How we've helped

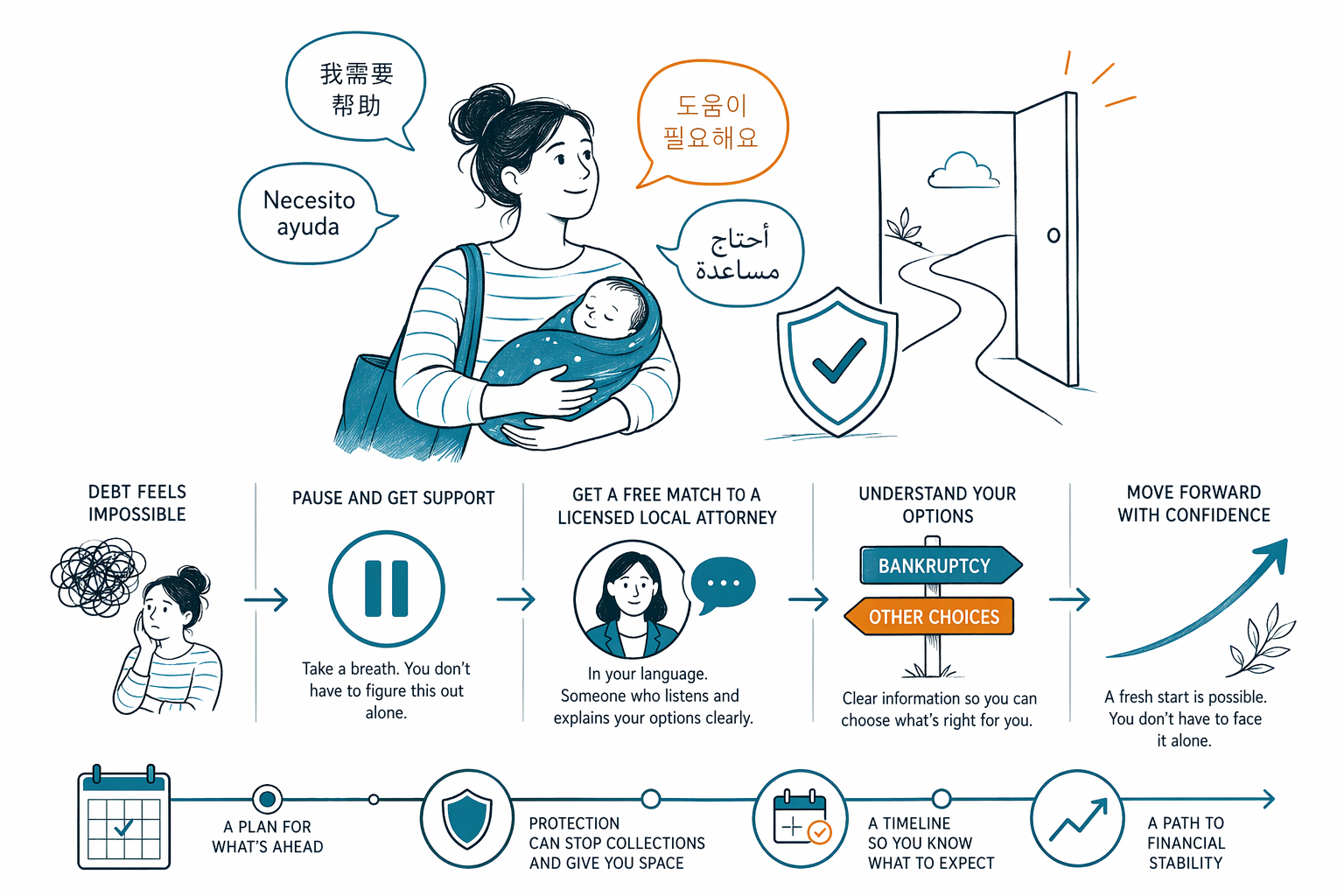

A new arrival gets help in their own language

This illustrative story shows how one new arrival, overwhelmed by credit-card debt, found calm help in their own language. It is not a real named client story, and every case depends on the facts, the state, and the court.

An illustrative story, not a promise

A person had been in the United States for less than two years. They were working hard, sending some money to family, and trying to build a life here. Then credit-card balances grew after a medical problem and a stretch of reduced work hours. Collection calls started. English was not their first language, and every phone call made the stress worse.

They were not sure what kind of help they needed. They had heard the word "bankruptcy," but did not know the difference between Chapter 7 and Chapter 13, whether they could keep their car, or whether filing would affect everything they owned. They also worried about being misunderstood because of language.

This is the kind of situation CleanSlate Match is built for. CleanSlate Match is a free matching service, not a law firm and not a lawyer. It does not file bankruptcy and does not create an attorney-client relationship. It simply helps people connect with a licensed bankruptcy attorney in their area, including attorneys who may speak their language or work with interpreters.

How they figured out what they needed

At first, they thought they had to gather every bill, every account number, and every private financial detail before asking for help. They did not. To get matched, they only needed basic contact information and a general sense of the problem: their name, phone number, optional email, state, preferred language, and a short description like "credit-card debt, behind on bills, worried about collection calls."

CleanSlate Match does not ask for a Social Security number, bank-account numbers, credit-card numbers, or detailed account balances. That mattered to them because they were already anxious and did not want to share sensitive information before speaking with a real attorney.

After learning a little more about bankruptcy chapters, they realized they did not need to decide everything alone. A licensed bankruptcy attorney could explain whether Chapter 7, Chapter 13, or another debt-relief option made sense for their situation. Bankruptcy law, exemptions, and local practice vary by state and judicial district, so general online information can only go so far.

The match and the first conversation

They used the free matching form and asked for help in their preferred language. Soon after, they were connected with a licensed bankruptcy attorney near them. Before sharing more, they did something smart: they confirmed the attorney's bar license and made sure they understood who they were speaking with.

In the consultation, the attorney slowed things down. They explained that Chapter 7 and Chapter 13 are both consumer bankruptcy options, but they work differently. Chapter 7 may help some people discharge many unsecured debts, such as credit-card debt or medical bills, if they qualify under the means test and other rules. Chapter 13 involves a repayment plan over time and may help some people catch up on missed mortgage or car payments. Which chapter, if any, fits depends on income, property, debts, goals, and local rules.

The attorney was also honest about limits. Bankruptcy does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. That honesty helped them trust the process more, not less.

Talking openly about cost

One of their biggest fears was cost. They assumed hiring a bankruptcy attorney would require a large payment they could not understand or predict. Instead, the attorney explained that many consumer bankruptcy lawyers charge a flat fee for their work, plus the court's filing fee and a small required credit-counseling fee. The exact amount depends on the chapter, how complex the case is, and the district.

As a general educational example only, Chapter 7 attorney flat fees often fall somewhere around $1,000 to $2,500 in many areas, while Chapter 13 attorney fees are often higher and may be around $3,000 to $6,000 or more, depending on the case and local court practices. Court filing fees are separate and are usually a few hundred dollars. There is also typically a small fee for the required credit-counseling course. These are ranges, not quotes, and not every case fits them.

What mattered most to them was clarity. They asked the attorney to explain what the flat fee covered, what court costs were separate, whether payment timing differed between Chapter 7 and Chapter 13, and whether any extra work could increase the total cost. Getting plain answers in their own language helped them feel less trapped and more informed.

What changed once they understood the process

The consultation did not promise a result, and it did not erase the stress overnight. But it gave them a map. They learned that if a bankruptcy case is filed, the automatic stay usually stops most collection activity right away, including many lawsuits, wage garnishments, foreclosures, and collection calls. They also learned that many people keep important property, including a home or car, depending on exemptions, payment status, and whether Chapter 13 is used to catch up over time.

Just as important, they learned what questions to ask before moving forward:

- Am I being evaluated for Chapter 7, Chapter 13, or another option?

- How does my state treat exemptions, and what property might be protected?

- What debts may not be dischargeable in my case?

- What is your flat fee, what court fees are separate, and what could change the cost?

- What documents will you need later, and what should I avoid doing right now?

With real information, their fear became something more manageable. They were no longer trying to decode legal words alone. They had a licensed attorney explaining the next steps and answering questions in a way they could understand.

A calmer next step for someone in the same position

If you are new to the US, more comfortable in another language, or simply overwhelmed, you do not have to know everything before asking for help. You do not need to be perfect, and you do not need to wait until every collector has called. A first conversation with a licensed bankruptcy attorney can help you understand your options without guessing.

CleanSlate Match is free for the person seeking help. It is not a law firm, not your lawyer, and it does not provide legal, tax, or financial advice. It helps connect you with a licensed bankruptcy attorney in your area, and you can ask for language support when you get matched.

No honest service can promise that bankruptcy will erase all debt or guarantee a particular outcome. But a clear explanation, in a language you understand, can make the next step feel possible. If you are ready, get matched for free and speak with a licensed bankruptcy attorney near you.

If debt feels impossible and language makes it harder, a free match to a licensed local bankruptcy attorney can help you understand your options clearly and safely.

Common questions

Can I ask for help if English is not my first language?

Yes. You can share your preferred language when you ask to be matched. CleanSlate Match will try to connect you with a licensed bankruptcy attorney who speaks that language or can work with an interpreter, depending on availability.

Do I need to give my Social Security number or account numbers to get matched?

No. CleanSlate Match only collects contact information and general intent, such as your name, phone number, optional email, state, preferred language, and a short description of the problem. It does not ask for your Social Security number, bank-account numbers, or credit-card numbers.

Will bankruptcy erase all of my debt?

No one can honestly promise that. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud. What happens depends on the type of debt, your facts, and the law in your state and district.

How much does a bankruptcy attorney usually cost?

Many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. As general ranges only, Chapter 7 attorney fees are often around $1,000 to $2,500, and Chapter 13 fees are often around $3,000 to $6,000 or more, but the real amount depends on the chapter, the complexity, and local rules.

What does CleanSlate Match actually do?

CleanSlate Match is a free matching service, not a law firm and not a lawyer. It helps connect you with a licensed bankruptcy attorney near you so you can get advice about your own situation.

Related help

How a couple buried in hospital bills used CleanSlate Match to find a Chapter 7 attorney and get a fresh start.

Open → A homeowner stops foreclosure with Chapter 13How someone behind on a mortgage filed Chapter 13 to catch up and keep their home.

Open → A worker stops wage garnishment in daysHow a single parent halted a garnishment and protected their paycheck after getting matched with a lawyer.

Open →