Guides

What is chapter 13 bankruptcy?

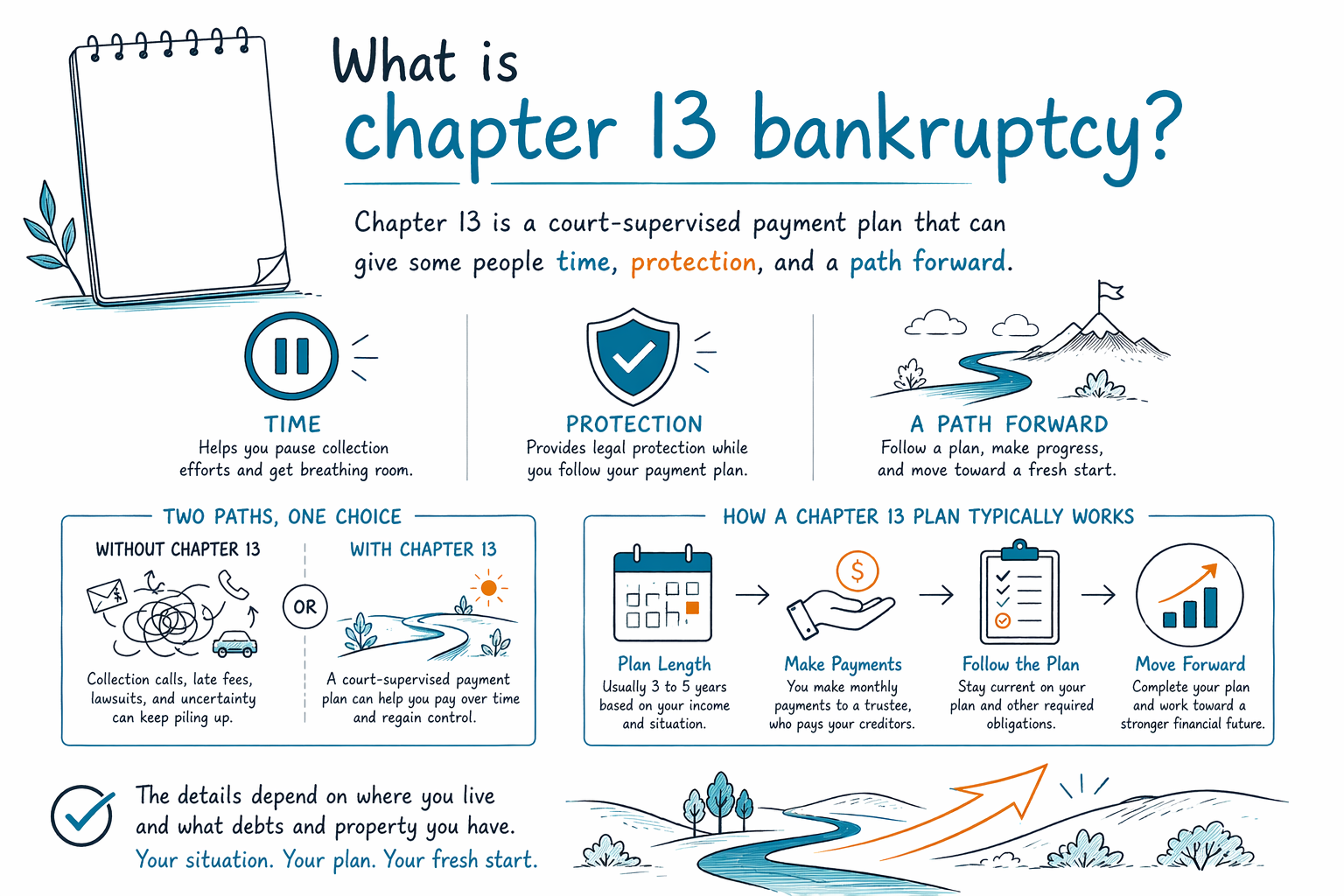

Chapter 13 is a type of consumer bankruptcy that lets some people repay part of what they owe through a court-approved plan, usually over 3 to 5 years, while getting protection from many collection actions. It can be a real path to stability, but the rules and results depend on your state, district, income, property, and debts.

The short answer

Chapter 13 bankruptcy is often called a "repayment plan" bankruptcy. Instead of selling property to pay creditors, you propose a monthly plan to pay some or all of certain debts over time, usually 3 to 5 years, under the supervision of the bankruptcy court and a trustee.

For many people, the main reason to look at Chapter 13 is not just reducing debt. It is buying time and protection. Filing a case can trigger the automatic stay, which usually pauses most collections, wage garnishments, foreclosure actions, repossessions, and lawsuits while the case moves forward.

Chapter 13 can help people who are behind on a mortgage or car loan catch up over time, and it can sometimes help when Chapter 7 is not available or is not the best fit. But it does not erase every debt, and it is not right for everyone. Bankruptcy laws, exemptions, local practices, and payment rules vary by state and judicial district, so a licensed bankruptcy attorney in your area should review your specific situation.

How Chapter 13 works in real life

In a Chapter 13 case, you file bankruptcy forms with the court and propose a payment plan based on your income, necessary living expenses, debts, and property. If the court confirms the plan and you make the required payments, you may be able to catch up on certain overdue debts and discharge some remaining eligible unsecured debt at the end.

A trustee is assigned to the case. The trustee reviews your paperwork, receives plan payments, and distributes money to creditors according to the confirmed plan. You usually make one regular monthly payment into the plan, though the exact structure depends on the case.

Chapter 13 is commonly used by people who have regular income and need time to deal with arrears, tax issues, or property they want to keep. It can also help if you have nonexempt property that might be at risk in Chapter 7, or if your income is too high to qualify easily for Chapter 7 under the means test. You can learn more about different bankruptcy options in our guides and chapters overview.

- Typical plan length: 3 to 5 years

- Often used to catch up on missed mortgage or car payments

- Usually involves one monthly plan payment to the trustee

What Chapter 13 may help with

Chapter 13 can be helpful when the problem is not only the amount of debt, but also the timing. If you fell behind because of job loss, illness, divorce, reduced hours, or another setback, a repayment plan may let you spread out arrears over time instead of dealing with immediate collection pressure.

It may help you stop or pause wage garnishment, delay or stop many foreclosure actions, and handle some tax debts or secured debts in a more organized way. Many people are able to keep their home or car through exemptions, through ongoing payments, or through a Chapter 13 plan that cures arrears over time.

But there are limits. Chapter 13 does not mean every debt disappears. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support, alimony, most court fines, and debts caused by fraud. Outcomes depend on the facts of the case, the type of debt, and local rules.

- May pause most collections through the automatic stay

- May help you catch up on mortgage arrears over time

- Does not usually erase child support, alimony, or most student loans

Who Chapter 13 is often for

Chapter 13 is often considered by people who have steady income but need room to breathe. That can include someone behind on a mortgage, facing garnishment, trying to save a car from repossession, or dealing with tax debt or other obligations that cannot easily be handled all at once.

It can also be an option for people who do not qualify for Chapter 7 or who would rather use a plan to protect property. In some cases, Chapter 13 is chosen because it gives a structured way to deal with secured debts while keeping important assets.

Whether it is the better choice depends on many details: your household income, your budget, what you own, what debts you have, whether debts are secured or unsecured, and your state's exemption rules. That is why this is general educational information only, not legal, tax, or financial advice. A licensed bankruptcy attorney can explain how your local court usually handles cases like yours.

Costs, paperwork, and what to expect

Most consumer bankruptcy attorneys charge a flat fee for a Chapter 13 case, plus the court's filing fee and a small required credit-counseling fee. In many areas, Chapter 13 attorney flat fees are higher than Chapter 7 because the case lasts longer and involves more work. A common general range is roughly $3,000 to $7,500 or more in attorney fees, plus the court filing fee and a small course fee. These are not quotes. The real amount depends on your district, the complexity of your case, the attorney, and whether extra issues come up.

Costs may be higher if you are trying to stop a foreclosure quickly, have business-related debts, tax issues, prior bankruptcy filings, property questions, lien issues, or disputes with creditors. In some Chapter 13 cases, part of the attorney's fee may be paid through the plan if local rules allow, but the details vary by district.

The paperwork is detailed. You generally need to disclose your assets, debts, income, expenses, recent financial history, and other required information to the court. Because mistakes can cause delays or serious problems, many people choose to work with a licensed bankruptcy attorney. You should also confirm that any attorney you hire is licensed and in good standing with the state bar.

How CleanSlate Match can help

If you are overwhelmed, you do not have to figure this out alone. CleanSlate Match is a free matching service that helps connect people with a licensed bankruptcy attorney near them. We are not a law firm, not a lawyer, and we do not file bankruptcy or create an attorney-client relationship.

We only collect basic contact information and general intent, such as your name, phone number, optional email, state, a general sense of what is going on, and your preferred language. We do not ask for your Social Security number, bank account numbers, credit card numbers, or detailed account information.

If you want, you can get matched for free and speak with a licensed attorney in your area who can explain whether Chapter 13, Chapter 7, or another option may fit your situation. It is okay to ask questions, compare options, and move at your own pace.

Chapter 13 is a court-supervised payment plan that can give some people time, protection, and a path forward, but the details depend on where you live and what debts and property you have.

Common questions

Is Chapter 13 the same as wiping out all my debt?

No. Chapter 13 is a repayment plan, and while some eligible unsecured debt may be discharged at the end, some debts usually survive bankruptcy, such as child support, alimony, most student loans, recent income taxes, most court fines, and debts from fraud.

Can Chapter 13 stop foreclosure or wage garnishment?

Filing a bankruptcy case usually triggers the automatic stay, which pauses many collection actions, including most garnishments, lawsuits, and foreclosure activity. But there are exceptions, deadlines, and limits, especially if you have filed before, so a local attorney should review your case quickly.

How long does Chapter 13 last?

Most Chapter 13 plans last 3 to 5 years. The exact length depends on your income, plan terms, and local rules.

Can I keep my house or car in Chapter 13?

Many people do keep their home or car through exemptions or by using a Chapter 13 plan to catch up on missed payments over time. Whether that is possible depends on the value of the property, the loan, your budget, and the rules in your state and district.

How much does Chapter 13 bankruptcy cost?

In many areas, consumer bankruptcy attorneys charge a flat fee for Chapter 13, often roughly $3,000 to $7,500 or more, plus the court filing fee and a small required credit-counseling fee. Those are general ranges, not quotes, and the real amount depends on your district and how complex the case is.

Is CleanSlate Match my lawyer?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help connect you with a licensed bankruptcy attorney near you, and no attorney-client relationship exists with us.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →