Guides

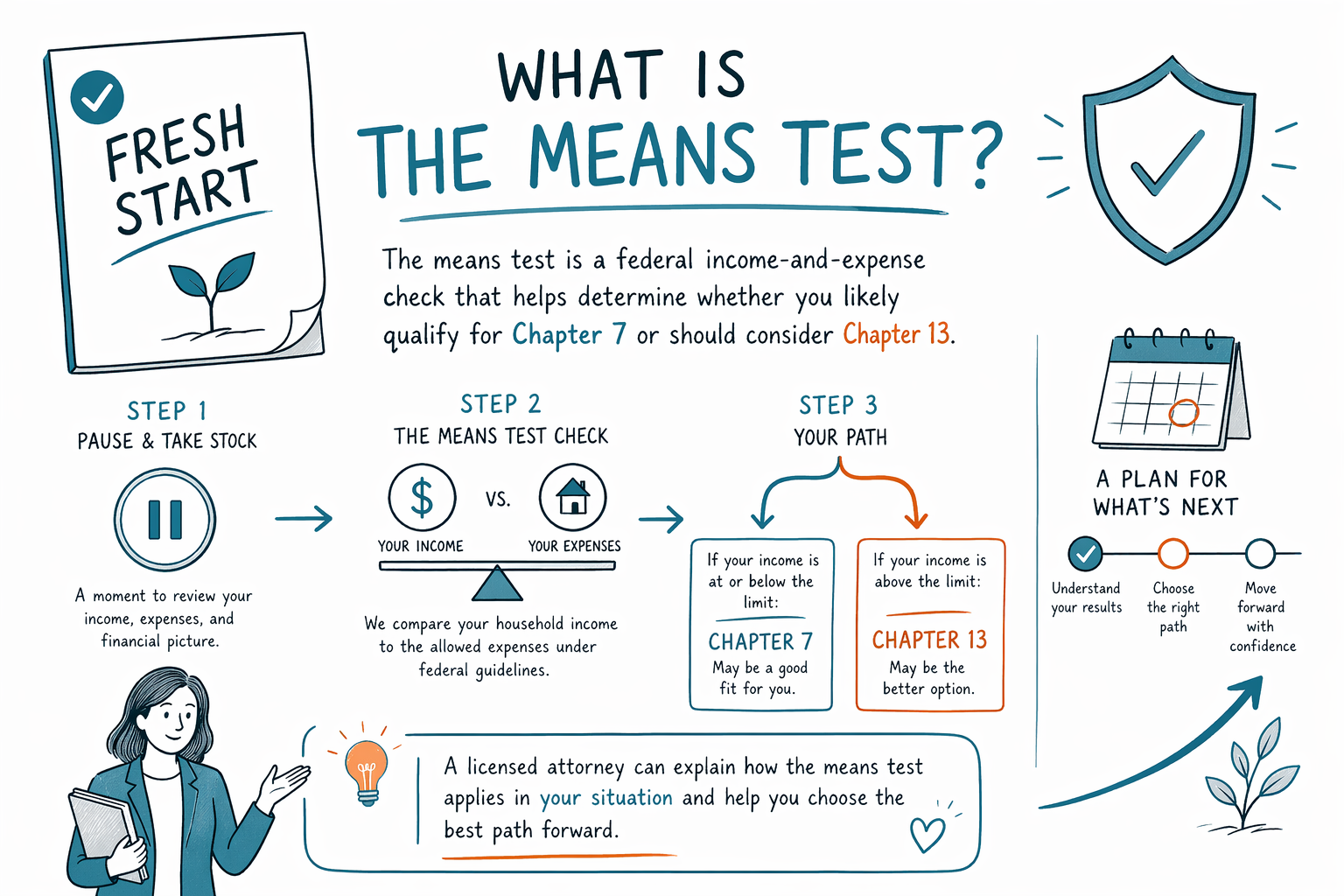

What is the means test?

The means test is a federal screening tool used in some consumer bankruptcy cases to see whether you qualify for Chapter 7 or should instead consider Chapter 13. It’s a process, not a judgment—and you can learn how it works.

The means test: what it is (and what it isn’t)

The means test is a math-based review required in many Chapter 7 bankruptcy filings for individuals. The goal is to check whether your income is low enough to qualify for Chapter 7 relief under federal rules.

It is not the same as “can you afford your debts?” Bankruptcy courts use specific formulas and allowed expenses. Also, the means test is not a guarantee of results—your full situation still matters.

Rules about the form, thresholds, and some details can vary by state and by the court (district). A licensed bankruptcy attorney in your area can confirm how the rules apply in your specific case.

- Means test mainly affects Chapter 7 eligibility

- It uses federal formulas and allowed expense categories

- How it applies can differ by state and judicial district

Why the means test exists

Congress created the means test to help decide which chapter is more appropriate for your income level. In general, Chapter 7 is designed for people with debts they can’t realistically pay back, while Chapter 13 is designed for people who can make a plan payment over time.

If the means test shows your income is above the relevant limit, the court may require you to file Chapter 13 instead of Chapter 7, or you may need to explain special circumstances.

Even when the means test points toward Chapter 13, that does not mean you “failed.” Many people use Chapter 13 to catch up on a mortgage, stop certain collection actions, and reorganize debts in a structured way.

Chapter 7 vs. Chapter 13 (how the means test fits in)

Chapter 7 is often called “liquidation” bankruptcy. In many cases, eligible debts may be discharged, meaning they’re wiped out legally—though not all debts can be erased. Whether you qualify depends partly on the means test in many situations.

Chapter 13 is “reorganization.” Instead of trying to discharge as quickly as possible, you usually propose a repayment plan that lasts about 3–5 years based on your income. Some debts may be reduced or discharged after you complete the plan.

Here’s the key practical point: if the means test doesn’t favor Chapter 7, a Chapter 13 plan may still offer real relief—like pausing collections and giving you a timetable to address arrears. For specifics, talk with a licensed attorney.

- Chapter 7 can discharge eligible unsecured debts

- Chapter 13 uses a repayment plan over time

- Means test affects many Chapter 7 cases

What debts usually survive bankruptcy

It’s important to understand the limits up front. Bankruptcy can help with many debts, but it does not automatically erase everything.

Some debts often survive bankruptcy, including (but not limited to) most student loans, many recent income tax obligations, child support and alimony, most criminal fines, and debts connected to fraud or certain misconduct. Courts look closely at the facts and how each debt is categorized.

Your attorney can tell you what’s likely in your situation. Since rules and outcomes vary by state and district, avoid relying on generic internet answers for your specific list of debts.

- Most student loans often remain

- Recent income taxes may remain

- Child support/alimony usually remain

- Fraud-related debts may not be dischargeable

How the means test is generally calculated (plain-language overview)

While the exact steps and forms are technical, the basic idea is straightforward: the court looks at your current monthly income using required categories and then compares it to federal benchmarks. It also allows certain expense amounts the rules consider standard.

If your income after allowed expenses is low enough, you may qualify for Chapter 7. If not, Chapter 13 may be the more likely path, or you may have to provide additional documentation or explanations allowed by law.

Because bankruptcy law and expense rules can change and because courts follow local practice, it’s smart to confirm your situation with a licensed bankruptcy attorney near you—not with guesswork.

- Your income is measured using federal rules and required categories

- Allowed expenses reduce what the means test counts

- The result influences Chapter 7 vs. Chapter 13

What you can do next (step-by-step, no pressure)

If you’re overwhelmed, the next step is getting accurate information for your state and court district. A licensed bankruptcy attorney can help you understand whether the means test applies, what numbers matter, and which chapter fits your goals.

CleanSlate Match is a FREE service that matches you with licensed bankruptcy attorneys in your area. We are not a law firm, and we do not file bankruptcy or represent you—matching only. You can request your preferred language as well.

Cost note: many consumer bankruptcy attorneys charge a flat fee for the attorney work, plus the required court filing fee and a small required credit-counseling fee. The exact range depends on the chapter (Chapter 7 vs. Chapter 13), case complexity, and the district. Flat-fee ranges are not quotes, and there are never guarantees about outcomes.

- Share your contact and general situation (no SSN, no bank details) and your preferred language

- Get connected with a licensed bankruptcy attorney near you

- In the consultation, confirm your bar license and ask how the means test may apply in your district

- Ask what the attorney’s process and total estimated costs typically look like for your chapter and complexity

- CleanSlate Match is free to you

- We only collect contact + general intent and do not ask for SSN or account details

- Confirm the attorney is licensed before you hire

The means test is a federal income-and-expense check that helps determine whether you likely qualify for Chapter 7 or should consider Chapter 13, and a licensed attorney can explain how it applies in your state and court.

Common questions

Does the means test mean the court thinks I’m lying or doing something wrong?

No. The means test is a required federal screening tool in many Chapter 7 cases. It’s designed to apply income rules consistently, not to judge your character or honesty.

If I don’t pass the means test, am I forced into Chapter 13?

Often, a higher result means Chapter 7 may not be available, and Chapter 13 becomes the more likely option. However, your full situation matters, and there may be ways your attorney can review special circumstances and alternatives under the law.

Can bankruptcy stop a wage garnishment or foreclosure while my case is pending?

In many cases, once a bankruptcy case is filed, an automatic stay goes into effect and pauses many collections, including some wage garnishments, foreclosures, and lawsuits. Exact results depend on the type of case and timing—your attorney can confirm what applies to you.

Does the means test use my actual bank account balances or my full financial statements?

The means test is based on income and expenses under specific rules, and the process requires certain documentation. Still, CleanSlate Match does not collect SSNs or bank-account details—your attorney would review what’s needed for your filing.

Will the means test tell me exactly which debts will be wiped out?

No. The means test is mainly about eligibility for a chapter (especially Chapter 7). Whether specific debts are dischargeable depends on debt type and legal categories, which an attorney can explain for your case.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →