Guides

What is the difference between secured and unsecured debt?

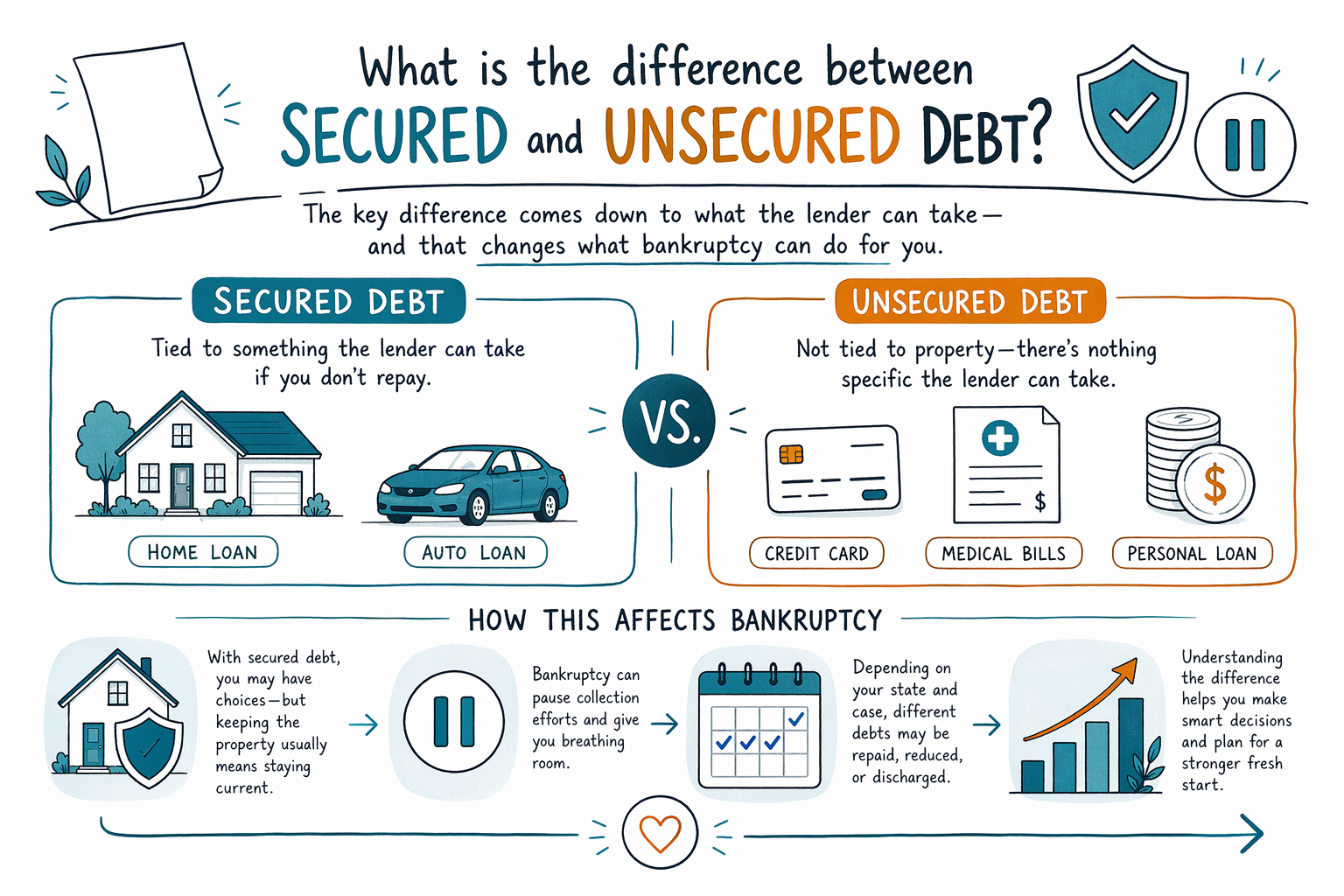

Secured debt is backed by something the lender can take if you don’t pay (like a car or home). Unsecured debt isn’t tied to specific property, so it’s handled differently in bankruptcy and other debt options.

The key difference (simple version)

Secured debt is connected to collateral—an asset that the lender can pursue if payments stop. Common examples are a mortgage (home) or a car loan (vehicle).

Unsecured debt is not tied to a specific asset. It usually comes from credit cards, many personal loans, and many medical bills.

This matters because bankruptcy laws treat secured and unsecured debts differently, including what you may be able to keep and how payment plans are structured.

Secured debt: how it works and what collateral means

When a debt is secured, the lender has a legal interest in the collateral. If you fall behind, the lender may use that interest to seek foreclosure (for a home) or repossession (for a car), depending on the situation.

In bankruptcy, secured creditors often still have rights to the collateral. Whether you can keep your home or car can depend on things like your ability to pay, the value of the collateral, and your state’s exemption rules.

Bankruptcy outcomes vary by state and federal district, so the details can be different depending on where you live.

Unsecured debt: what creditors generally can (and can’t) do

With unsecured debt, there’s no specific asset the lender can take just because you missed payments. Because of that, the lender’s options are often collections (calls, letters, lawsuits) and reporting to credit bureaus.

In bankruptcy, unsecured debts are usually grouped and handled under the chapter rules. In many cases, unsecured creditors may receive partial payment through a repayment plan or may receive a discharge for certain debts—depending on the type of unsecured debt and your case.

Important limit: bankruptcy does not automatically erase every kind of debt. Some debts often survive bankruptcy, even though results depend on the individual facts and local rules.

How secured vs. unsecured debt affects bankruptcy (Chapter 7 vs. Chapter 13)

In Chapter 7, many unsecured debts may be discharged, and certain debts tied to collateral are treated based on whether you keep paying and/or whether the collateral is surrendered. Some secured debts may still need ongoing payments if you want to keep the property.

In Chapter 13, you typically make payments for a set period through a court-approved plan. Secured debts are usually addressed in the plan (often with ongoing payments and/or treatment of arrears). Unsecured debts are also included, but how much they receive can depend on your repayment ability and the plan terms.

If you’re considering bankruptcy, the “secured vs. unsecured” breakdown is a key first step—but it’s not the only one. Courts also look at eligibility rules (including the “means test” for Chapter 7), exemptions, and timing.

What debts often survive bankruptcy (and why you should plan honestly)

Bankruptcy can help people get a fresh start, but it can’t promise to erase everything. Some debts usually survive, such as:

- Most student loans

- Recent income taxes (often depending on timing and other factors)

- Child support and alimony

- Many court fines and penalties

- Debts from fraud or certain misconduct

Also, even for unsecured debts, whether a specific bill gets discharged depends on facts. Your licensed bankruptcy attorney can review your situation and explain what is likely to be dischargeable and what may not be.

Next practical step: identify your debts correctly (without sharing sensitive info)

A fast way to prepare for a consultation is to categorize each debt as likely “secured” or “unsecured.” Look for clues like whether the debt is tied to a home or car.

If you’re not sure, don’t guess. Ask the attorney to confirm what type each debt is and how it appears in your case (for example, whether there’s collateral, a lien, or an arrears amount).

CleanSlate Match is a free service that can connect you with a licensed bankruptcy attorney near you. You’ll share contact details and a general sense of your situation and preferred language—never an SSN or bank details.

- Make a quick get-matched request

- Wait for a licensed attorney to reach out for a consult

- Ask the attorney how your secured vs. unsecured debts would be treated in your specific chapter

Secured debt is tied to something the lender can take (like a home or car), while unsecured debt isn’t—this difference strongly affects what bankruptcy can do for you, depending on your state and case details.

Common questions

How can I tell if my credit card or medical bill is secured or unsecured?

Most credit cards and most medical bills are unsecured because they’re not tied to specific collateral. If you have paperwork showing a lien on property (for example, against a car or home), that can make a debt secured—but many people only realize this by reviewing their account or getting attorney confirmation.

If I file bankruptcy, will a secured debt automatically go away?

Usually not automatically. Secured creditors often remain connected to the collateral. Whether you can keep the property, how arrears are handled, and whether the balance is discharged can depend on the chapter, your plan, and local rules—so it’s important to review your exact debts with a licensed bankruptcy attorney.

Do Chapter 7 and Chapter 13 treat secured and unsecured debts the same way?

No. Chapter 7 and Chapter 13 handle secured and unsecured debts differently. Chapter 13 typically uses a repayment plan that addresses both types, while Chapter 7 often focuses on discharge of qualifying unsecured debts and specific treatment of secured debts.

Are the rules the same everywhere in the United States?

Not always. Bankruptcy law is federal, but exemptions and certain procedures vary by state and by judicial district. A local, licensed bankruptcy attorney can explain what applies in your area.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →