Your situation

Bankruptcy When You're Buried in Medical Debt

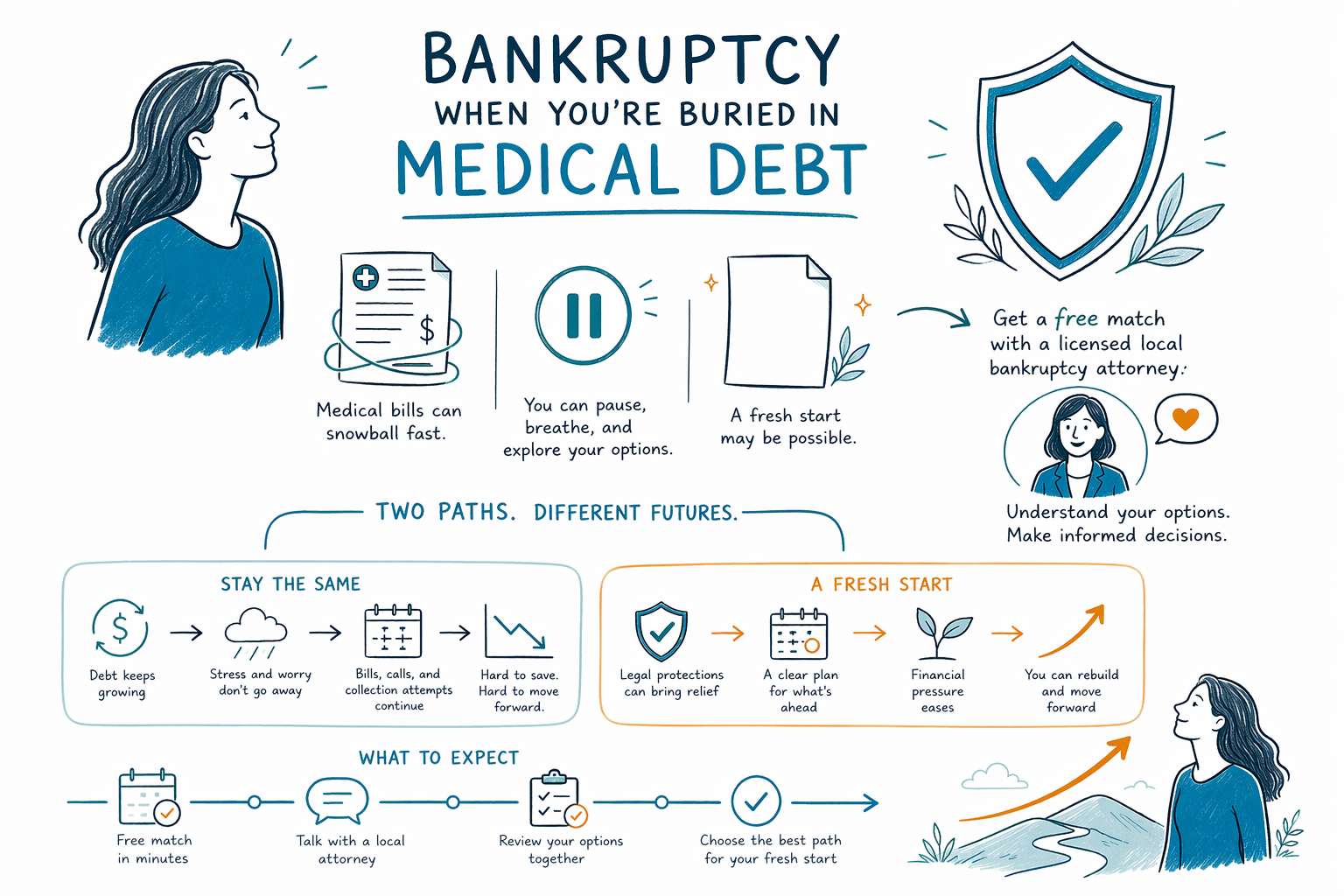

Medical bills can grow fast, even when you did everything right. If you're buried in hospital, doctor, ambulance, or insurance balance bills, bankruptcy may be one option to discuss with a licensed attorney near you.

Why medical debt pushes so many people to look at bankruptcy

Medical debt is different from many other debts because it often starts with something you did not plan for: an illness, injury, emergency room visit, surgery, pregnancy, or time away from work. Even people with insurance can end up owing large amounts after deductibles, copays, out-of-network charges, or denied claims.

When the bills keep coming, it can affect everything else. You may fall behind on credit cards, rent, a car payment, or a mortgage because you were trying to keep up with medical providers. For many people, the real problem is not just one hospital bill. It is the chain reaction that follows.

Bankruptcy does not mean you failed. It is a legal process that may help some people get relief from debts they cannot realistically repay. Medical debt is one of the most common reasons people start asking about chapters of bankruptcy and whether a fresh start is possible.

How bankruptcy usually treats medical bills

In many cases, ordinary medical bills are treated like unsecured debt. That means they are generally in the same broad category as many credit card balances or personal loans with no collateral attached. Depending on the chapter you qualify for and the facts of your case, medical debt may be discharged, paid in part through a plan, or handled in another way.

But it is important to be honest about limits. Bankruptcy does not erase every kind of debt, and no one can promise a result before reviewing your situation. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. Rules also vary by state and judicial district.

If your medical debt has already been sent to collections or included in a lawsuit, filing a bankruptcy case may trigger the automatic stay. The automatic stay usually pauses most collection actions, including many lawsuits, wage garnishments, and other collection efforts, as soon as a case is filed. A licensed bankruptcy attorney in your area can explain how that may apply in your case.

Chapter 7 vs. Chapter 13 for medical debt

Chapter 7 is often the chapter people ask about first. In a typical Chapter 7 case, a person who qualifies may be able to discharge many unsecured debts, including many medical bills, in a relatively short process. Whether you qualify can depend on the means test, your income, your household size, your assets, and the exemption laws in your state.

Chapter 13 works differently. Instead of seeking a quick discharge through Chapter 7, you propose a repayment plan, usually lasting three to five years. Chapter 13 may be helpful if you earn too much for Chapter 7, if you are behind on a mortgage or car loan, or if you need a structured way to catch up while still addressing medical debt.

Many people are surprised to learn that bankruptcy is not only about credit cards. If medical debt is the main reason you are drowning, either chapter may be worth discussing, depending on your full financial picture. A local lawyer can explain the difference in plain language and tell you what is realistic in your state.

- Chapter 7 may help some people discharge many medical bills if they qualify.

- Chapter 13 may help people repay part of what they owe over time while protecting a home or car.

- The right chapter depends on income, property, other debts, and state exemption rules.

What to do if medical bills are ruining your finances

If you are overwhelmed, try to slow the situation down and gather basic information. You do not need to solve everything in one day. A bankruptcy attorney will usually want a simple overview first, not a perfect file.

- Make a list of who is billing you: hospitals, doctors, collection agencies, and anyone suing you.

- Set aside recent letters, court papers, and collection notices in one place.

- Note any urgent deadlines, such as a court date, garnishment notice, or foreclosure issue connected to missed payments after medical problems.

- Write down the broad picture: whether you are working, whether your income dropped, and whether you are behind on rent, mortgage, car payments, or utilities.

- Ask whether bankruptcy is the only issue, or whether you may also need to discuss insurance disputes, payment plans, or other debt-relief options.

Do not ignore a lawsuit or garnishment notice because the debt is medical. Deadlines matter. A licensed bankruptcy attorney may be able to explain whether filing could stop or pause collection activity, but timing can be important.

How much does bankruptcy usually cost?

Cost matters, especially when the debt came from a health crisis. Most consumer bankruptcy attorneys charge a flat fee for a Chapter 7 or Chapter 13 case, plus the court's filing fee and a small required credit-counseling fee. The real amount depends on the chapter, the complexity of the case, and the district. These are general ranges, not quotes.

For many Chapter 7 cases, attorney flat fees often fall roughly in the range of about $1,000 to $2,500, plus the court filing fee and a small course fee. For many Chapter 13 cases, attorney fees are often higher, sometimes around $3,000 to $6,000 or more depending on local rules and complexity, plus the court filing fee and required course fees. Some Chapter 13 attorney fees may be paid in part through the plan, depending on the district and the case.

Fees may go up if your case involves a business, recent transfers of property, a high number of creditors, disputed debts, prior bankruptcy filings, nonexempt assets, or urgent litigation. A local attorney should explain the fee structure clearly before you hire them. Do not rely on a general online number as a promise.

How CleanSlate Match can help

CleanSlate Match is a free matching service. We are not a law firm, not a lawyer, and we do not file bankruptcy or create an attorney-client relationship. We provide general educational information and help connect people with a licensed bankruptcy attorney near them.

If you want, you can get matched for free. We only ask for contact information and general intent, such as your name, phone number, optional email, state, preferred language, and a simple description of what is going on. We do not ask for a Social Security number, bank-account numbers, credit-card numbers, or detailed financial account information.

When you speak with any attorney, ask whether they are licensed in your state and confirm their bar license. You can also look at our other debt situations and bankruptcy chapters to understand the basics before you decide what to do next.

If medical bills have turned into a financial crisis, you may have options, and a free match with a licensed local bankruptcy attorney can help you understand them clearly.

Common questions

Can bankruptcy get rid of medical bills?

Many medical bills are the kind of unsecured debt that may be discharged in bankruptcy, but no result is guaranteed. The outcome depends on your chapter, your overall case, and the rules in your state and district.

Will I lose my home or car if I file because of medical debt?

Not always. Many people keep their home and car through exemptions, current payments, or a Chapter 13 plan, but it depends on the facts of the case and state law.

Can bankruptcy stop collection calls or a lawsuit over hospital bills?

If a bankruptcy case is filed, the automatic stay usually stops most collection activity right away, including many lawsuits and garnishments. A local bankruptcy attorney can explain what that would likely mean in your situation.

Do I need to wait until all my medical treatment is finished before I talk to a lawyer?

No. If the bills are already unmanageable, it can make sense to talk with a licensed bankruptcy attorney sooner rather than later. Acting early may help you understand deadlines and options.

Is CleanSlate Match my lawyer?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We offer general educational information and help connect you with a licensed bankruptcy attorney near you.

Related help

How the automatic stay and Chapter 13 can pause foreclosure and help you keep your home.

Open → Bankruptcy When Your Wages Are Being GarnishedHow filing can stop a garnishment quickly and protect your paycheck.

Open → Bankruptcy When You're Being Sued for a DebtHow the automatic stay can pause a debt lawsuit and what to do if you've been served.

Open →