Guides

What is chapter 7 bankruptcy?

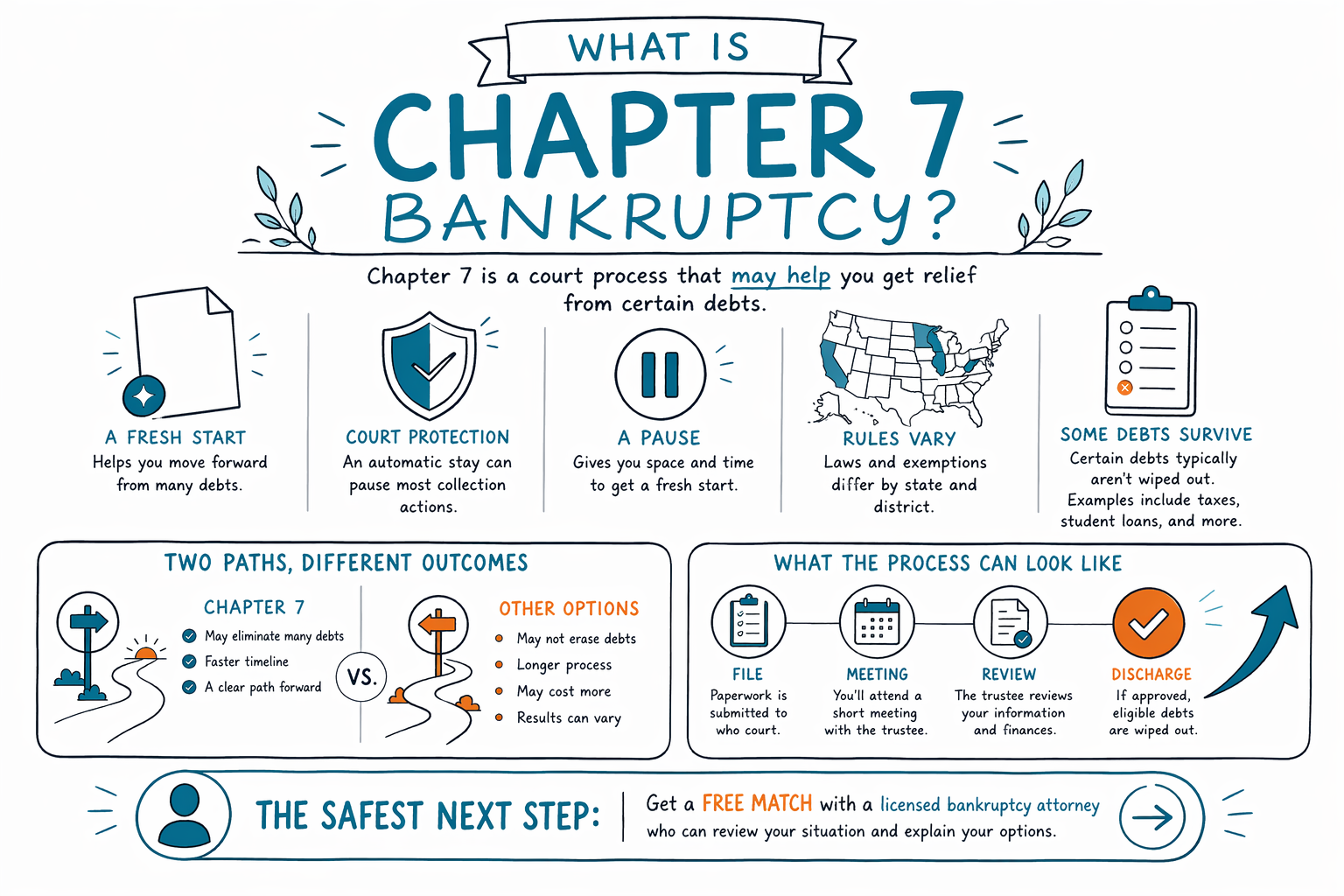

Chapter 7 bankruptcy is a legal process that may help some people get relief from overwhelming debt by wiping out certain unsecured debts. It is not right for everyone, and the rules vary by state and district, so a licensed bankruptcy attorney should review your situation.

What Chapter 7 bankruptcy is

Chapter 7 is often called “liquidation” bankruptcy, but in many consumer cases people do not lose everything they own. In a simple sense, it is a court process that can discharge certain debts when you qualify and complete the case.

People usually think about Chapter 7 when credit cards, medical bills, personal loans, or old collection accounts have become unmanageable. It can also help stop collection activity quickly once the case is filed, because the automatic stay generally pauses most calls, lawsuits, wage garnishments, and foreclosure activity right away.

It is important to know that Chapter 7 does not erase every kind of debt. Debts that often survive include most student loans, recent income taxes, child support, alimony, many court fines, and debts tied to fraud. A licensed bankruptcy attorney near you can explain what may or may not be discharged in your case.

How Chapter 7 usually works

Most cases start with a credit counseling step, then a bankruptcy petition is filed with the court. After filing, the automatic stay usually begins, which is one of the main reasons people seek bankruptcy relief when they are being chased by collectors.

Next, the court and a trustee review the case. The trustee looks at your forms, asks questions at the meeting of creditors, and checks whether any property is protected by exemptions. Exemptions vary by state and judicial district, so what you can keep depends on where you live.

If the case goes smoothly and you are eligible, the court may later enter a discharge for qualifying debts. That discharge is the order that ends your personal legal obligation to pay certain debts.

Who Chapter 7 may help

Chapter 7 is often considered by people whose debts are mostly unsecured and who do not have enough income to manage payments through a long repayment plan. It may be a good fit when the goal is a fresh start rather than reorganizing debt over time.

Some people use Chapter 7 to deal with:

- credit card debt

- medical bills

- personal loans

- old utility bills

- lawsuit judgments in some situations

It may also help if you are facing aggressive collection efforts and need a fast legal pause while you get your footing. But whether Chapter 7 is available, and whether it is the best option, depends on income, property, recent financial history, and state-specific rules.

What Chapter 7 can and cannot do

Chapter 7 can give many people real breathing room, but it has limits. It does not automatically stop every problem forever, and it does not remove every obligation.

Here is the practical version:

- It can discharge many unsecured debts.

- It can usually stop most collection activity once filed.

- It may let you keep protected property through exemptions.

- It does not usually erase child support, alimony, most recent taxes, most student loans, or debts involving fraud.

Also, if you are behind on a mortgage or car loan, Chapter 7 may help with the unsecured part of the debt, but it may not let you keep the property unless you can stay current or otherwise resolve the loan. A local attorney can explain the real options before you file.

Chapter 7 vs. Chapter 13

Chapter 7 is usually faster and is designed to discharge qualifying debt. Chapter 13 is a repayment plan that may help people catch up on mortgage arrears, car loans, or other debts over time.

If you are behind on a house payment or facing foreclosure, Chapter 13 may sometimes be the better tool. If your income is too low for a repayment plan and your debt is mostly unsecured, Chapter 7 may be the more practical choice. The right answer depends on your income, property, and the protections available in your state.

If you want a plain overview of both chapters, you can also read our chapter guides or start with general bankruptcy basics.

What it may cost

Most consumer bankruptcy attorneys charge a flat fee for Chapter 7, plus the court filing fee and a small required credit-counseling fee. The total can vary based on the complexity of the case and the district where you file.

As a general educational range, many Chapter 7 cases involve attorney fees that may be in the low thousands of dollars, plus the court filing fee and counseling cost. That is not a quote, and real pricing depends on your location and circumstances.

CleanSlate Match is free for the person seeking help. Participating attorneys pay a flat fee to take part in the service, and you can get matched with a licensed bankruptcy attorney near you by using get matched.

Chapter 7 is a court process that may help you get relief from certain debts, but the rules vary by state and district, some debts survive, and the safest next step is a free match with a licensed bankruptcy attorney.

Common questions

Will Chapter 7 erase all my debt?

No. Chapter 7 can discharge many unsecured debts, but some debts usually survive, including most student loans, recent income taxes, child support, alimony, many fines, and debts involving fraud. A lawyer in your area can tell you what applies in your case.

Can I keep my house or car?

Sometimes, yes, but not always. Whether you can keep property depends on exemptions, the type of debt, whether you are current on payments, and the rules in your state and district.

Will creditors stop calling if I file?

Usually, most collection activity pauses when the case is filed because of the automatic stay. There are exceptions, so if you have an urgent garnishment, lawsuit, or foreclosure issue, speak with a licensed bankruptcy attorney right away.

How do I know if I qualify?

Eligibility depends on several factors, including income, recent financial history, property, and the means test rules in your area. Because the rules vary by state and district, a local attorney is the best person to review your situation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →