Guides

Can i file bankruptcy on just one debt?

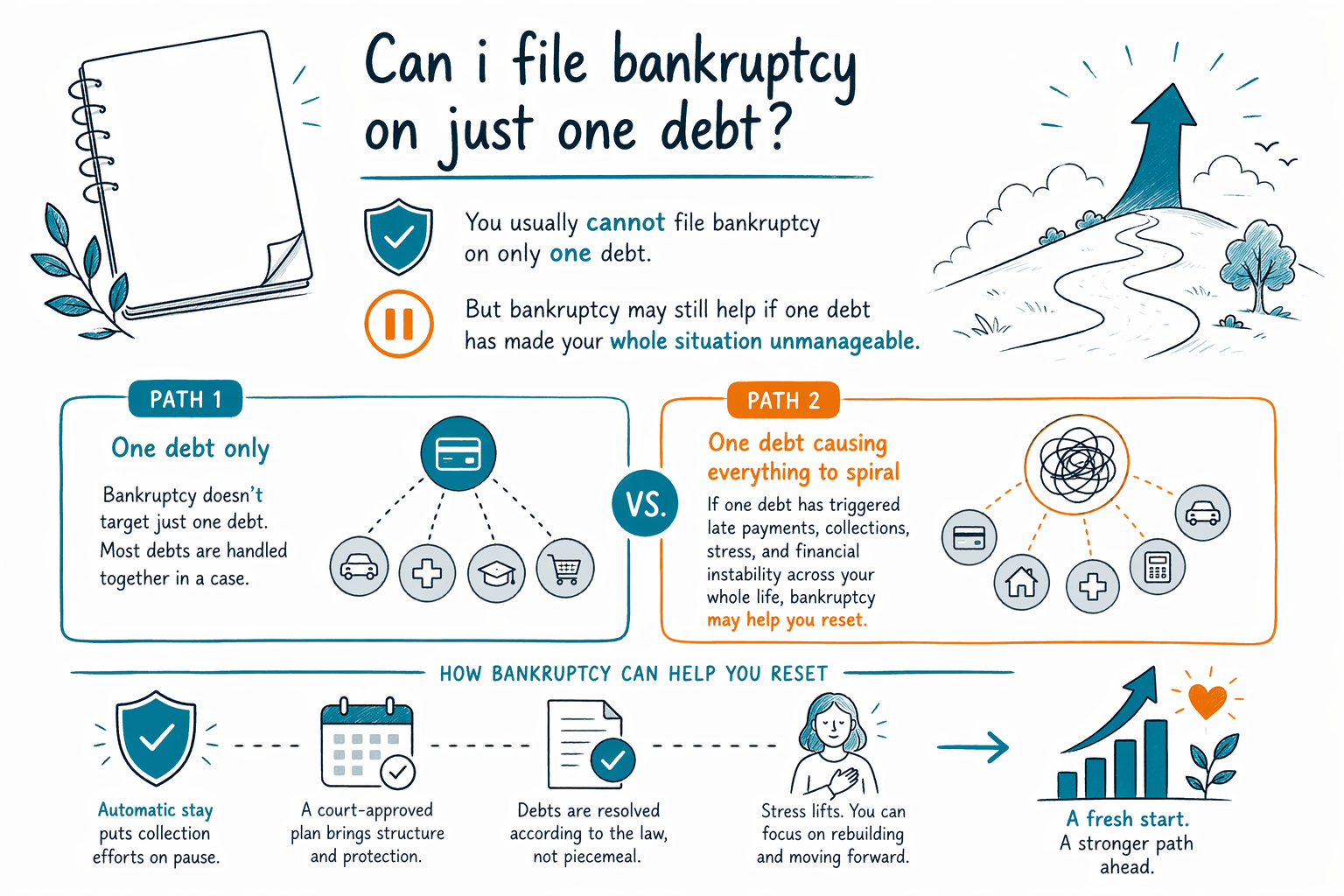

Usually, no. Consumer bankruptcy is meant to deal with your overall financial situation, not let you pick just one debt to erase while keeping the rest untouched.

Short answer: usually not the way people hope

In most consumer bankruptcy cases, you do not file "on just one debt" the way you might settle or dispute a single bill. When a Chapter 7 or Chapter 13 case is filed, you generally must list all of your debts, your property, your income, and your regular expenses. The court and trustee look at the full picture.

That does not mean every debt will be erased. Some debts are often dischargeable, and some usually are not. Most student loans, recent income taxes, child support and alimony, most court fines, and debts caused by fraud often survive bankruptcy. The result depends on the facts of the case.

Bankruptcy laws, exemptions, local procedures, and the means test vary by state and judicial district. This page is general educational information only, not legal, tax, or financial advice. A licensed bankruptcy attorney in your area can tell you how the rules apply to your situation.

Why bankruptcy usually includes all your debts

Bankruptcy is designed to be a complete legal process. If you file, you usually must disclose all creditors, not just the one causing the most stress right now. For example, if one credit card sued you or one medical bill went to collections, you still generally list your other debts too.

The reason is fairness and transparency. The court does not let people secretly leave out debts, income, or assets to shape the outcome. In a Chapter 7 case, the trustee reviews the whole financial picture. In a Chapter 13 case, your repayment plan is also based on the full picture.

Sometimes people ask this question because they really mean something else: "Can bankruptcy help me with the one debt that is hurting me most right now?" Often, the answer may be yes. If a case is filed, the automatic stay usually stops most collections right away, including many lawsuits, wage garnishments, foreclosures, and collection calls. But the case still involves all required debts and disclosures, not just one.

When one debt is the main problem

Even though you usually cannot file only against one debt, many people consider bankruptcy because of one crisis debt: a judgment, a wage garnishment, a foreclosure, a repossession, a large medical bill, or a tax problem. Bankruptcy may still help if that one debt has pushed everything else out of balance.

For example, someone may be current on most bills but unable to survive a wage garnishment. Another person may be okay on credit cards but behind on the mortgage after an illness. In those situations, a Chapter 7 or Chapter 13 case may offer broader relief than trying to fight one collector alone.

Which chapter may fit depends on income, assets, arrears, the means test, and what you are trying to protect. You can learn more in our guides and compare the main chapters. A local bankruptcy attorney can explain whether bankruptcy is even the right tool, or whether a non-bankruptcy option may make more sense.

What bankruptcy can and cannot do

Bankruptcy can be powerful, but it has limits. If a case is filed, the automatic stay usually pauses most collection activity immediately. That can include many garnishments, lawsuits, bank levies, foreclosure actions, and collection calls. Many people also keep their home or car through exemptions, by staying current, or through a Chapter 13 plan that helps catch up over time.

But bankruptcy does not magically erase every money problem. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most criminal or court fines, and debts tied to fraud or certain intentional wrongdoing. Secured debts like car loans and mortgages also involve the property itself, so whether you keep the property depends on several rules and choices.

It also matters that bankruptcy can affect your credit and may require careful timing. If you transfer property, repay relatives, or leave out information, that can create serious problems. That is one reason it is smart to speak with a licensed bankruptcy attorney before filing anything.

What are the alternatives if it really is just one debt?

If your problem truly is one debt and the rest of your finances are stable, bankruptcy may not be the first option to explore. Depending on the debt, some people look at settlement, a payment plan, defending a lawsuit, asking for hardship relief, or negotiating directly with the creditor. Those options have risks too, and they do not stop every collection action the way a filed bankruptcy case often does.

A good attorney will not push bankruptcy if another option seems better. In a first consultation, many consumer bankruptcy lawyers will ask whether the issue is one debt or a bigger pattern: multiple past-due bills, judgments, lawsuits, repossession risk, foreclosure risk, or a garnishment that makes normal life impossible.

If you are not sure where you stand, that is okay. You do not need perfect English or a full legal vocabulary to ask for help. Start with the plain facts: what kind of debt it is, whether you were sued, whether wages are being taken, and what state you live in.

How to get help, what it may cost, and what CleanSlate Match does

CleanSlate Match is a free matching service, not a law firm, not a lawyer, and not your attorney. We do not file bankruptcy cases or give legal advice. We help connect people with a licensed bankruptcy attorney near them for a consultation.

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. Very general ranges people often see are around $1,000 to $2,500 in attorney's fees for many Chapter 7 cases, and around $3,000 to $6,500 or more for many Chapter 13 cases, depending on the district, the lawyer, and the complexity. Court filing fees are separate and are commonly a few hundred dollars. These are not quotes, and the real number depends on your chapter, your location, and issues like business income, home equity, tax debt, prior filings, lawsuits, or missing records.

If you want to get matched, the service is free for you. We only collect contact details and general intent, such as your name, phone number, optional email, state, general situation, and preferred language. We do not ask for a Social Security number, bank-account numbers, credit-card numbers, or detailed account balances. If you move forward with any lawyer, confirm that the attorney is licensed in your state and in good standing with the state bar.

- Tell us a little about your situation at get matched.

- We try to connect you with a licensed bankruptcy attorney near you.

- Ask whether bankruptcy makes sense for your full situation, not just one debt.

- Ask about likely chapter options, what debts may survive, and the attorney's flat fee and court costs.

- Confirm the attorney's bar license before you hire anyone.

You usually cannot file bankruptcy on only one debt, but bankruptcy may still help if one debt has made your whole situation unmanageable.

Common questions

Can I choose just one credit card or one medical bill to put in bankruptcy?

Usually no. In a consumer bankruptcy case, you generally must list all of your debts and give a full picture of your finances, even if one bill is the main reason you are seeking help.

If I file, will that stop a wage garnishment or lawsuit over one debt?

Often yes, if a bankruptcy case is actually filed. The automatic stay usually stops most garnishments, lawsuits, and other collection activity right away, but there are exceptions and timing matters.

What if I only have one big debt and everything else is okay?

Bankruptcy may or may not be the best tool. Sometimes a payment plan, settlement, or defense to a lawsuit may be worth discussing, but only a licensed attorney who knows your state and district rules can evaluate that.

Will bankruptcy erase student loans or child support?

Usually not. Most student loans, child support, alimony, recent income taxes, most court fines, and some fraud-related debts often survive bankruptcy.

How much does it usually cost to file bankruptcy?

Many consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. Very general ranges are often about $1,000 to $2,500 for many Chapter 7 cases and about $3,000 to $6,500 or more for many Chapter 13 cases, but that depends on your location and case complexity, and these are not quotes.

What does CleanSlate Match do?

CleanSlate Match is a free matching service. We are not a law firm and not your lawyer; we help connect you with a licensed bankruptcy attorney near you so you can get advice about your own situation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →