Your situation

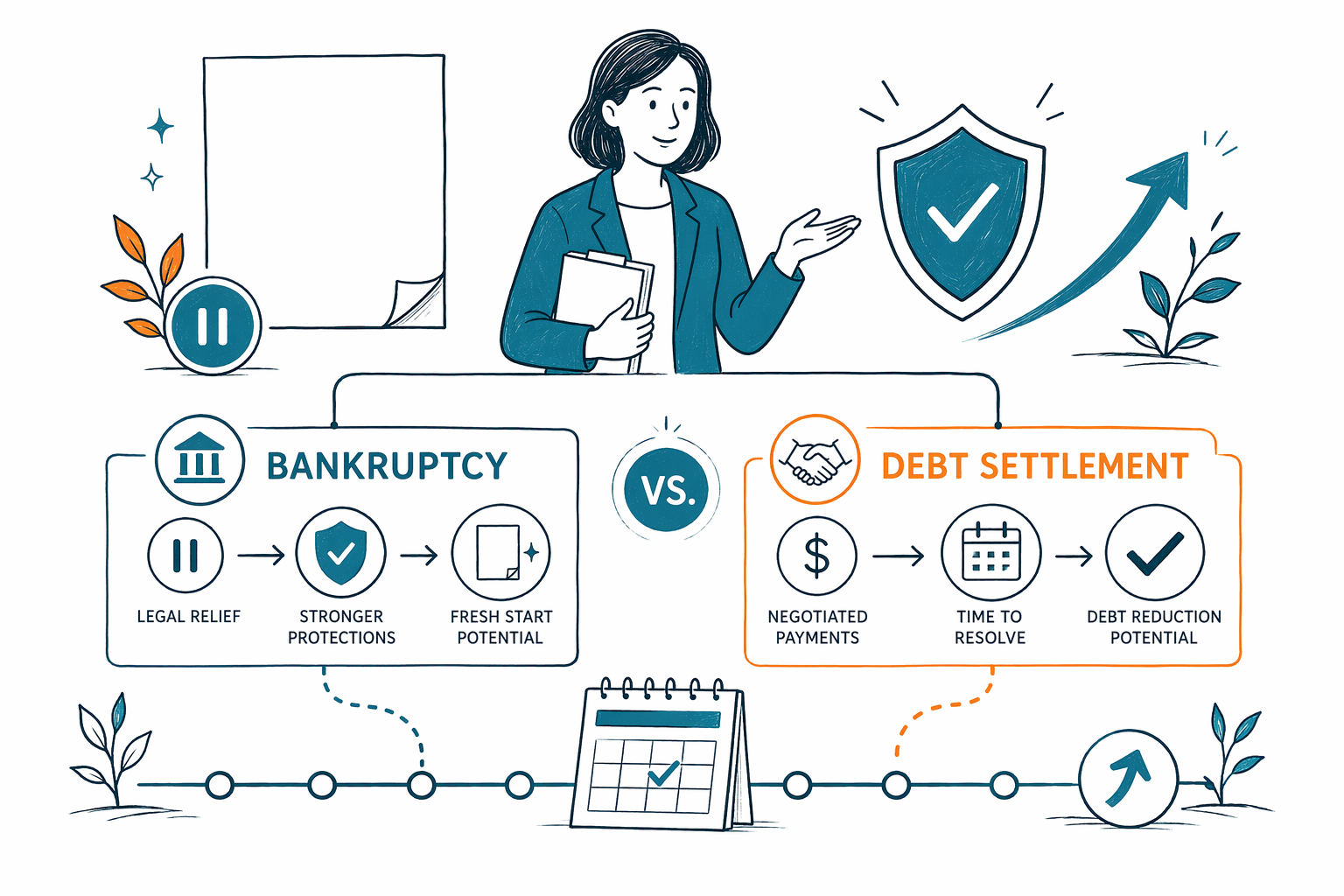

Bankruptcy vs Debt Settlement

If debt feels impossible, you may be comparing bankruptcy and debt settlement. Both can help some people, but they work very differently, and it is important to understand the risks before you choose.

What is the difference?

Bankruptcy is a legal process in federal court. For consumers, the two most common types are Chapter 7 and Chapter 13. It can stop many collection actions once a case is filed through something called the automatic stay. That stay usually pauses most lawsuits, wage garnishments, collection calls, and foreclosure actions while the case moves forward.

Debt settlement is not a court process. It usually means trying to negotiate with creditors to accept less than the full amount owed. Sometimes people do this themselves. Sometimes they hire a company or a lawyer to try to negotiate for them. Creditors do not have to agree, and collections may continue while negotiations are happening.

Neither option is "good" or "bad" for everyone. The right path depends on the kind of debt you have, whether you are being sued or garnished, whether you are behind on a mortgage or car loan, your income, your property, and the laws in your state and judicial district.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We give general educational information and can help you connect with a licensed bankruptcy attorney near you to talk through your options.

When bankruptcy may be stronger than debt settlement

Bankruptcy is often worth asking about if you need fast legal protection. If your wages are being garnished, a foreclosure sale is coming, or a lawsuit has already been filed, debt settlement may not move quickly enough. In many cases, filing bankruptcy triggers the automatic stay right away, which can pause most collection activity.

Bankruptcy may also help when the debt is simply too large to settle realistically. If you owe many creditors and cannot keep up, trying to negotiate each account one by one can be slow, stressful, and uncertain. A bankruptcy attorney can explain whether Chapter 7 or Chapter 13 might give broader relief.

That said, bankruptcy does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. Outcomes depend on the facts of the case, and exemption rules vary by state.

If you want a simple overview first, you can read more about bankruptcy chapters or see other common debt situations.

When debt settlement may be considered

Debt settlement is sometimes considered when a person mainly has unsecured debts, such as credit cards, and is not facing an urgent lawsuit, garnishment, or foreclosure. Some people prefer trying to negotiate before considering bankruptcy, especially if they hope to avoid court.

But there are real limits. Creditors can refuse to settle. Some may continue collection efforts or sue. Missed payments during a settlement attempt can hurt your credit further, and interest and fees may keep growing. Forgiven debt can also have tax consequences in some situations, which is one reason it is wise to ask a qualified professional about your specific case.

If someone is promising that settlement will definitely cut your debt to a certain amount or definitely stop collections, be careful. No honest professional should guarantee that. The result depends on the creditors, the timing, and your overall financial situation.

A licensed bankruptcy attorney can often tell you, in one consultation, whether settlement seems realistic or whether bankruptcy may give clearer protection.

Cost: honest ranges, not promises

Many people are afraid to call a lawyer because they think they cannot afford one. In consumer bankruptcy, many attorneys charge a flat fee rather than billing by the hour. The total usually also includes the court filing fee and a small required credit-counseling fee.

Very general ranges: a straightforward Chapter 7 attorney flat fee is often around $1,000 to $2,500, plus the court filing fee and a small credit-counseling fee. A Chapter 13 attorney flat fee is often around $3,000 to $6,000 or more depending on the district, plus the court filing fee and a small credit-counseling fee. These are not quotes, not guarantees, and not the same in every place.

Costs can go up or down based on where you live, how complex the case is, whether there is a business involved, whether there are lawsuits, tax issues, high-value assets, prior filings, or disputes about property or income. Rules and typical fees vary by state and judicial district.

Debt settlement costs vary too, and the total cost can be hard to compare because negotiations may take time and may not succeed with every creditor. Before signing anything, ask exactly what services are included, what happens if no settlement is reached, and whether collections can continue while negotiations are underway.

How to choose carefully

If you are deciding between bankruptcy and debt settlement, slow down and compare the risks, not just the sales pitch. Ask what happens to a lawsuit that is already filed. Ask what happens to a wage garnishment. Ask whether a foreclosure sale can still move forward. Ask which debts would likely remain even after the process ends.

It is also wise to ask about timing. In bankruptcy, legal protection usually begins when the case is filed. In debt settlement, protection is not automatic because it depends on whether creditors cooperate. That difference matters a lot when the pressure is immediate.

Before you hire anyone, confirm that the attorney is licensed in your state and in good standing with the state bar. If you are more comfortable in another language, ask whether interpretation is available. A good attorney should explain your options in plain words and should not shame or rush you.

CleanSlate Match does not file bankruptcy and does not create an attorney-client relationship. We are a free matching service. We only collect contact information and general intent, such as your name, phone, optional email, state, preferred language, and a general sense of your situation. We do not ask for your Social Security number, bank-account numbers, credit-card numbers, or other financial-account details.

A simple next step

If you are overwhelmed, you do not need to decide everything today. A practical next step is to speak with a licensed bankruptcy attorney in your area and ask for an honest comparison of Chapter 7, Chapter 13, and non-bankruptcy options based on your situation.

- Write down the debts causing the most stress: lawsuit, garnishment, foreclosure, credit cards, medical bills, or repossession risk.

- Note any urgent dates, such as a court hearing or sale date.

- Ask whether the automatic stay could protect you if bankruptcy is filed.

- Ask which debts might not be discharged.

- Ask for the attorney's flat-fee range, the court filing fee, and any other expected costs.

- Confirm the attorney's bar license and whether language help is available.

If you want, you can get matched for free with a licensed bankruptcy attorney near you. The goal is not pressure. It is to help you understand your real options and move forward with clear information.

- Free matching service for people in debt

- General educational information only

- Bankruptcy laws and exemptions vary by state and district

Bankruptcy and debt settlement are different tools, and a licensed bankruptcy attorney can help you understand which one truly fits your situation.

Common questions

Is bankruptcy better than debt settlement?

Not always. Bankruptcy can offer stronger legal protection, especially if you are facing a garnishment, lawsuit, or foreclosure, but the right option depends on your debts, income, property, and state law.

Will either option erase all my debt?

No honest source should promise that. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud, and debt settlement depends on whether creditors agree.

Can debt settlement stop a lawsuit or wage garnishment?

Not automatically. Because settlement is not a court process, creditors may still sue or keep collecting unless they choose to stop. Bankruptcy often stops most collection actions once the case is filed through the automatic stay.

How much does it cost to file bankruptcy?

Many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. Very general ranges are often about $1,000 to $2,500 for a straightforward Chapter 7 and about $3,000 to $6,000 or more for Chapter 13, but the real number depends on the case and district.

What does CleanSlate Match do?

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help connect you with a licensed bankruptcy attorney near you and only collect contact information and general intent, not Social Security numbers or account numbers.

I am new to the US and English is hard for me. Can I still get help?

Yes. You can ask for your preferred language when you reach out, and it is reasonable to ask whether interpretation is available. A licensed attorney should explain your options in clear, respectful language you can understand.

Related help

How the automatic stay and Chapter 13 can pause foreclosure and help you keep your home.

Open → Bankruptcy When Your Wages Are Being GarnishedHow filing can stop a garnishment quickly and protect your paycheck.

Open → Bankruptcy When You're Buried in Medical DebtHow bankruptcy treats medical bills and why it's one of the most common reasons people file.

Open →