Your situation

Bankruptcy When Your Wages Are Being Garnished

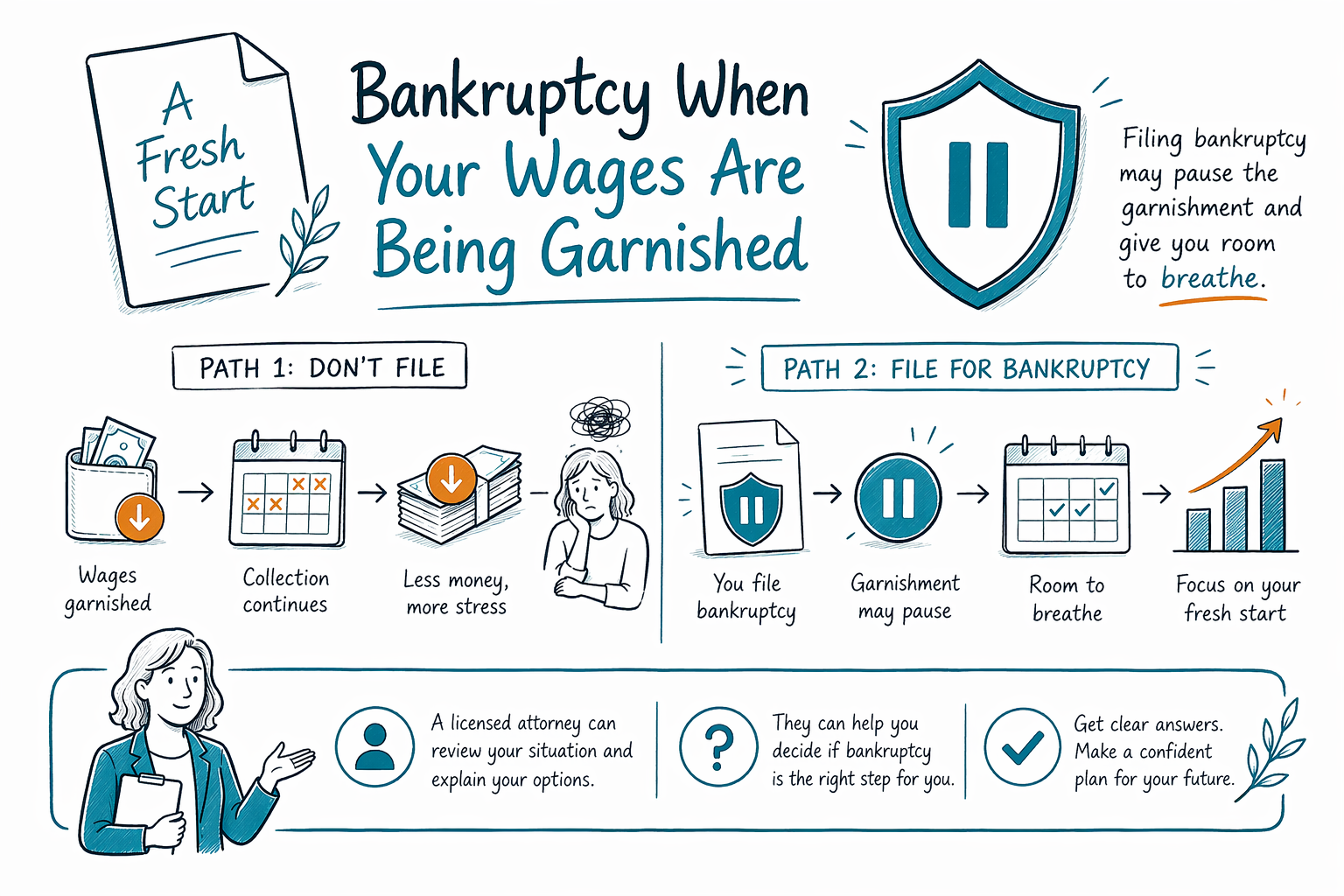

A wage garnishment can feel urgent and humiliating, but you still have options. Bankruptcy may stop the garnishment quickly in many cases, and a licensed attorney can help you understand what fits your situation.

What a wage garnishment means

A wage garnishment happens when money is taken from your paycheck because of a debt, usually after a court process. In some cases, the money is taken for other reasons, like child support, taxes, or student loans, which can follow different rules.

If your wages are being garnished, you may already be behind on bills, getting calls from collectors, or facing a lawsuit. That can be frightening, especially if you are new to the U.S. or unsure what the papers mean.

The important thing to know is this: you do not have to figure it out alone. Bankruptcy is one possible tool, but whether it helps depends on the type of debt, your state, and your overall finances.

How bankruptcy can help

When a bankruptcy case is filed, the automatic stay usually starts right away. That is a court order that pauses most collection efforts, including many garnishments, lawsuits, phone calls, and bank collection actions.

For many people, that pause can create breathing room fast. In some cases, the garnishment stops soon after the employer is notified of the filing. In other cases, there can be a short delay or extra steps, so it is important to speak with a licensed bankruptcy attorney as soon as possible.

Bankruptcy can also help if you are trying to catch up on other bills at the same time. Chapter 7 and Chapter 13 work differently, and the right choice depends on your income, property, debts, and goals. To compare them, see bankruptcy chapters.

What bankruptcy may not fix

Bankruptcy does not erase every debt. Some debts usually survive, such as most student loans, recent income taxes, child support and alimony, most court fines, and debts involving fraud. The exact result depends on the case and the law that applies where you live.

Also, not every garnishment is treated the same way. A garnishment for child support or certain taxes may be harder to stop or may continue in a different form. A wage garnishment tied to a lawsuit or credit card debt is often treated differently.

That is why general information can only go so far. Bankruptcy rules, exemptions, and local procedures vary by state and federal district, so you should confirm the details with a licensed attorney in your area.

What to do right now

If your paycheck is being taken, the next step is usually to get local legal guidance quickly. A bankruptcy attorney can review the kind of debt, check whether filing could stop the garnishment, and explain whether Chapter 7 or Chapter 13 may be more appropriate.

- Gather the papers you received about the garnishment, lawsuit, or debt.

- Write down which paycheck is affected and who is taking the money.

- Note any other urgent problems, like foreclosure, car repossession, or a lawsuit.

- Contact a licensed bankruptcy attorney in your state.

- If you want a simple place to start, use get matched to connect with a bankruptcy attorney near you.

CleanSlate Match is a free matching service, not a law firm, not a lawyer, and not your lawyer. We do not file bankruptcy for you. We simply help connect people with licensed bankruptcy attorneys.

What a bankruptcy attorney can explain

A licensed bankruptcy attorney can help you understand whether filing may stop the garnishment, what chapter might fit your situation, and whether you may be able to keep important property such as a car or home. They can also explain state exemptions and whether any plan or filing might fit your budget.

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The total cost varies based on the chapter, the complexity of the case, and the district. Any range you hear is not a quote, and you should confirm it directly with the attorney.

If you are worried about language, ask for an attorney or office that can communicate in your preferred language. You can also start by browsing situations to see other common debt problems people face.

If your wages are being garnished, filing bankruptcy may pause the collection and give you room to breathe, and a licensed attorney can tell you whether it is the right step for your situation.

Common questions

Will bankruptcy stop my wage garnishment right away?

Often, the automatic stay pauses most garnishments as soon as the case is filed, but timing and procedure vary. A local bankruptcy attorney can tell you what usually happens in your district and help move quickly.

Can bankruptcy remove all of the money already taken from my paycheck?

Not always. In some cases, money taken before the filing may not be recoverable, and results depend on the debt type and local law. An attorney can review the timing and explain your options.

Do I need to know my income or account balances to get started?

No. For matching, CleanSlate Match only asks for contact information and general information about your situation and preferred language. You do not need to provide a Social Security number, bank details, or account numbers.

Is CleanSlate Match a law firm?

No. CleanSlate Match is a free matching service that connects people with licensed bankruptcy attorneys. We are not a law firm and do not give legal advice or represent you.

Related help

How the automatic stay and Chapter 13 can pause foreclosure and help you keep your home.

Open → Bankruptcy When You're Buried in Medical DebtHow bankruptcy treats medical bills and why it's one of the most common reasons people file.

Open → Bankruptcy When You're Being Sued for a DebtHow the automatic stay can pause a debt lawsuit and what to do if you've been served.

Open →