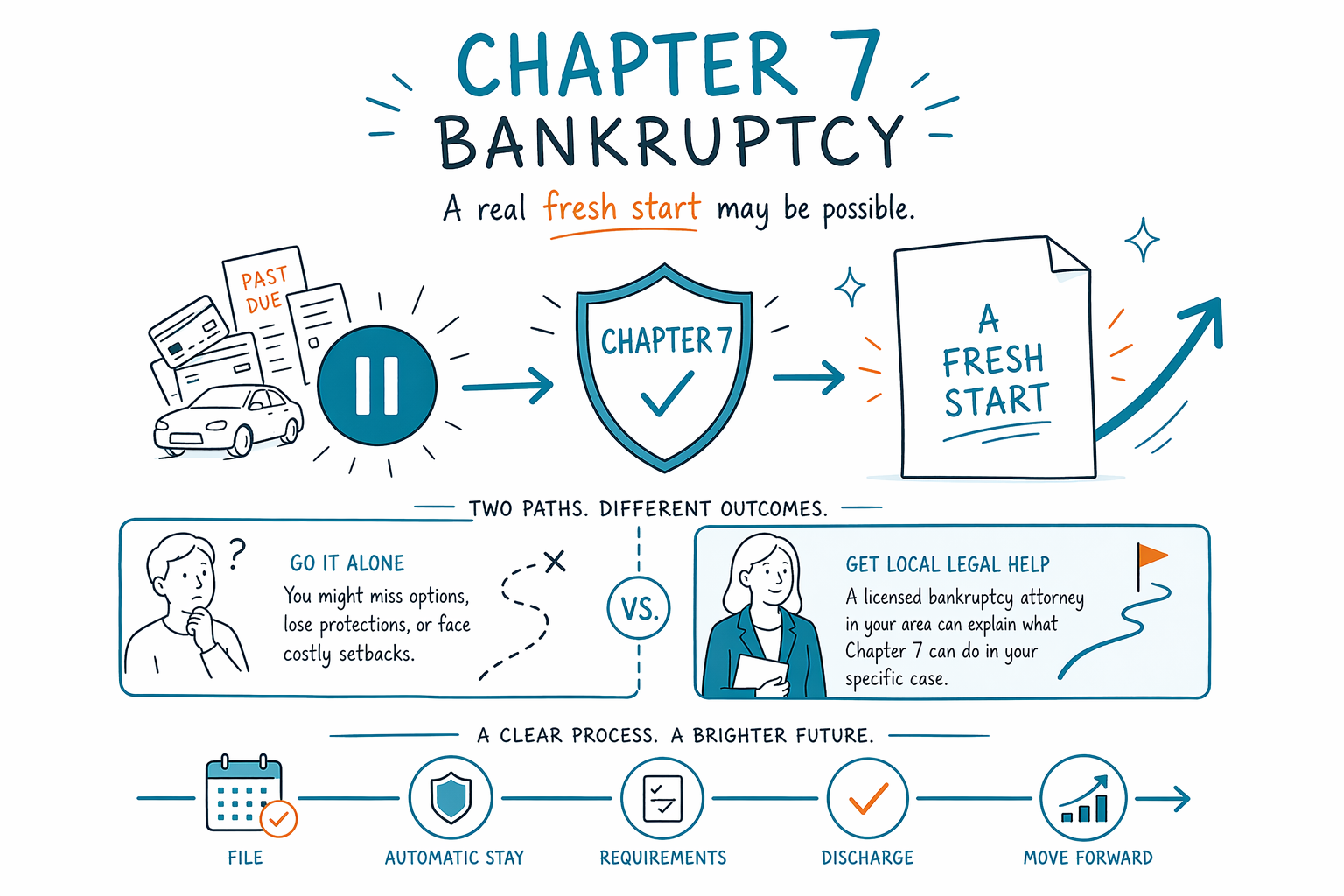

Chapter 7 is often called a “fresh start” bankruptcy because it can erase many unsecured debts in a few months. It does not erase every debt, and the rules depend on your state, your income, and your specific case.

What Chapter 7 does — and what it does not do

Chapter 7 is a type of consumer bankruptcy for people who cannot realistically pay their debts. In many cases, it can discharge unsecured debts such as credit cards, medical bills, personal loans, old utility bills, and some lawsuit debts. For many people, the process is faster than Chapter 13, often lasting a few months from filing to discharge.

One important protection is the automatic stay. In most cases, the moment a bankruptcy case is filed, the automatic stay stops most collection calls, wage garnishments, lawsuits, bank levies, and foreclosure actions. That breathing room can matter a lot when you feel cornered.

But Chapter 7 does not erase everything. Some debts usually survive, including most student loans, recent income taxes, child support, alimony, most court fines, and debts caused by fraud. Bankruptcy also does not magically make secured debt disappear if you want to keep the property tied to it. If you want to keep a home or car, you usually must stay current or make arrangements allowed by law.

This page is general educational information only. Bankruptcy law, exemptions, local practice, and eligibility rules vary by state and judicial district, so a licensed bankruptcy attorney in your area should review the facts of your case.

Who Chapter 7 may fit

Chapter 7 may fit someone with heavy unsecured debt and little realistic ability to repay it. It is often considered by people dealing with job loss, medical debt, a divorce, reduced hours, collection lawsuits, or wage garnishment. If you have few assets and your income is below certain limits, Chapter 7 may be a better fit than a repayment plan.

To qualify, many people must pass the means test. This is a formula that compares your household income and certain allowed expenses to legal standards. In simple terms, the means test is meant to see whether you have enough disposable income to repay creditors through Chapter 13 instead. Passing or failing is not always obvious from a quick internet search. Household size, income timing, expenses, and local rules can change the answer.

If you are behind on a mortgage or car loan and need time to catch up, Chapter 7 may not solve that problem by itself. It can delay foreclosure or repossession through the automatic stay, but it usually does not create a long-term payment plan to catch up. In those situations, Chapter 13 may sometimes be the better tool. You can learn more at Chapters.

A licensed bankruptcy attorney can look at your income, assets, debts, and goals and explain whether Chapter 7 is likely to fit, or whether another option may make more sense.

What you may be able to keep

Many people are surprised to learn that filing Chapter 7 does not automatically mean losing everything. Bankruptcy exemptions protect certain property up to limits set by law. Depending on your state and the facts of your case, exemptions may protect things like clothing, household goods, retirement accounts, part or all of the equity in a car, tools used for work, and sometimes equity in a home.

What you can keep depends on where you live, what property you own, how much equity you have, and whether your state requires you to use state exemptions or allows federal exemptions. That is why one person's case can look very different from another person's case, even if both are filing Chapter 7.

If property is not fully protected by exemptions, a Chapter 7 trustee may have the power to sell it and use the value for creditors. That possibility is why honest legal advice matters before filing. A careful attorney will review your assets first and explain any risk clearly.

Many people do keep their home or car, especially when the equity is protected and payments are manageable. But that result is never automatic, and no one should promise it without reviewing the case.

How Chapter 7 works, step by step

The process is more structured than many people expect. A case usually begins with a review of your debts, income, assets, recent financial history, and whether Chapter 7 is available. You also must complete a short required credit-counseling course from an approved provider before filing.

- Speak with a licensed bankruptcy attorney about your goals, debts, income, and property.

- Complete the required pre-filing credit-counseling course.

- Your attorney prepares and files the bankruptcy papers with the court.

- The automatic stay begins immediately in most cases when the case is filed.

- You attend a short hearing called the 341 meeting, where the trustee asks basic questions under oath.

- You complete a second required debtor-education course.

- If there are no major problems, the court may enter a discharge order a few months after filing.

A Chapter 7 case is a court process, so details matter. Transfers of property, use of credit cards before filing, tax refunds, lawsuits, inheritances, and co-owned property can all affect the outcome. That is one reason self-filing can be risky for some people.

CleanSlate Match is not a law firm, not a lawyer, and does not file bankruptcy. We are a free matching service that helps connect people with a licensed bankruptcy attorney near them. If you want to talk to someone, you can get matched for free.

Common mistakes to avoid

People under stress sometimes make fast decisions that hurt their case. It is common to cash out retirement funds, repay family members first, transfer a car title, run up credit cards, or ignore a lawsuit because they plan to file later. Those choices can create new problems.

Before filing, it is usually wise to pause and get legal guidance. A licensed bankruptcy attorney can explain what documents are needed, what property is protected, how the means test may apply, and whether timing matters. A few weeks can sometimes change the result, especially if income has recently gone down.

Here are common mistakes to avoid:

- Waiting too long after a garnishment or foreclosure notice arrives

- Hiding assets or leaving debts off the paperwork

- Paying back friends or family right before filing without legal advice

- Selling or giving away property for less than it is worth

- Taking new cash advances or using credit cards when you already plan to file

- Assuming student loans, taxes, or support debt will automatically go away

If you are meeting anyone about bankruptcy, confirm that the attorney is licensed in your state and ask who will actually handle your case. State rules and local court practice matter.

What Chapter 7 usually costs

Cost matters, especially when money is already tight. In many parts of the United States, consumer bankruptcy attorneys charge a flat fee for a Chapter 7 case rather than billing by the hour. On top of the attorney's fee, there is also a court filing fee and a small fee for the required credit-counseling and debtor-education courses.

A common Chapter 7 attorney flat-fee range is about $1,000 to $2,500 for a relatively straightforward case. The court filing fee is usually a few hundred dollars, and the required courses often add a small extra amount. These are general ranges, not quotes, and the real number depends on your district, the complexity of the case, whether there are business debts, real estate issues, tax issues, prior filings, lawsuits, or questions about assets or income.

Fees may be lower for a simple case and higher for a complicated one. If your case involves significant property, nonexempt assets, recent transfers, a pending foreclosure, self-employment records, or means-test disputes, the flat fee may go up. A good attorney should explain what is included in the fee and what might cost extra before you hire them. You can read more at Costs.

CleanSlate Match is always free for the person looking for help. We only collect contact information and general intent, such as your name, phone, optional email, state, preferred language, and a short description of your situation. We do not ask for a Social Security number, bank-account numbers, or credit-card numbers.

Chapter 7 may give you a real fresh start, but only a licensed bankruptcy attorney in your area can tell you what it can do in your specific case.

Common questions

Will Chapter 7 erase all my debt?

No. Chapter 7 can erase many unsecured debts, but some debts usually survive, including most student loans, recent income taxes, child support, alimony, most court fines, and debts from fraud. The result depends on the facts of your case.

How long does Chapter 7 take?

Many Chapter 7 cases finish in a few months, but timing varies by court and by case. Problems with paperwork, assets, income questions, or creditor disputes can make it take longer.

Can Chapter 7 stop a wage garnishment or foreclosure?

In most cases, yes, at least temporarily. When the case is filed, the automatic stay usually stops most garnishments, lawsuits, and foreclosure actions right away, but long-term results depend on your debts, property, and what chapter fits your situation.

Will I lose my home or car if I file Chapter 7?

Not always. Many people keep their home or car through exemptions and by staying current on secured payments, but it depends on equity, state exemption rules, and whether the payments are affordable.

How do I know if I pass the means test?

There is no safe way to guess from a simple rule of thumb. The means test depends on household size, income, allowed expenses, and local standards, so a licensed bankruptcy attorney should review it with you.

What does CleanSlate Match do?

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help connect you with a licensed bankruptcy attorney near you so you can get advice about your own case.