Guides

What is a lien?

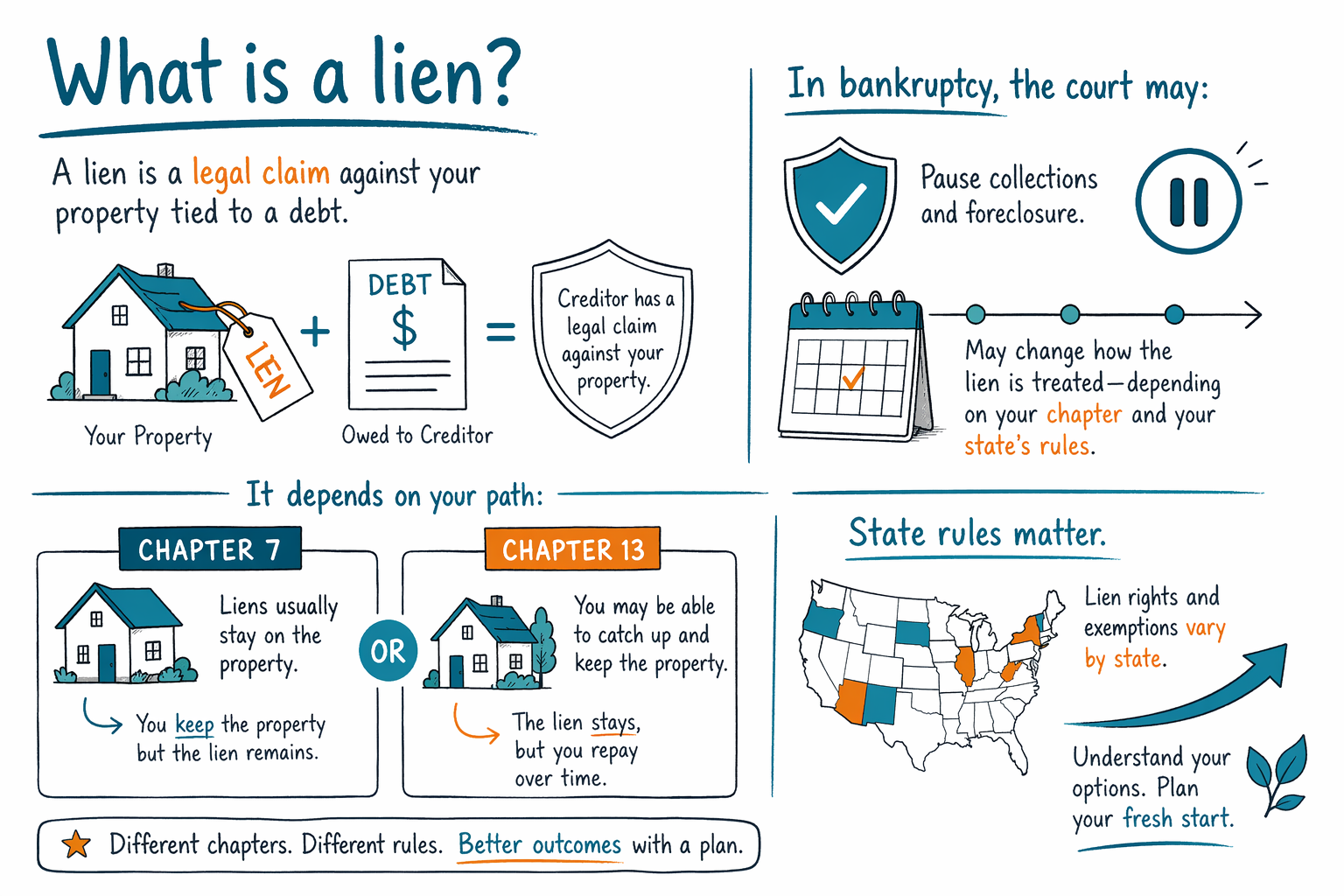

A lien is a legal “claim” on your property that lets a creditor take certain steps to get paid. If you’re facing debt, a lien can feel scary—but you have options, and a licensed bankruptcy attorney can explain what applies in your case.

A lien, in plain language

A lien is a legal right a person or company (like a creditor) gets to attach to your property—usually your home, land, or sometimes a car or other asset.

If the debt isn’t paid, a lien can make it harder to sell or refinance because the lien typically has to be paid off before clear ownership transfers. In some situations, it can also lead to collection steps like foreclosure (for a home) or other legal processes, depending on the type of lien and state rules.

- Think of it as a “holder” marking that your property is tied to a debt.

- Liens are recorded or enforced through specific legal steps that vary by state.

Common types of liens you might hear about

You may see different names depending on how the lien was created. Some liens are tied to a loan (like a mortgage), while others come from court judgments or unpaid taxes.

Here are a few common categories:

- Mortgage liens: the lender’s security interest on your home

- Judgment liens: a lien that can attach to property after a court case and judgment (details vary by state)

- Tax liens: liens related to unpaid state or federal taxes

Whether a lien is “secured” (backed by property) or “unsecured” affects how it’s handled during bankruptcy. The exact rules vary by state and by the bankruptcy court’s district.

- A mortgage lien is often connected to a specific property loan.

- A judgment lien usually comes after a lawsuit and judgment.

Where liens show up in your life (and how they affect you)

Liens can affect both your short-term options and your long-term plan. For example, if you want to sell a home, refinance, or transfer ownership, a lien often must be resolved first so the title can be clear.

Liens can also be part of larger collection actions. Depending on the facts, a creditor may use the lien to pursue foreclosure, wage or bank actions, or other steps. If you’re overwhelmed, it can help to focus on what’s happening right now and what deadlines you may be facing.

- A lien can block smooth selling/refinancing until it’s handled.

- Different debts can lead to different collection steps.

Can bankruptcy stop or remove a lien? (The honest answer)

Bankruptcy may be able to affect liens, but it doesn’t automatically erase every lien in every situation. The result depends on the lien type, when it was created, how it’s attached to the property, and your state’s exemption rules.

In general terms (not legal advice):

- Filing bankruptcy can trigger an automatic stay, which often pauses many collection actions, including many foreclosure and lawsuit activities, while the case is pending.

- Whether the lien is removed, “stripped,” avoided, or treated differently depends on the chapter (Chapter 7 vs. Chapter 13), the property, and state/district law.

- Some debts commonly survive bankruptcy—such as certain taxes, child support/alimony, many student loans, court fines, and debts involving fraud. Even when a debt continues, a lien may still be handled differently depending on the circumstances.

Because rules vary by state and bankruptcy court district, the safest next step is to discuss your specific lien with a licensed bankruptcy attorney who can review the documents and explain realistic outcomes.

- An automatic stay can pause many collections soon after you file.

- Lien outcomes vary widely—ask a licensed attorney for case-specific guidance.

Chapter 7 vs. Chapter 13: how liens are usually treated

Chapter 7 and Chapter 13 are different paths. The best choice depends on your income, your debts, the property involved, and what you want to protect.

- Chapter 7 often focuses on discharging eligible debts, but lien treatment depends on the type of lien and state law. Some liens may remain even if you get a discharge for the debt.

- Chapter 13 involves a court-approved repayment plan, which can sometimes help you catch up on certain secured debts and keep property, depending on the facts.

If you’re trying to stop a foreclosure or deal with judgment liens, a bankruptcy attorney can explain which chapter may fit your situation and what documentation is needed. If you want a helpful starting point, you can read more about chapters and the differences before you talk to an attorney.

- Chapter choice and your state rules often determine what happens to property and liens.

- A lawyer can review the lien type and your goals (keeping home/car, stopping foreclosure).

What to do next (without sharing sensitive information)

If a lien is on your record, try to stay calm and take one practical step at a time. You don’t have to guess what it means, and you don’t have to face it alone.

- Gather what you already have: lien notice(s), court case numbers (if any), foreclosure notices (if any), and any letters from the creditor.

- Note key dates: when the lawsuit/judgment happened, when the lien was recorded, and any deadlines you’ve been given.

- Get matched with a licensed bankruptcy attorney near you through get-matched so you can ask specific questions about lien treatment in your state.

- During the consultation, confirm the attorney is licensed to practice bankruptcy law and ask about likely outcomes. Be cautious of anyone who promises a guaranteed result.

CleanSlate Match is a free matching service. We do not file bankruptcy and we are not a law firm, and we don’t create an attorney-client relationship. We collect only contact details and general intent—never your SSN, bank account, or account numbers.

- Bring documents and deadlines—skip sensitive financial details you don’t need to provide upfront.

- Ask a licensed attorney what could happen to your specific lien.

Cost and expectations: what you should know before hiring an attorney

Many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The total you pay can vary based on the chapter, how complex your case is, and the bankruptcy court’s rules in your district.

Typical ranges you may see (not quotes) are:

- Chapter 7: flat attorney fee often roughly in the $1,500–$3,500 range, plus the court filing fee (often a few hundred dollars) and a small credit-counseling fee.

- Chapter 13: flat attorney fee often roughly in the $3,000–$6,000 range, plus the court filing fee (often a few hundred dollars) and a small credit-counseling fee.

These ranges can go up if there’s a foreclosure, multiple liens, lots of creditors, or additional motions. The attorney you meet with can give clearer expectations after reviewing your situation—there are no guarantees. Outcomes depend on facts, state law, and district rules.

- Costs are usually flat-fee based, plus court and required counseling fees.

- Complexity and local rules can change the final total.

A lien is a legal claim against your property tied to a debt, and bankruptcy may pause collections and sometimes change lien treatment—but what happens depends on your chapter and your state’s rules, so get matched with a licensed attorney.

Common questions

If I have a lien, does that mean I’m going to lose my home?

Not necessarily. A lien can make selling or refinancing harder, and it can be used in some collection actions, but losing your home depends on the type of lien, whether foreclosure steps are underway, and your state’s process. A bankruptcy attorney can explain what’s realistic in your situation.

Will bankruptcy automatically remove my lien?

Usually not automatically. Bankruptcy can pause collections through the automatic stay, and some liens may be changed, removed, or treated differently depending on your chapter and state/district rules. A licensed bankruptcy attorney can review your lien documents and explain likely outcomes.

Does bankruptcy erase the debt that created the lien?

Sometimes, for debts that are dischargeable, the underlying personal debt can be wiped out—but some debts commonly survive bankruptcy (for example, many student loans, recent income taxes, child support/alimony, many court fines, and debts tied to fraud). Even if some debt remains, lien handling may still differ based on the case.

How do I know what kind of lien I have?

Look for documents like a recorded lien notice, judgment details, mortgage paperwork, or any court papers showing the source of the claim. If you’re matched with an attorney, you can ask them to explain the lien type and how it affects your property under your state’s rules.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →