Guides

What happens to cosigners in bankruptcy?

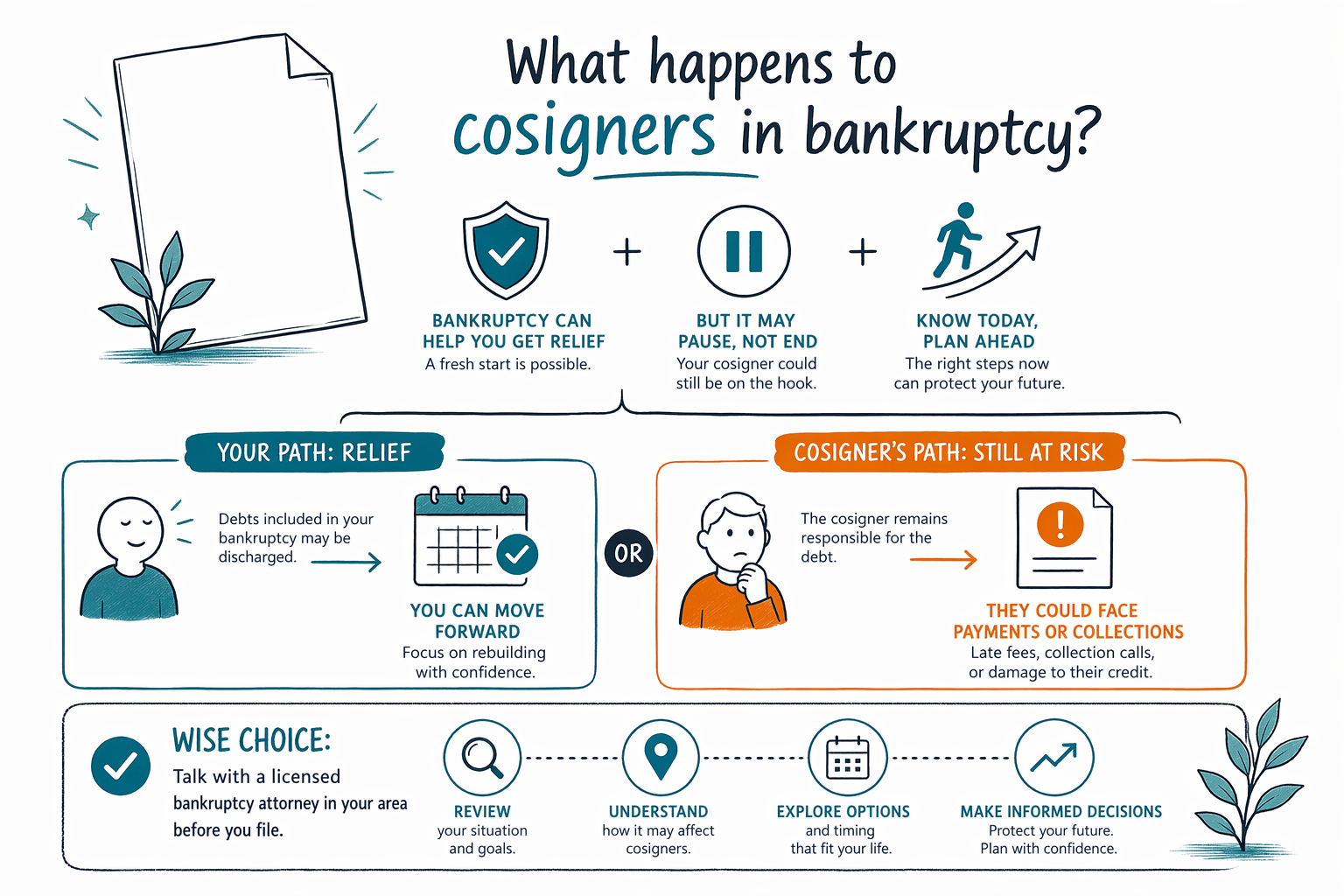

If you have a cosigner, bankruptcy can affect that person too — but the result depends on the chapter, the debt, and your state or district. A licensed bankruptcy attorney can explain the risks and the options in your area.

The short answer

When one person files bankruptcy, the cosigner is not always protected just because the borrower filed. In Chapter 7, the lender may still be able to collect from the cosigner on debts that are not paid in the bankruptcy case.

In Chapter 13, there may be more protection for cosigners on certain consumer debts, but the details matter. Bankruptcy rules, exemptions, and court practices vary by state and federal district, so the same debt can be handled differently from one place to another.

The safest way to understand the risk is to have a licensed bankruptcy attorney review the specific debt before you file. CleanSlate Match is a free matching service, not a law firm, and we do not give legal advice.

- A cosigner can still be pursued by a creditor in some cases.

- Bankruptcy may help stop collection against you, but not always against the cosigner.

What usually happens to the cosigner

A cosigner is someone who promised to repay the debt if the main borrower does not. Because of that promise, the lender may have a separate right to collect from the cosigner.

If you file Chapter 7, your discharge may wipe out your personal responsibility for qualifying debts, but it does not automatically erase the cosigner’s responsibility. The lender may still send bills, make calls, or sue the cosigner for the remaining balance unless another rule protects them.

If you file Chapter 13, some debts that are covered by your repayment plan may give cosigners more breathing room. Still, the protection is limited and depends on the type of debt, how it is listed, and what the court allows.

- Cosigners can be family members, friends, or a spouse.

- A debt can feel ‘shared,’ but bankruptcy treatment is still very specific.

How this affects common debts

Cosigned debts often include car loans, personal loans, private student loans, and sometimes credit cards or medical arrangements. The result is different for each kind of debt.

For example, if you are behind on a car loan and the debt is cosigned, bankruptcy may help you protect the car or restructure the payment, but the cosigner can still be affected if the lender is not paid in full. If the debt is unsecured, the creditor may focus on the cosigner once you file.

Some debts are harder to discharge than others. Many student loans, recent income taxes, child support, alimony, most court fines, and debts from fraud usually survive bankruptcy unless a very specific exception applies. A local attorney can tell you what your case may do, but no one should promise a result without reviewing the documents.

- Secured debts and unsecured debts are treated differently.

- Some debts are often harder to discharge than others.

What you can do before filing

If a cosigner may be affected, ask a bankruptcy attorney to look at the whole picture before you file. That includes the debt type, who signed it, whether payments are current, and whether you are trying to keep a car, home, or other property.

A few practical steps can help:

1. Gather the loan or credit agreement.

2. Make a list of any cosigners or co-borrowers.

3. Note whether the debt is secured, like a car loan, or unsecured, like a credit card.

4. Ask the attorney how your chapter choice may affect the cosigner.

Do not send Social Security numbers, bank-account numbers, credit-card numbers, or full account balances to a matching service. CleanSlate Match only asks for contact information and general details about your situation so we can connect you with a licensed bankruptcy attorney near you.

- Bring the contract if you have it.

- Tell the attorney whether the other person is a cosigner or co-borrower.

Why talking to a local attorney matters

Bankruptcy is federal law, but many important details vary by state and judicial district. Local exemptions, filing procedures, trustee practices, and how courts handle cosigned debts can all affect the outcome.

A licensed bankruptcy attorney can also explain what filing may cost. Many consumer bankruptcy lawyers charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The exact amount depends on the chapter, the complexity of the case, and where you file, so any range is only an estimate — not a quote.

If you want help finding someone near you, get matched for free. You can also browse guides or read more about the chapters at Chapter 7 and Chapter 13.

- Always confirm the lawyer is licensed in your state.

- A short consultation can prevent a costly mistake for you or your cosigner.

Bankruptcy can help you get relief, but a cosigner may still be at risk, so it is wise to talk with a licensed bankruptcy attorney in your area before you file.

Common questions

Will my bankruptcy automatically protect my cosigner?

Not always. In some Chapter 13 cases there may be protection for certain consumer debts, but Chapter 7 usually does not stop the lender from trying to collect from a cosigner. The exact result depends on the debt and your local rules.

Can bankruptcy erase the debt for both of us?

Sometimes a debt may be discharged as to the person who files, but that does not always erase the cosigner’s responsibility. Some debts also survive bankruptcy entirely, including many student loans, recent taxes, child support, alimony, most fines, and fraud-related debts.

Should I tell the cosigner before I file?

In many cases, yes, because filing can affect them and they may need to plan for possible collection. A bankruptcy attorney can help you think through how to have that conversation.

Is CleanSlate Match my lawyer?

No. CleanSlate Match is a free matching service, not a law firm, and it does not create an attorney-client relationship. We connect you with a licensed bankruptcy attorney near you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →