Guides

What is a reaffirmation agreement?

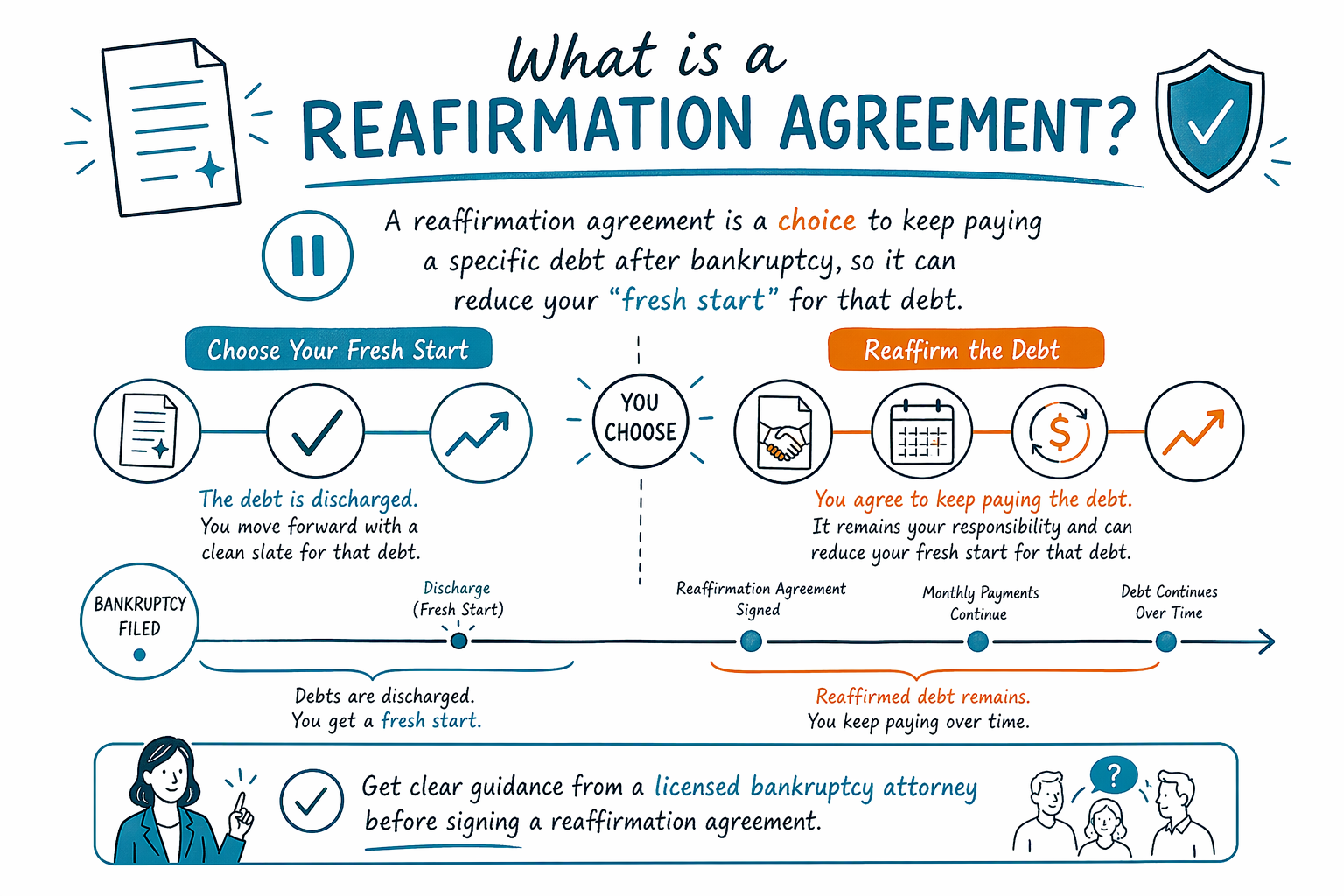

A reaffirmation agreement is a paperwork agreement in bankruptcy where you promise to keep paying certain debts after your bankruptcy ends. It’s optional, not automatic, and it can affect whether you’ll have a clear “fresh start” on that specific debt.

Quick answer: what it is (and what it isn’t)

A reaffirmation agreement is an official contract filed with the bankruptcy court that says you will continue paying a specific debt—usually a car loan or certain secured debts—even though bankruptcy normally helps with a “discharge.”

It’s not the same as “keeping the item by default.” In many cases, you can choose to keep paying under a reaffirmation, but you also may be able to keep the property through other options (like a Chapter 13 repayment plan) depending on your situation.

CleanSlate Match can explain the general process, but this is educational information only—not legal advice, not a guarantee of any outcome, and rules can vary by state and federal district. A licensed bankruptcy attorney can explain what’s usually available in your area.

If you want to understand the bigger picture first, you can start with our bankruptcy chapter guide.

Why reaffirmation agreements exist

Many people use reaffirmation agreements when they want to keep an item (commonly a car) and also want the lender to have stronger confidence they’ll keep receiving payments after bankruptcy.

If a debt is reaffirmed, you are essentially agreeing that you will still be responsible for that debt if you default later—even after the bankruptcy case ends.

This is why reaffirmation is a decision with real consequences. For some people it helps them keep the asset. For others, it may make the “fresh start” smaller for that particular debt.

A bankruptcy attorney will look at your income, your ability to keep paying, the debt type, and whether keeping the item is possible without reaffirming.

How reaffirmation works in the bankruptcy process (general steps)

In most situations, a reaffirmation agreement is offered for a specific debt and is filed with the court as part of (or near) the bankruptcy case.

Often, you’ll review the agreement to confirm details like the amount, payment terms, and what happens if you can’t pay. The court typically reviews reaffirmation paperwork to help ensure the agreement is understood and appropriate.

Important: you do not have to sign a reaffirmation agreement in every case. Whether reaffirmation is available—and whether you should consider it—depends on your bankruptcy chapter, the debt type, and your situation.

Because details vary, a free attorney match can connect you with a licensed bankruptcy attorney near you who can explain the real-world options for your case.

Common pros and cons (know what you’re trading)

Possible reasons someone may consider reaffirming include:

- Keeping a car or other property when the lender might otherwise be able to repossess or the payment plan is unclear

- Reducing the lender’s uncertainty about repayment after bankruptcy

- Avoiding a situation where the debt is discharged but you still need reliable access to the item

Possible downsides include:

- You may still be legally responsible for the debt after your bankruptcy ends

- If you later miss payments, the lender may have more options to collect compared to a discharged debt

- The reaffirmed obligation can limit the benefit of discharge for that specific debt

The safest way to decide is to talk with a licensed attorney about your budget and which debts would survive without reaffirmation and which might not. Rules and practices vary by district and state.

What bankruptcy usually does not erase (and why reaffirmation matters)

A key limit to understand: bankruptcy does not automatically wipe out every type of debt. Some obligations usually survive bankruptcy, including most student loans (unless a rare exception applies), most recent income taxes, child support and alimony, many court-ordered fines/penalties, and debts from fraud or certain wrongdoing.

Whether a particular debt survives can depend on facts and timing. That’s one reason a reaffirmation can be such a high-stakes choice: reaffirming may keep you responsible for a debt that could otherwise be discharged.

Also, reaffirmation decisions can interact with how you’re handling secured debts and whether you’re in Chapter 7 or Chapter 13. Educationally, Chapter 13 often involves making payments under a court-approved plan, while Chapter 7 generally focuses on discharge (subject to exemptions and eligibility rules like the means test).

For a clear overview, see what Chapter 7 vs Chapter 13 means.

Cost and next steps: get clear answers before you sign anything

Be cautious about signing anything you don’t fully understand. Reaffirmation agreements can require review and may require the court’s attention, depending on your case.

Before committing, ask a licensed bankruptcy attorney to explain: (1) whether reaffirmation is even recommended in your situation, (2) which debts are likely to be discharged, and (3) what happens if you don’t reaffirm.

Attorney costs vary by chapter, district, and case complexity. Many consumer bankruptcy attorneys charge a FLAT FEE (not hourly), plus the court filing fee and a small required credit-counseling fee. Typical total costs often fall in ranges such as:

- For Chapter 7: roughly $300 to $1,500 for court-related fees and required counseling, plus an attorney flat fee that can bring the overall range higher (commonly somewhere around $1,500 to $3,500, depending on the district and complexity).

- For Chapter 13: the attorney flat fee and additional administrative requirements often make the overall cost higher (often commonly around $2,500 to $6,000 total, depending on the district and how complex the plan is).

Ranges are not quotes, and your final cost depends on your chapter and circumstances—only an attorney who reviews your case can estimate accurately.

If you’re overwhelmed right now, you can get matched for free with a licensed bankruptcy attorney near you through CleanSlate Match. You can also confirm the attorney is licensed in your state before discussing legal steps.

A reaffirmation agreement is a choice to keep paying a specific debt after bankruptcy, so it can reduce your “fresh start” for that debt—get clear guidance from a licensed bankruptcy attorney before signing.

Common questions

Is a reaffirmation agreement required in bankruptcy?

No. Reaffirmation is usually optional. Whether it’s offered or appropriate depends on your case, the debt type, and what you’re trying to accomplish.

If I sign a reaffirmation agreement, does that mean the debt will be paid no matter what?

Signing generally means you stay responsible for that specific debt after the bankruptcy ends. If you later can’t pay, the lender may be able to pursue you for collection. Your attorney can explain the realistic risks for your situation.

Can reaffirmation help me keep my car?

Sometimes. People often consider reaffirmation with secured debts like car loans, especially if they want to keep the vehicle and continue making payments. But there may be other options too, depending on your bankruptcy chapter and local practice.

Will bankruptcy discharge a car loan or other secured debt?

Often, secured debts work differently than unsecured credit cards. Outcomes depend on your chapter, whether you keep or surrender the property, your district rules, and local practice. A licensed bankruptcy attorney can explain what’s likely for your specific debt.

Does reaffirmation affect other debts in my case?

Usually it only applies to the specific debt(s) you reaffirm. Other debts may be discharged or may survive depending on their type and the details of your case.

Are reaffirmation rules the same in every state?

No. Bankruptcy is federal law, but courts and state-related rules (and district practice) can affect how things work. Always confirm with a licensed bankruptcy attorney in your state.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →