Guides

Bankruptcy and Your Credit Score

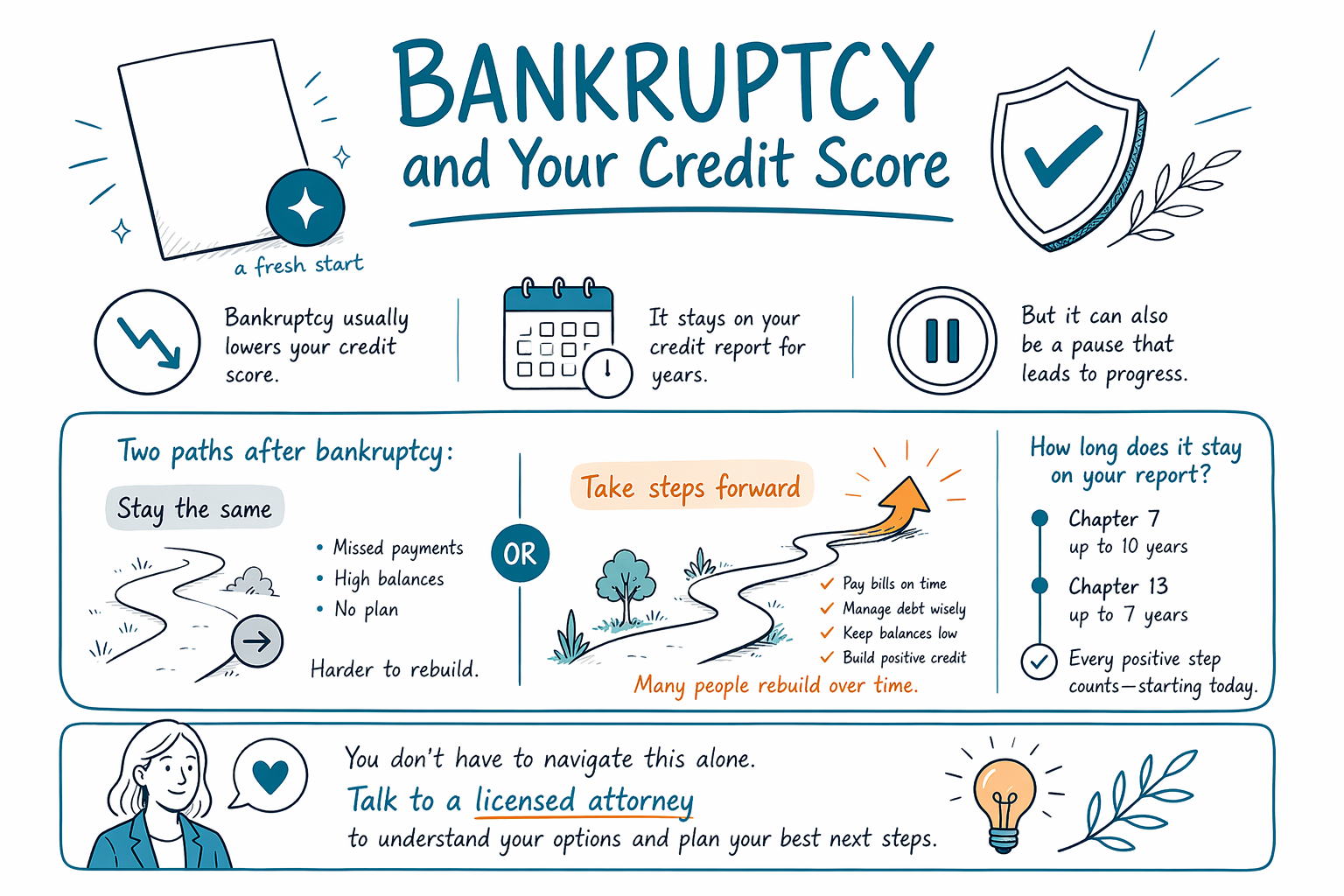

Bankruptcy can affect your credit score and your credit report for years, but it does not mean you can’t rebuild. Here’s what usually happens, what tends to improve, and how to make a plan with a licensed attorney.

The direct answer: will bankruptcy “ruin” your credit?

Bankruptcy typically hurts your credit score at first and stays on your credit report for a long time. That said, the impact is often less permanent than people fear—many people rebuild step by step after they get breathing room from overwhelming debt.

What matters is what you do next. Even with a bankruptcy filing on your record, you can still qualify for certain credit products over time and improve your score by making consistent, on-time payments and keeping balances low where possible.

Rules and timelines can vary depending on your state and the federal district your case is filed in, and credit reporting practices can also differ by credit bureau. A licensed bankruptcy attorney can explain how your specific situation may play out.

How long bankruptcy stays on your credit report

In general, Chapter 7 bankruptcy stays on credit reports for about 10 years, and Chapter 13 stays for about 7 years. Different credit bureaus may reflect the information slightly differently, and your individual report may include other factors like late payments or collections.

Your credit score is not calculated the same way for everyone, but most scoring models treat bankruptcy as a serious negative item. The score impact often lessens gradually as you build a pattern of reliable payments after filing.

If your current credit report already reflects missed payments, collections, or a lawsuit, the “damage” may already be done. Bankruptcy is often a way to stop the bleeding and create a clear path forward, not a magic eraser.

What really happens to your credit score after you file

Many people see their score drop after a bankruptcy is filed because lenders and scoring models view it as a high risk signal. That drop can be sharper if your credit was already damaged.

After the filing, your score can improve over time if you avoid new late payments. In some cases, you may be able to keep or manage certain accounts, depending on the type of bankruptcy and the specific creditor terms (your attorney can walk you through what typically happens in your situation).

It’s also common to get “pre-approval” offers right after bankruptcy. Be cautious and read carefully—some offers have high fees or terms that can make things harder if you’re already stretched.

Chapter 7 vs. Chapter 13: does one hurt credit more?

Both Chapter 7 and Chapter 13 can affect your credit. The main difference is how the case resolves your debts.

In Chapter 7, many eligible unsecured debts are discharged, and the bankruptcy process is usually shorter. Chapter 13 involves a court-approved repayment plan over time, and you typically make monthly payments while the plan is in effect.

Because credit score impact depends on your starting point and your ongoing payment history, there isn’t a single “best” choice for your credit. The best chapter depends on eligibility (including the means test for Chapter 7), your income, your debts, and your goals—like whether you’re trying to keep a home or stop certain actions. To understand the differences in your area, see our chapter guide.

Important limits: bankruptcy doesn’t erase every type of debt

Bankruptcy can remove or reduce many debts, but it does not erase everything. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, many court fines and penalties, and debts based on certain types of wrongdoing (like fraud). Outcomes depend on the specific facts of your case.

Because you may still owe some balances after bankruptcy, your credit rebuilding plan should include how you’ll handle the debts that usually remain—plus staying current on any ongoing obligations.

Also, while bankruptcy can pause many collection actions after the case is filed, it does not guarantee every creditor will stop immediately or that every debt will be handled the same way. For decisions about what you may be able to keep or discharge, confirm details with a licensed bankruptcy attorney near you.

How to rebuild credit in a safe, realistic way

Rebuilding usually looks like: staying on top of payments, keeping new credit use modest, and choosing credit products you can realistically manage. Start with the basics—pay everything you must on time and avoid taking on new debt you can’t afford.

Some people use secured credit cards or credit-builder loans after bankruptcy, but terms vary widely. If you do consider a new credit product, look for clear fees, manageable monthly payments, and automatic reminders so you don’t miss due dates.

If you’re unsure what to do first, it can help to talk with a licensed attorney about what happens to your specific accounts during bankruptcy. Then, after filing (or while you’re deciding), ask the attorney or a qualified credit counselor for general guidance on next steps. For more on getting help, you can start here: get matched and review guides.

- Check your credit reports for accuracy after filing and before you apply for new credit

- Avoid “credit repair” promises—look for honest steps you can take consistently

Talk to a licensed bankruptcy attorney (and confirm the basics)

CleanSlate Match is a FREE matching service that connects you with a licensed bankruptcy attorney near you. We are not a law firm and we do not file bankruptcy, and you won’t become our client through this process.

Rules vary by state and by the federal district where your case is filed, and credit reporting timelines and impacts can vary too. A licensed attorney can explain how your situation may affect your credit and what you can and can’t expect regarding discharge.

If cost comes up, many consumer bankruptcy attorneys charge a flat fee plus the court filing fee and a small required credit-counseling fee. The total often ranges roughly from a few thousand dollars up to around $3,500–$6,000 (depending on chapter, complexity, and district). These ranges aren’t quotes—only a lawyer can estimate based on your case. Be wary of anyone who promises guaranteed results.

Bankruptcy usually lowers your credit score and stays on your report for years, but with a fresh start and careful next steps, many people can rebuild over time—talk to a licensed attorney to understand your real options in your state.

Common questions

Will my credit score go back to normal after bankruptcy?

Your credit score may improve over time, especially if you keep accounts current and avoid new late payments. However, “back to normal” depends on your starting point and your post-bankruptcy habits, and the bankruptcy record can remain for years.

Does Chapter 13 help my credit more than Chapter 7?

Chapter 13 can involve showing consistent repayment through a court plan, which may help some people rebuild. But the impact is still personal—your current credit history, your plan payments, and what creditors do all affect the outcome.

Can bankruptcy stop collections, garnishments, or foreclosure?

In many cases, once a bankruptcy case is filed, an automatic stay pauses many collection actions, including many foreclosures, wage garnishments, and certain lawsuits. Specific results depend on your facts and timing, so confirm details with a licensed bankruptcy attorney.

Will bankruptcy erase student loans or back taxes?

Usually, most student loans and many recent income taxes do not get erased through standard consumer bankruptcy. Some debts may be discharged in limited situations, but that depends on the facts. An attorney can review what applies to you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →