Guides

Does bankruptcy clear credit card debt?

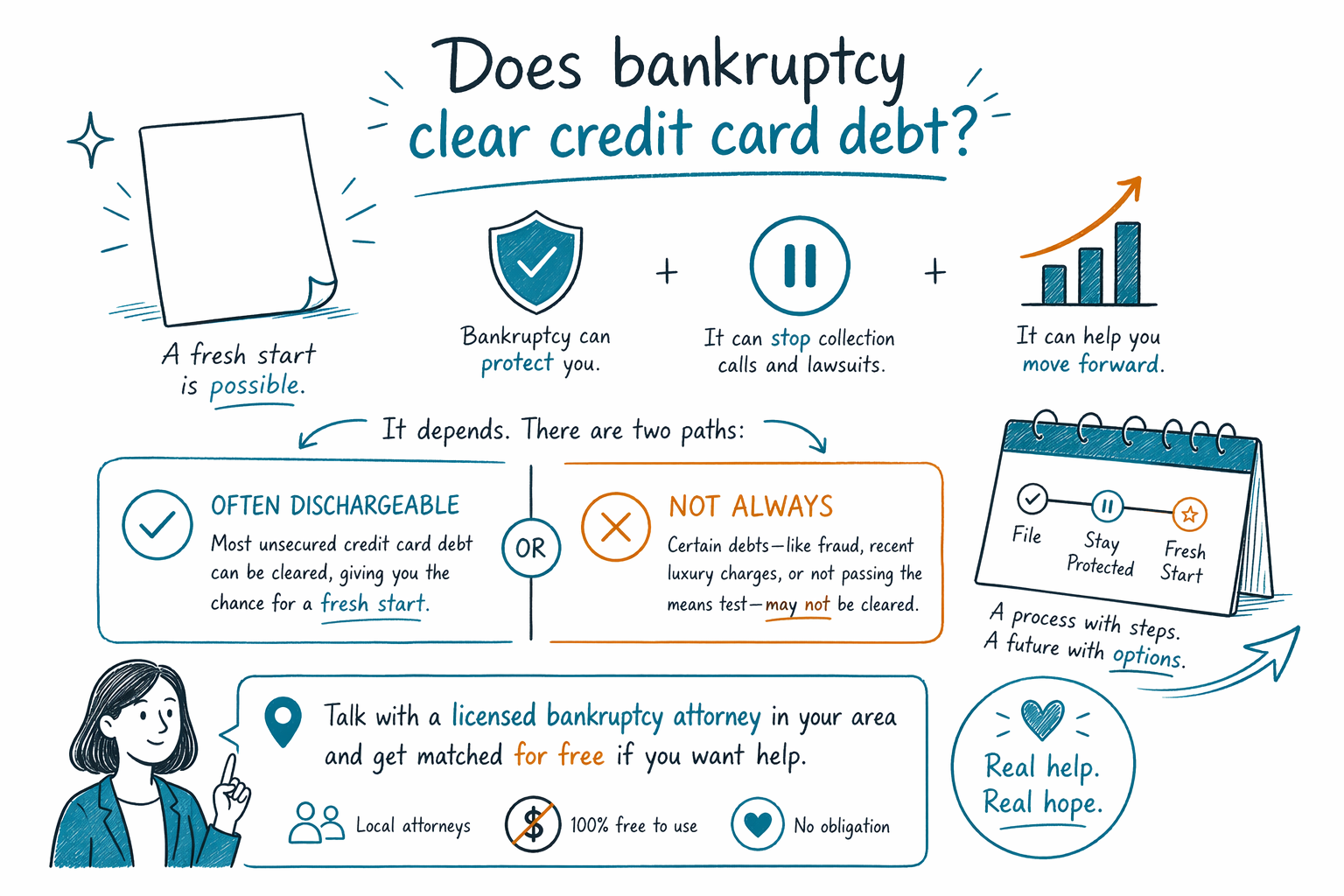

Usually, credit card debt can be discharged in bankruptcy, but not always. The answer depends on the type of bankruptcy, how the debt was incurred, and the facts of your case under your state and federal rules.

Short answer: often yes, but there are important exceptions

In many consumer bankruptcy cases, ordinary credit card debt is the kind of debt people are trying to deal with. If the debt is unsecured and there was no fraud or other legal problem, Chapter 7 may discharge it, and Chapter 13 may let you pay only part of it through a court-approved plan before the rest is discharged at the end.

But bankruptcy does not automatically erase every credit card balance. Some charges may be challenged by a creditor, especially if they were recent luxury purchases, cash advances, or charges made when the person likely could not repay. The result depends on the facts, the chapter filed, and the local court.

Bankruptcy also does not erase every kind of debt in a person's life. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. Rules vary by state and judicial district, so only a licensed bankruptcy attorney in your area can review your situation and explain what may happen in your case.

When credit card debt may be cleared

Credit card debt is usually unsecured debt. That means there is no house or car tied to it as collateral. In general, unsecured debts are the kinds of debts that bankruptcy may help with most.

In Chapter 7, many people seek a quicker fresh start. If they qualify, eligible unsecured debts may be discharged after the case moves through the court process. In Chapter 13, the person makes payments under a plan, usually for three to five years, and qualifying remaining unsecured debt may be discharged at the end if the plan is completed.

A lot depends on timing and conduct. If the credit card balance grew over time from everyday living expenses, medical needs, or trying to keep up during a hard period, bankruptcy may still help. If there are signs of fraud, false information on applications, recent cash advances, or expensive purchases shortly before filing, a creditor may object and ask the court to keep some of that debt from being discharged.

- Older, ordinary unsecured card balances are often the most likely to be dischargeable

- Recent luxury purchases or cash advances may receive more scrutiny

- A creditor can object, and the court decides disputed issues

Chapter 7 vs. Chapter 13 for credit card debt

Chapter 7 and Chapter 13 can both help with credit card debt, but they work differently. Chapter 7 and Chapter 13 are not better or worse in every case; the right fit depends on income, property, arrears on a home or car, and local exemption rules.

Chapter 7 is often used when a person has limited income and cannot realistically repay unsecured debts. It may discharge qualifying credit card debt relatively quickly. But not everyone qualifies. A means test and other rules apply, and exemptions vary by state, which affects what property a person may be able to protect.

Chapter 13 is often used when someone has regular income and needs time to catch up on mortgage arrears, car payments, or tax issues while also dealing with credit card debt. It can be especially important if a person is trying to stop foreclosure or wage garnishment and needs a structured repayment plan. The automatic stay begins when a case is filed and usually pauses most collections, lawsuits, garnishments, and foreclosure actions while the case moves forward.

Many people are surprised to learn that filing bankruptcy does not always mean losing a home or car. Depending on exemptions, loan status, and the chapter filed, many people keep important property. That is one reason a local licensed bankruptcy attorney is so important.

What can stop credit card debt from being discharged

This is the part people deserve to hear clearly and honestly. Bankruptcy can be powerful, but it has limits. A credit card debt may not be discharged if a creditor proves the debt came from fraud or false pretenses. That can include using a card with no intent to repay, lying on a credit application, or certain recent charges made right before filing.

Courts may look closely at recent luxury purchases and cash advances. There is no single simple rule that fits every case, and deadlines matter. A creditor usually must raise the issue in court. If no one objects, some debts may still be discharged, but you should not assume that will happen.

Also, even if credit card debt is dischargeable, other debts may remain. Bankruptcy usually does not discharge child support, alimony, most student loans, recent income taxes, most criminal fines, and some debts from fraud or intentional injury. A bankruptcy attorney can help you sort out which debts may be helped and which may survive.

What filing may cost, and what CleanSlate Match does

People often worry they cannot afford to even ask for help. A first consultation with a bankruptcy attorney may be free or low cost, depending on the office. If someone hires an attorney for a consumer bankruptcy case, many attorneys charge a flat fee rather than billing by the hour. There is also a court filing fee and a small required credit-counseling fee.

As a very general educational range, Chapter 7 attorney flat fees are often around $1,000 to $2,500, and Chapter 13 attorney flat fees are often around $3,000 to $6,000 or more, depending on the district, the complexity of the case, and whether there are disputes. Court filing fees are commonly a few hundred dollars, and the required credit-counseling course is usually a small additional cost. These are not quotes, not promises, and not the same in every state or court.

Costs can go up if there is a business involved, non-exempt property, recent transfers, tax issues, lawsuits, creditor objections, or a complicated home or car situation. A local attorney can tell you what fees apply in your district and whether payment plans are available.

CleanSlate Match is a free matching service, not a law firm, not a lawyer, and not your attorney. We do not file bankruptcy and we do not create an attorney-client relationship. We simply help connect people with a licensed bankruptcy attorney near them. It is always free to the person seeking help.

A practical next step if you are overwhelmed

If you are behind on cards, getting collection calls, facing a lawsuit, or worried about garnishment, it is reasonable to get legal information before things get worse. You do not need to feel embarrassed. Many people turn to bankruptcy after job loss, illness, divorce, immigration stress, or just trying to keep a family afloat.

Here is a calm way to move forward:

- Learn the basics in our guides and overview of chapters.

- Make a simple list of your debts, lawsuits, garnishments, and any urgent deadlines.

- Gather basic papers you already have, like collection letters, card statements, and court notices.

- Get matched, free, through CleanSlate Match with a licensed bankruptcy attorney near you.

- Ask the attorney to explain which debts may be discharged, what may survive, what chapter may fit, and what the total flat fee, court fee, and course fee would be in your district.

- Confirm the attorney's state bar license before hiring.

When you contact us, we only ask for contact details and general intent, such as your name, phone, optional email, state, preferred language, and a brief description of what is going on. We do not ask for a Social Security number, bank account numbers, credit card numbers, or other financial account details.

The main thing to remember is this: there may be a real path forward, but you deserve advice from a licensed bankruptcy attorney who knows your state and local court rules.

Credit card debt is often dischargeable in bankruptcy, but not always, so it is smart to speak with a licensed bankruptcy attorney in your area and get matched for free if you want help.

Common questions

Will bankruptcy erase all of my credit card debt?

Sometimes it can discharge most or all qualifying credit card debt, but not always. Recent luxury charges, cash advances, or debts tied to fraud may be challenged, and outcomes depend on the facts of the case.

Can credit card companies stop my bankruptcy from clearing the debt?

A creditor can object and ask the court to rule that a particular debt should survive, usually by claiming fraud or improper recent charges. They do not automatically win; the court looks at the evidence and the law.

If I file bankruptcy, will collections and garnishment stop?

When a bankruptcy case is filed, the automatic stay usually pauses most collection actions, lawsuits, wage garnishments, and foreclosure activity right away. There are exceptions, and the exact effect depends on the kind of case and your history.

Can I keep my home or car if I file over credit card debt?

Many people do keep their home or car, depending on exemptions, loan status, and whether they file Chapter 7 or Chapter 13. Property rules vary a lot by state and district, so a local attorney should review your case.

How much does it cost to file bankruptcy for credit card debt?

Many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. General ranges are often about $1,000 to $2,500 for Chapter 7 and about $3,000 to $6,000 or more for Chapter 13, but those are not quotes and vary by district and complexity.

What does CleanSlate Match do?

CleanSlate Match is a free matching service that helps connect you with a licensed bankruptcy attorney near you. It is not a law firm, does not give legal advice, and does not create an attorney-client relationship.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →