Guides

Can i buy a house after bankruptcy?

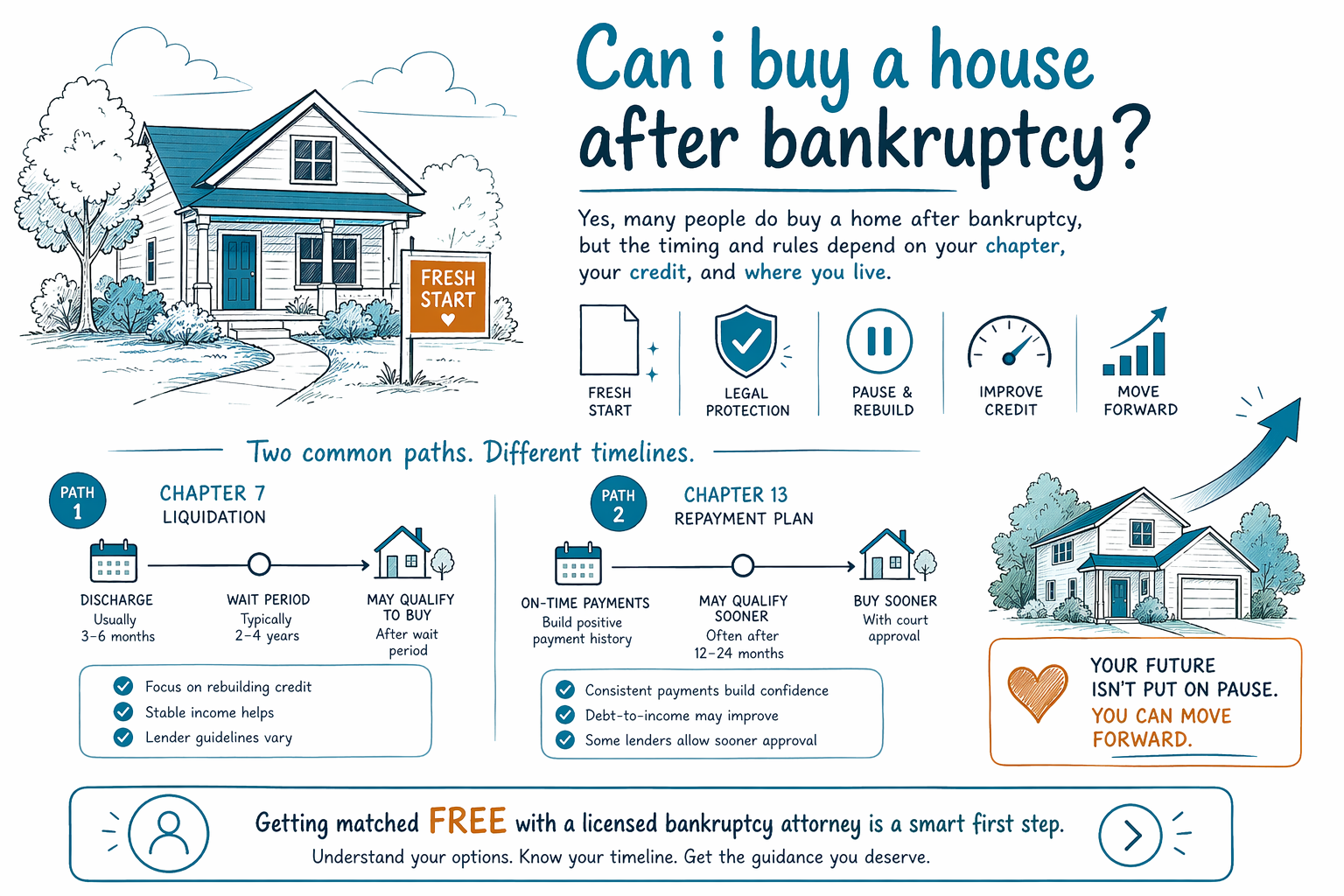

Yes, many people can buy a house after bankruptcy. The timing depends on the chapter filed, your credit recovery, and the mortgage rules lenders use — and bankruptcy rules vary by state and district.

The short answer

Bankruptcy does not mean you can never own a home. For many people, it is a reset that later makes homeownership possible again, especially after the immediate debt pressure eases.

The real question is usually not "can I ever buy?" but "when will a lender approve me, and what will I need to show?" That depends on the type of bankruptcy, how the case ends, your credit after the case, your income, your savings, and the mortgage program.

If you are overwhelmed right now, that does not mean a house is out of reach. It just means the path may take some time and planning.

How bankruptcy can affect home buying

A bankruptcy filing can lower your credit score for a while, and lenders look closely at recent bankruptcy history. That can make it harder to get a mortgage immediately, even if the case helped stop collections, lawsuits, wage garnishment, or foreclosure.

The good news is that the automatic stay can pause most collection activity when a case is filed, and many people keep their home or car through exemptions or a Chapter 13 plan. But bankruptcy does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud.

Because mortgage rules change and are not the same everywhere, a licensed bankruptcy attorney in your area can explain how your case may affect future home-buying options.

Chapter 7 and Chapter 13 are different

In a Chapter 7 case, many people can qualify for a new mortgage sooner than they expect, but there may be a waiting period after the case is finished. In a Chapter 13 case, you are usually in a repayment plan, so buying a home may be possible in some situations, but it often requires court approval and more documentation.

Lenders also care about whether you are current on rent, whether you have stable income, and whether you have enough saved for a down payment and closing costs. Bankruptcy can help clean up the debt side of your finances, but it is only one part of getting mortgage-ready.

If you are trying to choose between chapters, our chapter guide explains the basic differences in plain language.

What usually matters to lenders

Most lenders want to see that you have had time to rebuild and that your finances are stable again. They may look at your income, employment history, debt-to-income ratio, savings, and payment history after bankruptcy.

- Keep paying current bills on time.

- Save what you can for a down payment and closing costs.

- Check your credit reports for mistakes.

- Keep records showing steady income and housing payments.

- Ask a licensed attorney or mortgage professional what waiting period applies to your situation.

Bankruptcy law, exemptions, and mortgage rules vary by state and judicial district, so there is no single timeline that fits everyone.

What bankruptcy can and cannot do

Bankruptcy can give you breathing room and may help you get back on your feet financially. For some people, that is the step that eventually makes homeownership realistic again.

But it is important to be honest: bankruptcy does not guarantee a mortgage, does not guarantee a specific credit score, and does not erase every debt. The result depends on your facts, your chapter, and the rules where you live.

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The exact amount depends on the chapter, complexity, and district, so any range you hear is only a range, not a quote.

How CleanSlate Match can help

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help people in the United States share basic contact details and general intent so we can connect them with a licensed bankruptcy attorney near them.

We only collect contact and general situation information, such as your name, phone, optional email, state, preferred language, and a simple description of what is going on. We do not ask for Social Security numbers, bank-account or credit-card numbers, balances, or income figures.

If you want to understand your options before you try to buy a home, get matched free with a licensed bankruptcy attorney who can explain the rules in your area.

Yes, many people do buy a home after bankruptcy, but the timing and rules depend on your chapter, your credit, and where you live — so getting matched free with a licensed bankruptcy attorney is a smart next step.

Common questions

Can I get a mortgage right after bankruptcy?

Sometimes, but usually not immediately. Lenders often require a waiting period, and the exact timing depends on the chapter filed and the loan program, so you should ask a licensed attorney or mortgage professional in your area.

Will bankruptcy ruin my chance of owning a home forever?

Usually no. Many people buy homes after bankruptcy once their finances stabilize and they rebuild credit, but the path takes time and the rules vary by state and district.

Does bankruptcy erase all debt so I can qualify faster?

No. Bankruptcy can help with many debts, but some usually survive, such as most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud. That is why a licensed attorney should review your specific situation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →