Guides

What is the automatic stay?

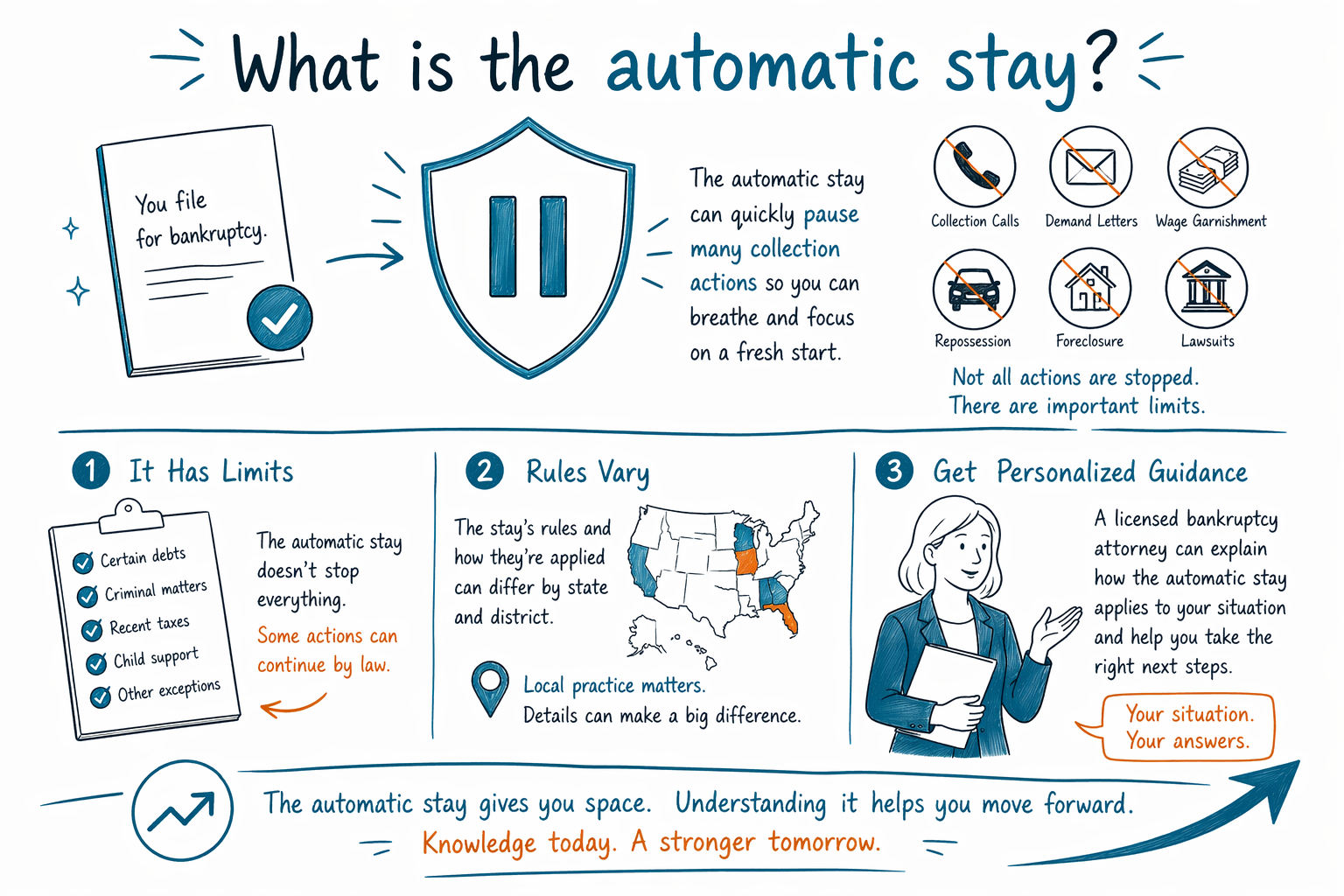

The automatic stay is a legal pause that usually starts the moment a bankruptcy case is filed. It can stop many collection actions quickly, but it does not stop every debt or solve every problem by itself.

The short answer

The automatic stay is a court-ordered stop sign for many creditors after a bankruptcy case is filed. In many Chapter 7 and Chapter 13 cases, it pauses collection calls, letters, lawsuits, wage garnishments, bank levies, and many foreclosure or repossession actions right away.

This is often one of the biggest reasons people look into bankruptcy. If you are being sued, your paycheck is being garnished, or you are behind on your mortgage, the automatic stay may give you breathing room while the case moves forward.

But it is important to be honest about limits. The stay does not erase debt by itself, and bankruptcy does not make every debt disappear. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. Rules also vary by state and federal judicial district, so a licensed bankruptcy attorney in your area is the right person to review your situation.

What the automatic stay usually stops

Once a case is filed, the automatic stay usually stops many common collection actions. Creditors are generally supposed to stop trying to collect from you directly while the stay is in place.

This can include phone calls and demand letters, collection lawsuits, wage garnishments, bank account levies, and many steps in a foreclosure or car repossession. It can also pause some utility shutoff efforts and other collection pressure, depending on the facts.

The key word is usually. Timing matters, the type of debt matters, and repeat bankruptcy filings can change how much protection you get. That is why it helps to speak with a licensed bankruptcy attorney before waiting too long, especially if a foreclosure sale, repossession, or court hearing is close.

What it does not always stop

The automatic stay has real power, but it has limits. It usually does not stop child support collection, many family court matters, criminal cases, or some tax actions. In some situations, a landlord may still be able to move forward with an eviction, especially if a judgment for possession was entered before the bankruptcy was filed.

Creditors can also ask the bankruptcy court for permission to continue certain actions. This is often called asking the court to "lift" the stay. For example, a mortgage lender or car lender may ask for relief from the stay if payments are far behind and the law allows it.

If you have filed bankruptcy before, the stay may be shorter or may not go into effect automatically at all. These repeat-filing rules are technical and can be strict, and they vary by timing and by case history.

How long the stay lasts

In a Chapter 7 case, the automatic stay usually lasts until the case ends, the debt is addressed, or the court lifts the stay for a specific creditor. Chapter 7 is often used to deal with unsecured debts such as credit cards, medical bills, and personal loans, but whether a debt is discharged depends on the facts and the law.

In a Chapter 13 case, the stay can remain in place while you make payments under a court-approved plan, often three to five years. This is one reason Chapter 13 may help people who need time to catch up on mortgage arrears or car payments.

The stay is not the same thing as a discharge. The stay is temporary protection while the case is active. A discharge, when available, is the court order that wipes out certain eligible debts at the end of the process. To learn more about how the chapters work, you can read guides and compare chapters.

Why timing matters if you are facing foreclosure or garnishment

If your wages are being garnished or a foreclosure sale is coming soon, timing can matter a lot. The automatic stay usually starts when the bankruptcy case is actually filed with the court, not when you start thinking about filing and not when you first talk to someone.

That means waiting too long can reduce your options. If a sale date, repossession, or court deadline is close, speaking with a licensed bankruptcy attorney as soon as possible is important. An attorney can explain whether bankruptcy may help, whether Chapter 7 or Chapter 13 fits better, and what deadlines apply in your district.

Many people do keep a home or car in bankruptcy, often through exemptions or through a Chapter 13 repayment plan. But that depends on income, equity, payment history, the type of debt, and local rules. No honest service should promise a specific result before a lawyer reviews the facts.

How CleanSlate Match can help, free

CleanSlate Match is a free matching service. We are not a law firm, not a lawyer, and we do not file bankruptcy or create an attorney-client relationship. We provide general educational information and help connect people with a licensed bankruptcy attorney near them.

If you want, you can get matched for free. We only collect basic contact information and general intent, such as your name, phone number, optional email, state, preferred language, and a general sense of what is going on. We do not ask for a Social Security number, bank account numbers, credit card numbers, or detailed financial account information.

If cost is worrying you, many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. Very general ranges people often see are about $1,000 to $2,500 in attorney flat fees for many Chapter 7 cases and about $3,000 to $6,500 or more for many Chapter 13 cases, depending on the district, complexity, and whether motions or emergencies are involved. Court filing fees are usually a few hundred dollars. These are not quotes, not guarantees, and the real amount can be higher or lower in your area.

When you speak with any attorney, ask for the full fee structure in writing, ask what is included, and confirm the lawyer's state bar license. A calm, honest consultation should help you understand your options without pressure.

The automatic stay can quickly pause many collection actions after a bankruptcy filing, but it has limits, rules vary by state and district, and a licensed bankruptcy attorney can tell you how it applies to your situation.

Common questions

Does the automatic stay stop wage garnishment right away?

It often stops most wage garnishments once the bankruptcy case is filed, but timing matters and there can be exceptions. A licensed bankruptcy attorney can tell you how it usually works in your state and district.

Will the automatic stay stop a foreclosure on my home?

It often pauses foreclosure activity when the case is filed, which can create time to act. But it may not be permanent, and whether you can keep the home depends on the chapter, your payments, your equity, and local rules.

Does the automatic stay erase my debt?

No. The automatic stay is a pause on many collection actions, not a debt cancellation by itself. Some debts may later be discharged in bankruptcy, but some usually survive, including most student loans, recent taxes, child support, alimony, most court fines, and debts from fraud.

Can creditors start collecting again later?

Yes, sometimes. A creditor may ask the court to lift the stay, or the stay may end when the case ends or under repeat-filing rules.

Is CleanSlate Match my lawyer?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We can help connect you with a licensed bankruptcy attorney for advice about your own case.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →