Guides

Bankruptcy When Youre New To The Us

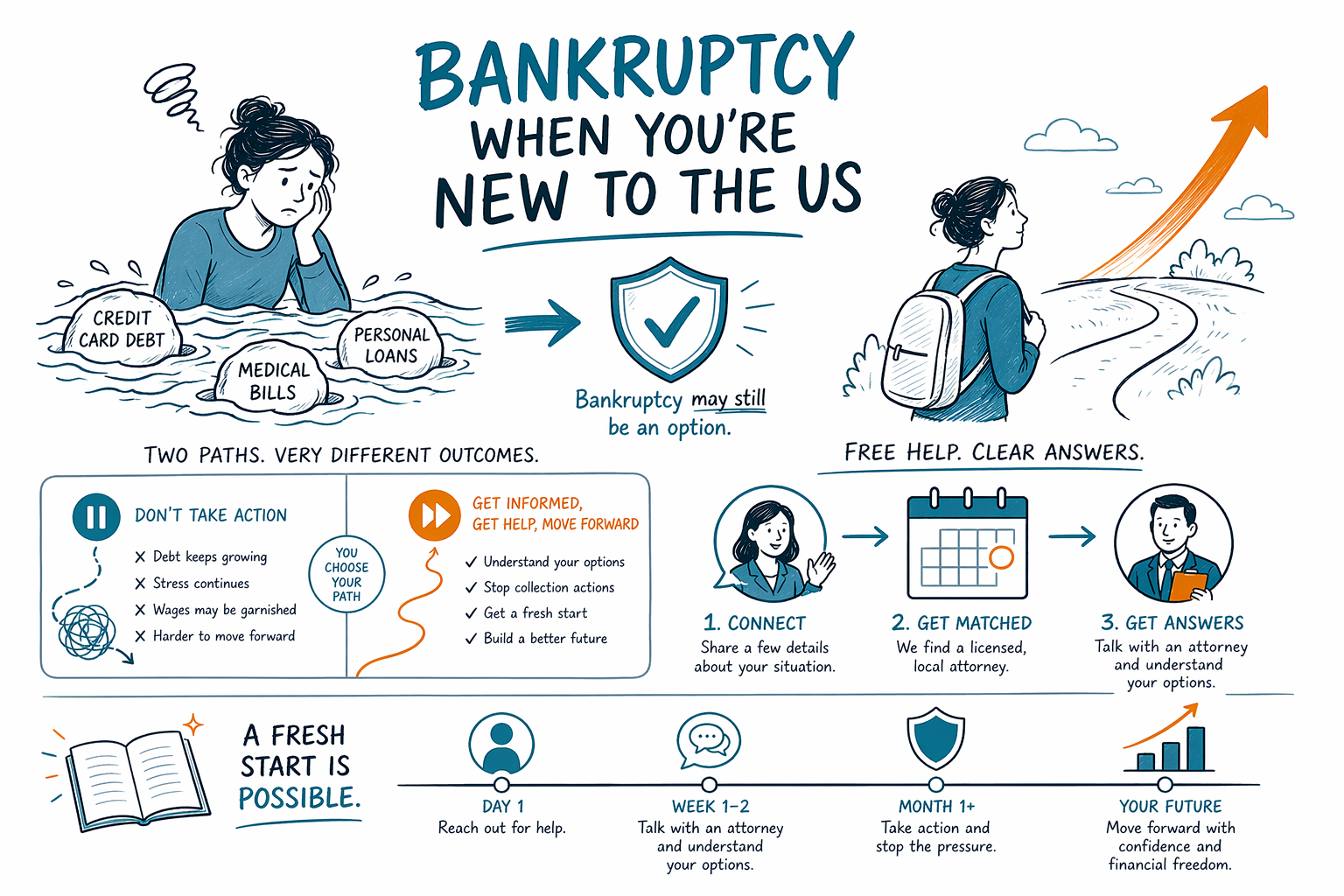

Yes, you may still be able to file consumer bankruptcy if you are new to the US. What matters is your current situation, where you live, and the type of debt you have — and the rules can vary by state and court district.

The short answer

Being new to the United States does not automatically stop you from filing bankruptcy. Many immigrants, permanent residents, visa holders, and other non-citizens look into Chapter 7 or Chapter 13 when they are overwhelmed by credit cards, medical bills, a lawsuit, wage garnishment, or mortgage arrears.

What matters most is usually where you live now, what property and income you have, and whether you meet the legal rules for the chapter you want to file. Bankruptcy is a federal court process, but some important parts — especially exemptions, local procedures, and practice details — vary by state and judicial district.

Bankruptcy can help many people get breathing room, but it does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. The result depends on the facts of the case.

If you are worried because English is not your first language, that is understandable. A licensed bankruptcy attorney in your area can explain the process in plain language and tell you how the local court handles things.

What bankruptcy may help with if you are starting over here

For many people who are new to the US, debt grows fast. A job change, medical emergency, divorce, missed rent or mortgage payments, or helping family can lead to collection calls, lawsuits, repossession threats, or garnishment. Bankruptcy is one legal tool that may help when the debt has become too much to manage.

A bankruptcy filing creates an "automatic stay." That is a legal stop sign that usually pauses most collection activity right away once a case is filed. In many cases, it can stop wage garnishment, pause foreclosure, stop collection lawsuits, and reduce the daily pressure while the case moves through court.

Chapter 7 is often used by people who cannot realistically repay unsecured debt and who qualify under the means test or another rule. Chapter 13 is often used by people who have regular income and need time to catch up on a mortgage, car loan, or certain other debts through a payment plan.

If you are not sure which chapter even applies to you, start with a basic overview of chapters or browse more plain-language guides. A local attorney can then explain what those rules mean where you live.

Questions many newcomers have

People often worry: "Do I need to be a US citizen?" Citizenship is not the only issue. In many cases, non-citizens can file consumer bankruptcy, but eligibility and practical concerns depend on your residence, your assets, your income, and the court's rules. Because immigration status and bankruptcy can sometimes overlap in complicated ways, it is especially important to speak with a licensed attorney who understands local practice.

Another common fear is paperwork. Bankruptcy cases require documents and a full, truthful financial picture, but that does not mean you should guess or hide anything. A lawyer can tell you what is actually needed and what can be explained if records are incomplete. Rules and document expectations can differ by district.

Some people are afraid that filing will mean losing everything. That is not how many consumer cases work. Exemption laws protect certain property, and many people keep their home, car, household goods, and personal belongings depending on the facts and the law in their state. In Chapter 13, people often use a repayment plan to keep property while catching up over time.

It is also normal to ask whether bankruptcy will hurt future plans. Bankruptcy can affect credit, but so can unpaid collections, judgments, and missed payments. For some people, dealing with debt through the court is the first step toward rebuilding.

What bankruptcy cannot promise

It is important to be honest here: bankruptcy is powerful, but it has limits. It may discharge many unsecured debts, such as some credit card balances, medical bills, personal loans, and old utility bills, but not every debt goes away.

Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support, alimony, most court fines and penalties, and debts caused by fraud or certain intentional wrongdoing. Secured debts like a mortgage or car loan also work differently because the lender has rights in the property.

Bankruptcy also does not fix every money problem by itself. If the issue is ongoing income loss, unaffordable housing, or a loan you want to keep, the right chapter and the right timing matter. A licensed bankruptcy attorney can explain the likely benefits and the limits based on your actual facts.

No one should promise you a guaranteed result, a guaranteed price, or that all debt will disappear. Outcomes depend on the chapter, your records, your property, your income, your debts, and the court where the case is filed.

What it may cost

Many people delay getting help because they are afraid even asking will cost too much. A first consultation with a bankruptcy attorney is often low-cost or free, but each lawyer decides that for their own office.

If someone hires a consumer bankruptcy attorney, many attorneys charge a flat fee for the legal work, plus the court filing fee and a small required credit-counseling fee. These are ranges, not quotes, and the real number depends on the chapter, the complexity of the case, and the court district.

In many areas, a straightforward Chapter 7 attorney flat fee may fall roughly in the range of about $1,000 to $2,500, plus a court filing fee that is a few hundred dollars, and a small credit-counseling cost. Chapter 13 attorney flat fees are often higher — sometimes roughly $3,000 to $6,500 or more in some districts — plus the court filing fee and the required course fees. Complex cases, urgent filings, business-related issues, prior bankruptcies, lawsuits, nonexempt assets, or difficult documentation can increase cost.

CleanSlate Match is free for the person seeking help. We are not a law firm, not a lawyer, and we do not file bankruptcy. We are a free matching service that helps connect you with a licensed bankruptcy attorney near you.

How to get help safely and simply

If you are overwhelmed, you do not need to know everything before reaching out. Start with a lawyer who handles consumer bankruptcy in your state and ask for plain-language answers. Because rules vary by state and district, local advice matters.

When you speak with an attorney's office, it is reasonable to ask whether they can communicate in your preferred language or work with an interpreter. It is also reasonable to ask about fees, timing, what documents are needed, and whether they think Chapter 7, Chapter 13, or another option may fit your situation.

CleanSlate Match can help you take that first step. We only collect contact information and general intent — such as your name, phone number, optional email, state, a general sense of what is happening, and your preferred language. We do not ask for a Social Security number, bank account numbers, credit card numbers, or detailed account balances.

If you want, you can get matched for free with a licensed bankruptcy attorney near you. You should also confirm the attorney's bar license in your state before hiring anyone.

- Ask whether the lawyer handles Chapter 7 and Chapter 13 regularly

- Ask for the total expected flat fee, filing fee, and course costs

- Ask what debts may and may not be discharged in your case

- Ask what property you may be able to protect under your state's exemptions

- Ask whether filing could stop a garnishment, lawsuit, or foreclosure

If you are new to the US and drowning in debt, bankruptcy may still be an option, and you can get free help finding a licensed local attorney to explain it clearly.

Common questions

Can I file bankruptcy if I am not a US citizen?

Possibly, yes. Citizenship alone does not decide it, but eligibility depends on your residence, your finances, your property, and the rules in your state and court district.

Will bankruptcy affect my immigration case?

It can raise important questions in some situations, which is why you should speak with a licensed attorney about your specific facts. Bankruptcy and immigration are separate areas of law, and careful local advice matters.

Can bankruptcy stop wage garnishment or foreclosure?

Once a bankruptcy case is filed, the automatic stay usually pauses most collections, including many garnishments, lawsuits, and foreclosures. There are exceptions and timing matters, so a local attorney should review your situation quickly.

Will bankruptcy erase all of my debt?

No. Some debts usually survive, including most student loans, recent income taxes, child support, alimony, most court fines, and debts tied to fraud.

How much does it usually cost to file?

Many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required course fee. A simple Chapter 7 may be around $1,000 to $2,500 in attorney fees in many areas, while Chapter 13 is often higher, but these are only general ranges, not quotes.

What does CleanSlate Match do?

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help connect people with a licensed bankruptcy attorney near them for a consultation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →