Guides

How long does bankruptcy stay on credit report?

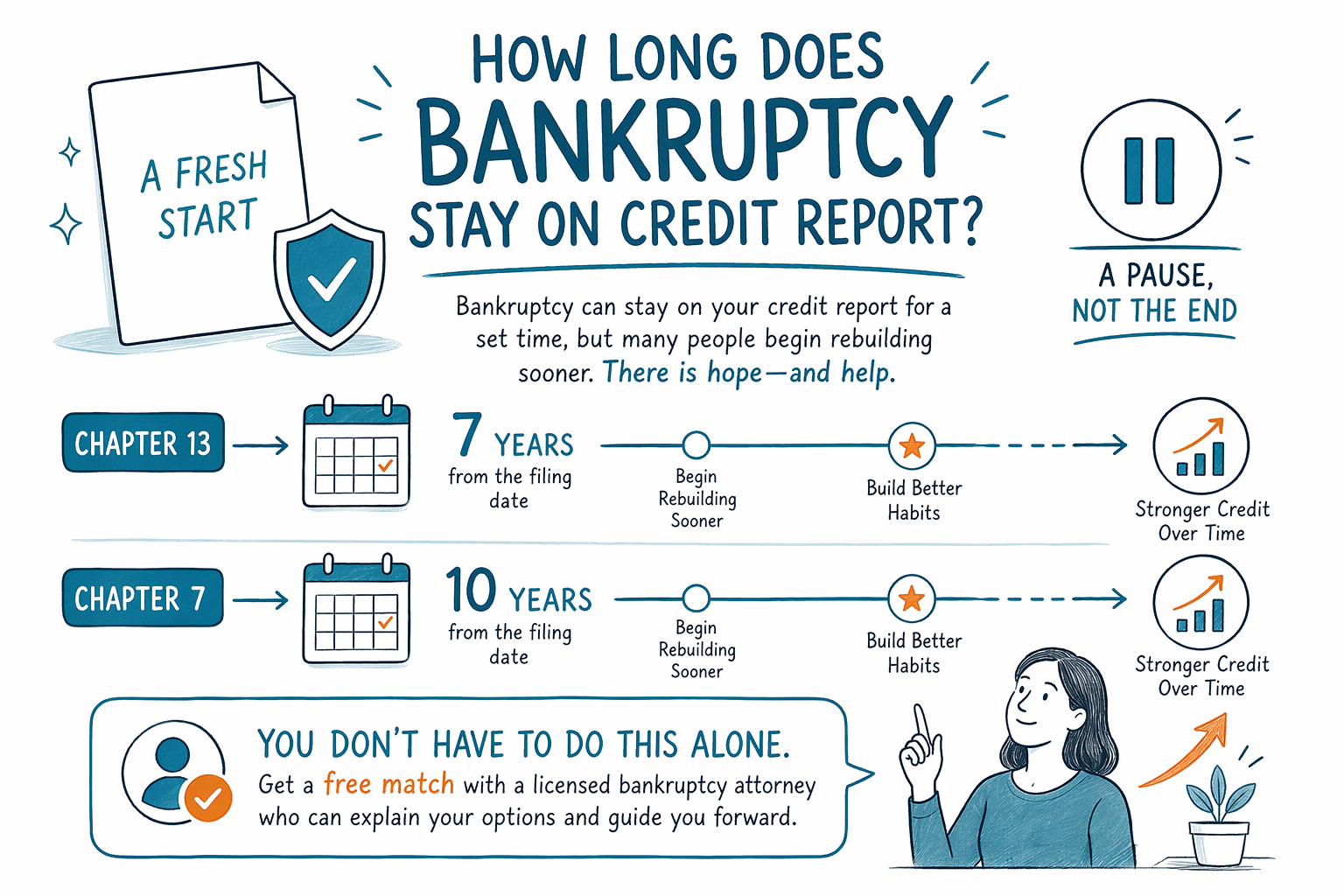

In most cases, bankruptcy stays on a credit report for up to 10 years for Chapter 7 and up to 7 years after a Chapter 13 case is filed. The exact effect on your score, and what happens in your case, can vary by state, district, and your full credit history.

The short answer

Bankruptcy is a public court case, and credit bureaus usually report it for a set period of time. Chapter 7 is typically listed for 10 years from the filing date, and Chapter 13 is typically listed for 7 years from the filing date.

That does not mean your credit is ruined for the whole time. Many people begin rebuilding credit sooner, especially after the case is finished and they start making on-time payments again. The impact depends on what else is on your report, how much debt you had, and how you handle credit afterward.

Bankruptcy rules, exemptions, and how cases are treated can vary by state and federal district, so a licensed bankruptcy attorney in your area can explain what is most likely in your situation.

What bankruptcy can and cannot do

Bankruptcy can help stop collection calls, lawsuits, wage garnishment, and, in many cases, foreclosure activity once the case is filed because of the automatic stay. It can also discharge many unsecured debts, such as credit cards and some medical bills.

But bankruptcy does not erase every debt. Debts that often survive include most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. Whether a debt is discharged depends on the chapter used, the facts of the case, and the law in your state and district.

If you are trying to understand how long bankruptcy will stay on your report, it helps to think about two different things: how long it is reported, and how long it affects you. Those are not the same.

Chapter 7 vs. Chapter 13 on a credit report

Chapter 7 is often called a liquidation case. For many people, it moves faster and can clear eligible debts sooner, but it is usually reported for 10 years.

Chapter 13 is a repayment plan made through the court. It usually stays on a credit report for 7 years from the filing date, even though the plan may last 3 to 5 years.

Which chapter makes sense depends on your income, assets, debts, and whether you are trying to save a home from foreclosure or deal with a wage garnishment. A licensed bankruptcy attorney can help explain the difference in plain words and confirm their bar license before you hire them.

How people rebuild credit after bankruptcy

Many people are surprised to learn that they can start rebuilding before the bankruptcy falls off their credit report. The most important steps are usually simple and steady:

- Pay every bill on time after the case is filed and after it ends.

- Keep balances low on any new credit you use.

- Check your credit reports for mistakes.

- Avoid taking on new debt you do not need.

- Give yourself time; rebuilding is often gradual, not instant.

If you are new to the U.S. credit system, that can feel confusing. A local attorney or a nonprofit credit counselor may be able to explain the basics, but only a licensed bankruptcy attorney can advise you on your case.

What CleanSlate Match can help with

CleanSlate Match is a free matching service, not a law firm, and not your lawyer. We help people share only basic contact information and general intent — like your state, preferred language, and whether you are dealing with credit cards, medical bills, foreclosure, or garnishment — so we can connect you with a licensed bankruptcy attorney near you.

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The total depends on the chapter, the complexity of the case, and your district, so any numbers you hear should be treated as ranges, not quotes.

If you want a calmer next step, you can start here: Get matched. You can also read more basics in our guides or compare chapters on our chapter overview.

Bankruptcy usually stays on your credit report for 7 years in Chapter 13 or 10 years in Chapter 7, but many people begin rebuilding sooner, and a free match with a licensed bankruptcy attorney can help you understand your options.

Common questions

Will bankruptcy fall off my credit report automatically?

Usually yes, after the reporting period ends, but you should still check your credit reports for errors. Sometimes information is listed incorrectly and may need to be disputed.

Can I get a mortgage or car loan after bankruptcy?

Often yes, but it may take time and the terms may be different. Lenders look at your income, payment history, and overall credit profile, not just the bankruptcy entry.

Does filing bankruptcy mean I lose everything?

Not necessarily. Many people keep important property through exemptions or a Chapter 13 plan, but rules vary by state and district. A licensed bankruptcy attorney can explain what is likely protected in your area.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →