Guides

What is credit counseling before bankruptcy?

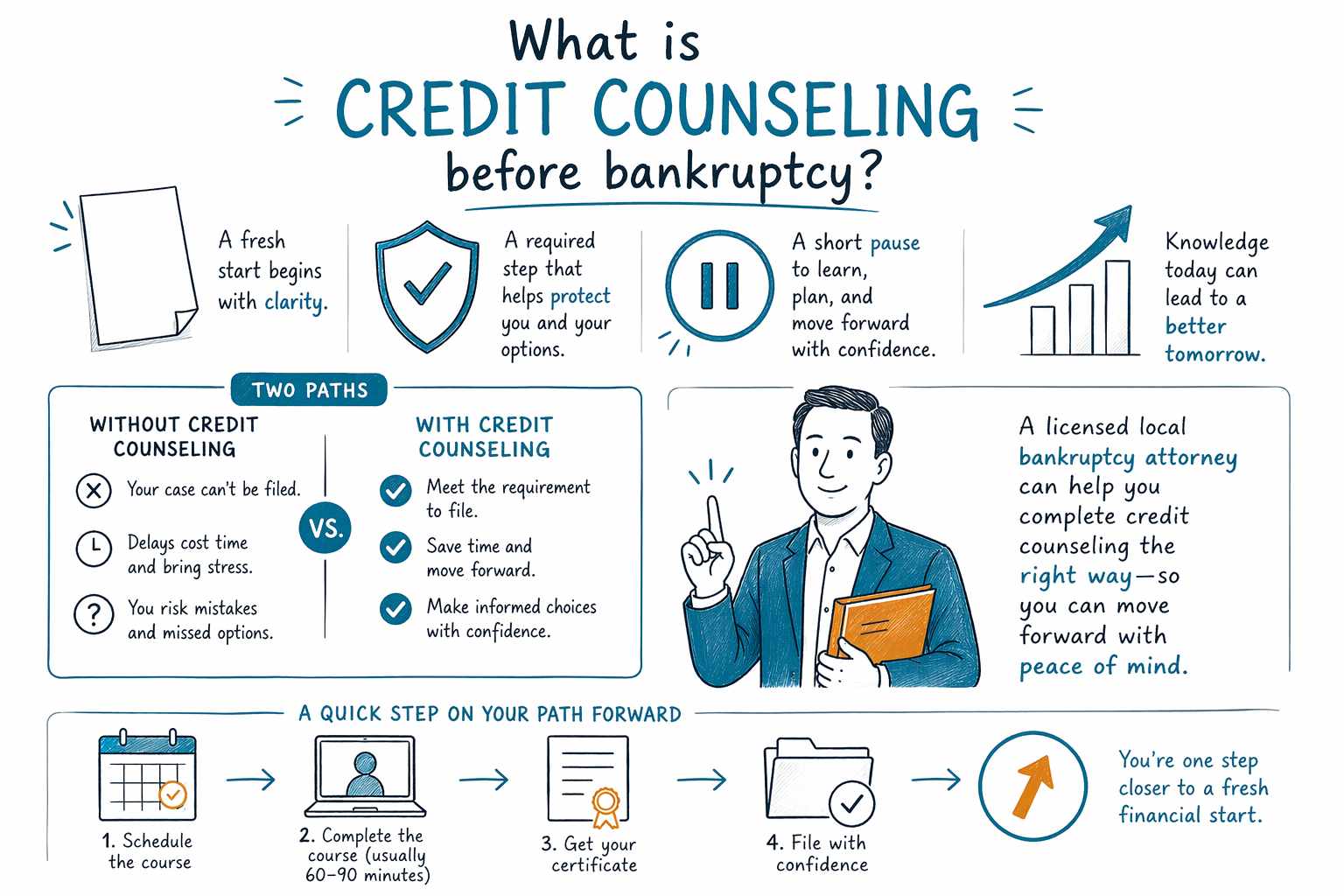

Credit counseling before bankruptcy is a short course most people must take from an approved provider before filing a consumer bankruptcy case. It is usually simple, done online or by phone, and meant to explain your options — not to judge you.

The short answer

In most consumer bankruptcy cases, you must complete a credit-counseling course from a provider approved by the U.S. Trustee Program before your case is filed. This applies to most Chapter 7 and Chapter 13 cases.

The course usually reviews your income, expenses, debts, and possible alternatives to bankruptcy. In many cases, it takes about 60 to 90 minutes and can be done online, by phone, or sometimes in person. After you finish, you receive a certificate that is usually filed with your bankruptcy paperwork.

This requirement is about education and process. It is not a test you “pass” or “fail,” and it does not mean the counselor is deciding whether you deserve help.

Why it matters before you file

The timing matters. In general, the course must be completed within the 180 days before your bankruptcy case is filed. If it is not done on time, the court may dismiss the case unless a limited exception applies.

That is one reason many people choose to speak with a licensed bankruptcy attorney before filing. A local attorney can tell you which approved providers are accepted in your district, how the certificate is handled, and whether anything unusual applies in your case. Bankruptcy rules and procedures vary by state and district.

If you are facing wage garnishment, a foreclosure, a repossession, or a lawsuit, timing can be especially important. The automatic stay usually starts when a bankruptcy case is filed and can pause most collections, garnishments, foreclosures, and lawsuits — but the case has to be properly filed first.

What happens during the course

The course is usually straightforward. The provider asks for basic information about your financial situation and reviews possible options, which may include budgeting, debt-management plans, or bankruptcy. For many people, it feels more like a required class than a deep counseling relationship.

The provider may suggest alternatives, but you are not required to choose a debt-management plan just because it is discussed. If bankruptcy still appears to be the realistic option, the course completion certificate is what matters for filing.

You should be careful about what information you share and with whom. CleanSlate Match only collects contact information and general intent — such as your name, phone number, optional email, state, preferred language, and a general description of your situation — so we can help connect you with a licensed bankruptcy attorney. We do not ask for Social Security numbers, bank-account numbers, credit-card numbers, or other financial-account details.

How much does credit counseling cost?

The pre-bankruptcy credit-counseling course usually has a small fee. Often, the cost is around $10 to $50, though the exact amount depends on the provider. Some approved providers offer fee waivers or reduced fees for people with low income.

If you hire a bankruptcy attorney, the counseling fee is separate from the attorney's fee and the court filing fee. Most consumer bankruptcy attorneys charge a flat fee, but the real amount depends on the chapter, the complexity of the case, and the district. As a general educational range, Chapter 7 attorney flat fees are often about $1,000 to $2,500, and Chapter 13 attorney flat fees are often about $3,000 to $6,000 or more, depending on the area and case complexity. Court filing fees are separate and are commonly a few hundred dollars. These are not quotes, and local prices may be lower or higher.

A licensed bankruptcy attorney in your area can explain the likely costs in your district and whether a payment arrangement may be available before filing. CleanSlate Match is a free matching service — not a law firm, not your lawyer, and not a bankruptcy filer — and it is always free for the person seeking help.

What credit counseling does not do

Credit counseling does not guarantee that your bankruptcy will be approved, and it does not decide what debts will be discharged. It is only one required step in most cases.

It also does not mean all debts will go away. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. What happens to any specific debt depends on the facts, the chapter filed, and the law in your state and district.

Bankruptcy can still be powerful relief for many people. Depending on the case, it may erase certain unsecured debts, stop collection pressure through the automatic stay, and help someone catch up on secured debts in Chapter 13. Many people are able to keep a home or car through exemptions or a repayment plan, but outcomes are never guaranteed.

Practical next steps

If you think bankruptcy may be coming soon, it helps to move in an orderly way:

- Learn the basics about chapters and your general options.

- Gather simple documents you already have, like recent bills, lawsuit papers, pay stubs, or foreclosure notices.

- Speak with a licensed bankruptcy attorney in your area and ask which approved counseling provider to use.

- Confirm the attorney's bar license in your state.

- Complete the required credit-counseling course before filing, if your attorney says it applies.

If you want, you can start with our guides or use get matched to connect, free, with a licensed bankruptcy attorney near you. CleanSlate Match gives general educational help and matching only; we do not provide legal advice, and we do not create an attorney-client relationship.

Credit counseling before bankruptcy is usually a short required course you take before filing, and a licensed local bankruptcy attorney can help you do it the right way.

Common questions

Do I always have to take credit counseling before bankruptcy?

In most Chapter 7 and Chapter 13 cases, yes. There can be limited exceptions, but they are narrow, and the rules can vary by district, so a licensed bankruptcy attorney should review your situation.

Is the course hard or embarrassing?

Usually no. For most people, it is a short, practical course done online or by phone, and it is not a judgment about your character or worth.

Can I file bankruptcy the same day I decide to do it?

Sometimes urgent cases move quickly, but in most situations the required credit counseling must be completed before filing. If you are facing a garnishment, foreclosure, or lawsuit, speak with a licensed bankruptcy attorney right away because timing matters.

Will credit counseling stop my wage garnishment or foreclosure?

No. The counseling course itself usually does not stop collection action. The automatic stay usually begins when a bankruptcy case is actually filed.

Does taking the course mean all my debts will be erased?

No. Bankruptcy does not erase every debt, and some debts usually survive, such as most student loans, recent income taxes, child support, alimony, most fines, and debts from fraud.

Can CleanSlate Match sign me up for the course or file my case?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We can help you connect with a licensed bankruptcy attorney near you, who can explain the next steps.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →