Guides

Does my spouse have to file too?

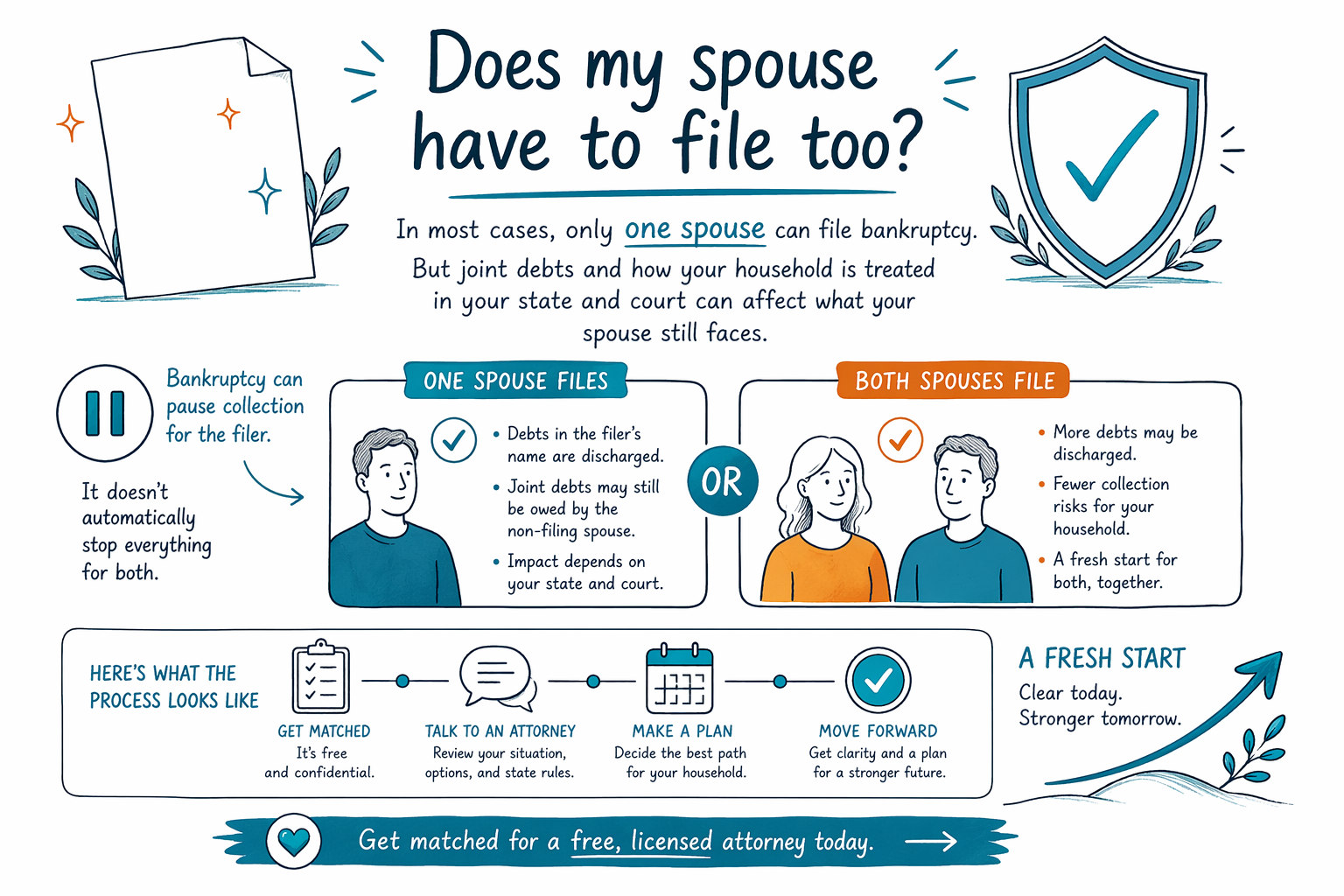

In many consumer bankruptcy cases, only one spouse files. But whether your spouse must (or should) file depends on debts, income, and how the bankruptcy chapter affects your household—so it’s important to talk with a licensed attorney near you.

Quick answer: Does your spouse have to file too?

Usually, no. In most Chapter 7 or Chapter 13 consumer cases in the US, you can file by yourself even if you’re married.

That said, some situations may strongly affect whether your spouse should file too, or whether certain debts will still be collectible from your spouse after your case is over. A local, licensed bankruptcy attorney can explain what applies to your specific facts in your state and court district.

CleanSlate Match is a FREE matching service—we can help you connect with a licensed bankruptcy attorney near you. We’re not a law firm, and we don’t file bankruptcy or give legal advice.

- If only you file, your case affects you (and your assets/exemptions) directly, but may not automatically protect your spouse from all creditor actions.

- If your debts are joint (shared), both your bankruptcy and your spouse’s choices can matter.

Why the answer can change: joint debts, separate debts, and your household finances

Bankruptcy can only directly address the debts and legal position of the person who files. If your spouse is not a debtor in the case, creditors often look to your spouse to satisfy certain debts—especially debts that are legally tied to them.

Common examples where your spouse’s situation matters:

- Credit cards or personal loans taken out jointly

- A mortgage or car loan where both names are on the account

- Medical bills or other bills where you and your spouse are both responsible

Also, chapters like Chapter 13 involve a repayment plan based on household income and requirements. Even when your spouse doesn’t file, their income or the way your household is counted can affect what’s required in your plan. The details vary by state and by the bankruptcy court that serves your area.

- Joint accounts are often the biggest reason attorneys discuss filing for both spouses—or leaving it to one spouse.

- If your spouse has separate debts, those may still be pursued unless they also file.

Chapter 7 vs. Chapter 13: how spouse decisions play out

Chapter 7 is often focused on whether you qualify under the means test and whether there are non-exempt assets that could be used to pay creditors. If only one spouse files, the case generally covers that spouse’s debts and that spouse’s assets, protected by exemptions, according to your state’s rules.

Chapter 13 is different. It’s a court-approved repayment plan, usually designed around a household’s ability to pay over time. If your spouse is not included as a debtor, your attorney will still need to consider how household finances are treated for plan requirements and whether certain debts should be handled differently.

In both chapters, your attorney will also look at how creditors have been collecting so far—letters, lawsuits, garnishments, or foreclosure notices—because the “best” strategy can depend on the type of debt and how it’s enforced.

- Either chapter can be possible with one spouse filing, but the plan details and creditor treatment can differ.

- Local rules and how your court interprets household information can change the outcome.

Important limits: what bankruptcy can’t erase for everyone

It’s understandable to want a simple answer like “bankruptcy will stop everything.” But the truth is more careful: bankruptcy can often discharge certain consumer debts, yet some categories of debt usually survive. Outcomes depend on the specific case and the type of obligation.

Common debts that often cannot be erased (or may require a special challenge) include:

- Most student loans (usually not discharged the same way as credit cards)

- Recent income taxes that meet certain time/rule requirements

- Child support and alimony

- Many court fines/penalties

- Debts tied to fraud or intentional wrongdoing

Even in cases where your own debts may be reduced or discharged, your spouse may still face collections on debts that are not part of your spouse’s bankruptcy (for example, separate debts or certain joint obligations). A licensed attorney can explain what will likely stop and what may not—no promises, just honest expectations.

- If your spouse doesn’t file, your spouse may not get the same legal protections as you do from the moment your case is filed.

- Your local attorney can explain how “joint” vs. “separate” responsibility affects creditor actions.

What you can do next (no pressure): get matched to a licensed attorney

You don’t have to navigate this alone. A good first step is to talk with a licensed bankruptcy attorney in your area to confirm whether filing one spouse-only makes sense for your debts and household situation.

CleanSlate Match is FREE for you. We ask for limited contact and general intent only (name, phone, optional email, state, a general sense of the situation, and your preferred language). We do not ask for Social Security numbers, bank-account numbers, or account balances.

To learn more about the basics, you can review our chapter guide and learn more guides. When you’re ready, use get matched to connect with a licensed bankruptcy attorney near you for an individualized consultation.

- Confirm the attorney is licensed in your state (and the relevant federal court) before meeting.

- Bring a short list of the debts you share and the debts that are only in your name.

Costs and fees: what to expect when you ask about “both spouses”

Attorney fees vary by case complexity, chapter type, and the court district, so any numbers you see online should be treated as estimates—not quotes. Many consumer bankruptcy attorneys charge a flat fee for representation, plus the required court filing fee and a small required credit-counseling fee.

For consumer cases, flat attorney fees often fall in a broad range (commonly roughly $1,000–$3,500+), plus court costs (often a few hundred dollars) and the required credit-counseling fee (typically in the range of tens of dollars). Fees may be higher if there are multiple people to represent, complicated schedules, recent transfers, a foreclosure/eviction timeline, or disputed issues.

If your attorney discusses whether both spouses should file, ask how that changes the attorney work and whether the flat fee changes. CleanSlate Match does not charge you anything and does not take a share of your debt or any percentage of attorney fees. The most reliable way to understand your cost range is to ask a licensed attorney after a brief review of your situation.

- Ranges can vary widely—your district and case complexity matter.

- A quick, honest consultation is the safest way to confirm strategy and expectations.

In most cases, only one spouse can file bankruptcy, but joint debts and how your household is treated in your state and court can affect what your spouse still faces—get matched for a free, licensed attorney consult to confirm.

Common questions

If I file bankruptcy, will my spouse automatically be protected too?

Usually, no. Your bankruptcy generally protects the person who files and their assets and debts. If your spouse is not part of the case, creditors may still pursue your spouse—especially for debts that are legally tied to your spouse or for separate debts.

What if we have joint credit cards or a joint mortgage—should we both file?

Joint debts often make the decision more complicated. Sometimes only one spouse files; other times attorneys recommend filing for both spouses. The best choice depends on who owes what, your chapter (Chapter 7 or 13), and local rules.

Does Chapter 13 require my spouse’s income even if they don’t file?

It can. Chapter 13 eligibility and plan requirements may involve household income and how income is treated in your district. An attorney can explain how your specific household situation is counted.

If my spouse doesn’t file, can creditors keep garnishing their wages or pursuing them in court?

They may be able to, depending on the type of debt and whether your spouse is included in the bankruptcy case. Many collections are paused for the debtor once a bankruptcy case is filed, but that pause may not automatically extend to a spouse who is not part of the case.

Can bankruptcy erase our debts and “fix everything” in one step?

Bankruptcy may discharge many types of consumer debt, but not all debts usually disappear. Some debts commonly survive, such as many student loans, certain recent income taxes, child support/alimony, many fines/penalties, and debts tied to fraud. Your attorney can explain what is likely to be dischargeable in your specific case.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →