Your situation

Bankruptcy for Seniors on a Fixed Income

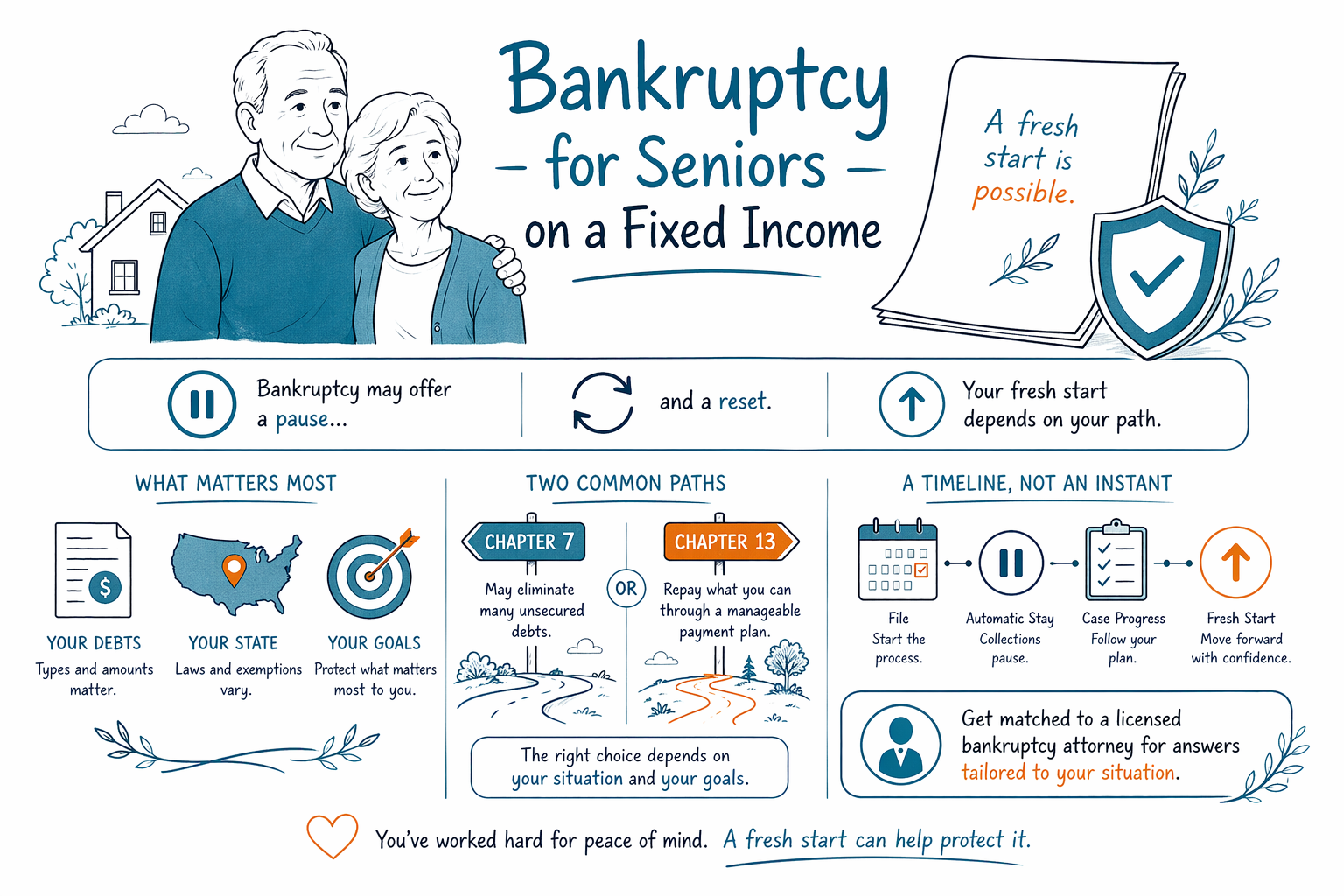

If you’re a senior on Social Security or a fixed income, debt can feel impossible to catch up on. Bankruptcy can sometimes offer relief, but what happens depends on your state, your debts, and your situation—let’s go step by step.

First: you’re not alone—and bankruptcy for seniors can be a “reset,” not a last resort

Many retirees and people living on Social Security, disability, or pensions worry that bankruptcy won’t “work” for them—or that it will remove too much.

The truth is: bankruptcy rules are different for each person. A licensed bankruptcy attorney can explain which debts may be dischargeable, what might be protected (like certain retirement or household items), and whether Chapter 7 or Chapter 13 fits your goals.

CleanSlate Match is a FREE service that connects you with a licensed bankruptcy attorney near you. We don’t file bankruptcy and we aren’t your lawyer, but we can help you get a real consultation started.

How fixed income affects Chapter 7 vs. Chapter 13 (in plain English)

Chapter 7 is often called a “fresh start” option. It may discharge (remove) many eligible unsecured debts, and in many cases the court process can pause collections. Whether you qualify can depend on the “means test,” which looks at income and expenses under current rules.

Chapter 13 is more like a structured payment plan over time. It can be an option when you have ongoing income (even if it’s fixed) and you want to keep certain property or catch up on past-due amounts. In Chapter 13, the court approves a repayment plan, and creditors generally must follow it.

Either way, the attorney will review your specific income sources (including Social Security), the type of debts you have, and your state’s protections to determine what’s realistic for you. Rules and exemptions vary by state and district.

What bankruptcy can (and can’t) do for seniors

Bankruptcy can’t erase every type of debt. Some debts usually survive bankruptcy, such as most student loans, many recent income tax debts, child support/alimony, most court fines/penalties, and debts tied to fraud or certain criminal conduct.

Bankruptcy may also not always remove secured debts the way people hope. If you owe on a house or car, your outcome often depends on whether the debt is current, the value of the collateral, what exemptions protect, and whether you choose Chapter 7 or Chapter 13.

Good news: once a bankruptcy case is filed, an “automatic stay” often pauses many collection actions—including foreclosure, lawsuits, and many types of wage garnishment—while the case is handled. An attorney can explain what will pause in your specific situation.

Common senior concerns—and what to do right now

If you’re worried about losing your home, retirement accounts, or a benefit check, it’s understandable. The first step is not panic—it’s getting accurate, case-specific guidance.

Here are practical next steps and common questions seniors ask:

- Make a simple list of your debts (who you owe and roughly what they’re for—medical, credit cards, mortgage, car, utilities, etc.).

- Keep notice letters and court papers. If you’ve received a lawsuit summons, foreclosure notice, or garnishment paperwork, do not ignore it.

- Note your income sources (for example: Social Security, pension, retirement withdrawals) and whether you have any deductions coming out automatically.

- Don’t share sensitive account numbers. For a free match, CleanSlate Match only needs contact details and general intent—no SSN or banking details.

Questions you can ask a bankruptcy attorney in your first call:

- “If I’m on Social Security, will the means test still apply to me?”

- “What debts are likely to be dischargeable in my case—and what usually isn’t?”

- “Will I be able to keep my home and car?”

- “If I’m being garnished or sued, will the automatic stay stop it?”

- “What chapter fits my goal: lowering payments, catching up, or getting a fresh start?”

Cost: what bankruptcy usually costs (flat fee + court fees) and what changes the price

Most consumer bankruptcy attorneys charge a flat fee for preparing and filing the case. You’ll also pay required court filing fees and a small required credit-counseling fee.

Because costs vary by chapter and complexity, the most honest way to think about pricing is as ranges—not exact quotes. In many cases, total attorney + court costs for a consumer case often fall roughly in the following ranges:

- Chapter 7: about $1,500–$3,500 in attorney fees, plus court filing fees (often a few hundred dollars) and required counseling.

- Chapter 13: about $2,500–$6,500 in attorney fees, plus court filing fees and required counseling (and you may also have ongoing plan payments, depending on your case).

These ranges can be higher if your case is more complex—for example: multiple properties, co-owners, business income/ownership, prior filings, foreclosure mediation, contested issues, or significant paperwork to organize. The attorney you’re matched with can explain the likely cost structure for your specific situation (ranges are not guarantees).

CleanSlate Match is free for you. There is no percentage, commission, or share of fees paid by you—participating attorneys may have a flat fee to be part of the program, but it’s always free to the person seeking help.

How to find and verify a licensed bankruptcy attorney near you

A good first consultation should be unhurried and judgment-free. You should understand (1) which debts may be dischargeable, (2) what happens to the house/car/benefits in your state, (3) whether Chapter 7 or Chapter 13 makes sense for your goal, and (4) what the process and costs look like.

Before you hire anyone, verify licensing:

- Confirm the attorney is licensed to practice in your state and is authorized to handle bankruptcy matters.

- Ask about experience with Chapter 7 and Chapter 13 cases in your judicial district.

- Check that they clearly explain limits—what bankruptcy usually can’t erase—so you’re not misled.

To get matched: you can use CleanSlate Match to connect with a licensed bankruptcy attorney near you. Start at Get matched, and browse the basics at Chapter 7 vs. Chapter 13 and other situations at situations.

If you’re a senior on fixed income, bankruptcy may offer a pause and a reset, but the real outcome depends on your debts, your state, and your goals—get matched to a licensed bankruptcy attorney for a clear, honest plan.

Common questions

I’m on Social Security and Medicare. Will bankruptcy take my benefits?

In most cases, Social Security and many benefits are protected, but the exact outcome depends on your state exemptions and how your debts and assets are structured. A licensed bankruptcy attorney can explain what typically stays protected in your area and in your specific case.

Will bankruptcy stop my garnishment or foreclosure?

Often, filing bankruptcy triggers an automatic stay that pauses many collections, including many garnishments and foreclosure actions. But what can pause—and how fast—can vary based on your case and the type of action involved.

Can I file Chapter 7 if my income is fixed?

Many people on fixed incomes still may qualify for Chapter 7, but eligibility can involve a means test and other factors. Your attorney will review your income sources, expenses, and the debts involved to determine the right chapter.

What debt usually does NOT go away in bankruptcy?

Some debts usually survive, such as many student loans, recent income taxes, child support/alimony, most court fines/penalties, and debts related to fraud. Your attorney can tell you which of your debts are likely to be dischargeable.

How much does a bankruptcy attorney cost for seniors?

Most consumer attorneys charge a flat fee, plus required court filing fees and a small required credit-counseling fee. Total costs vary by chapter and complexity, so you’ll receive a realistic range after the attorney reviews your situation.

Related help

How the automatic stay and Chapter 13 can pause foreclosure and help you keep your home.

Open → Bankruptcy When Your Wages Are Being GarnishedHow filing can stop a garnishment quickly and protect your paycheck.

Open → Bankruptcy When You're Buried in Medical DebtHow bankruptcy treats medical bills and why it's one of the most common reasons people file.

Open →