Guides

What is a no asset case?

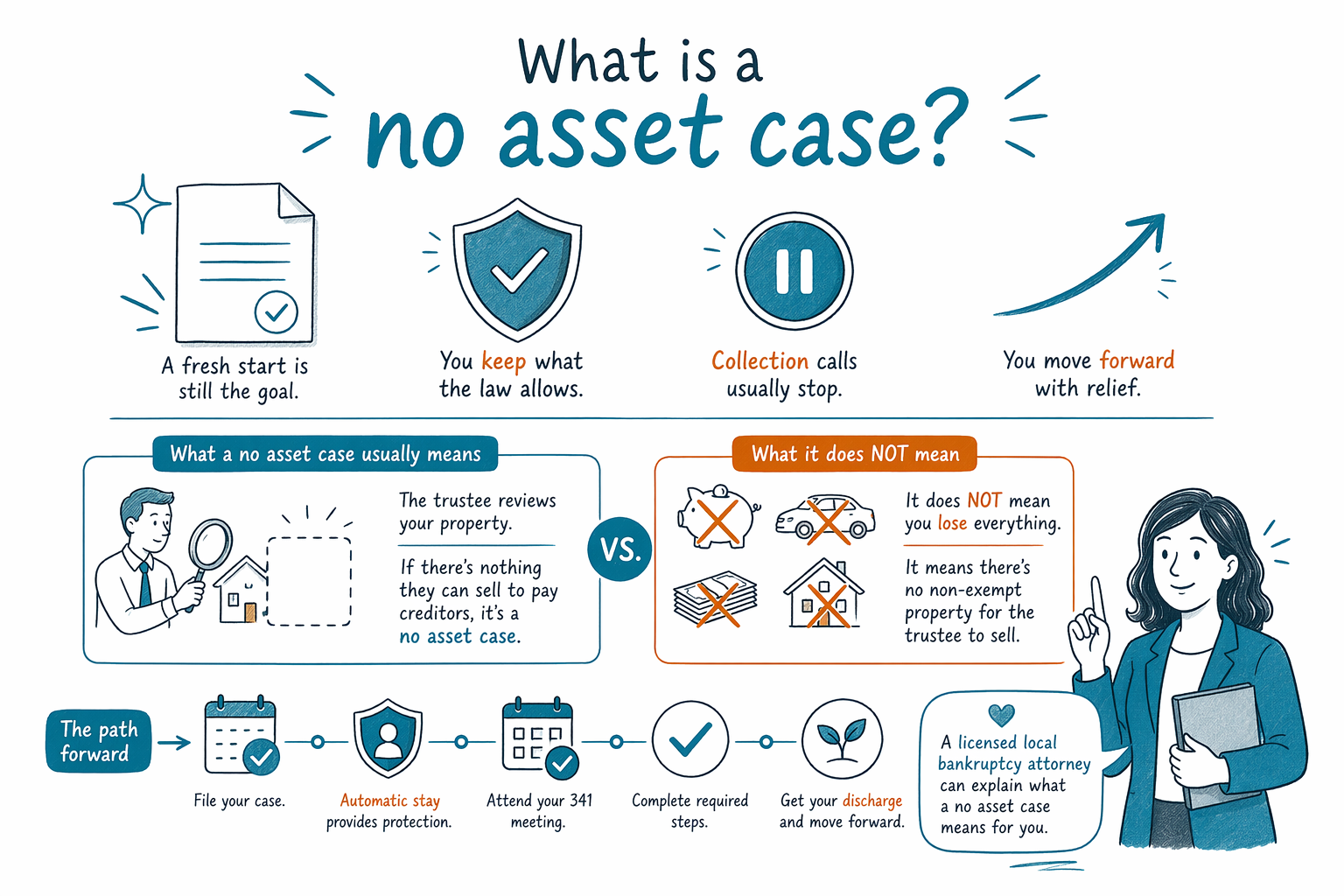

A no asset case usually means the bankruptcy trustee did not find property they could sell to pay unsecured creditors. It does not mean you own nothing, and it does not guarantee which debts will be erased.

What “no asset” means in plain English

In most consumer bankruptcy cases, especially Chapter 7, the court looks at whether there is any property the trustee could legally sell for the benefit of creditors. A “no asset case” usually means the trustee decided there were no non-exempt assets worth taking and selling.

That often happens because the things a person owns are protected by exemption laws, or because the items are not worth enough to sell after costs. Many people in Chapter 7 own a car, clothes, furniture, tools for work, or money in a bank account and still have a no asset case.

So the phrase can sound harsher than it really is. It does not automatically mean you are broke beyond hope, and it does not mean you lose everything. It is mainly an administrative term about whether there is anything available to distribute to creditors.

Bankruptcy rules, exemptions, and local practice vary by state and judicial district. A licensed bankruptcy attorney in your area can tell you whether your case may be treated as a no asset case under your state’s rules.

What happens in a no asset Chapter 7 case

If a Chapter 7 case is no asset, unsecured creditors usually are told not to file a proof of claim unless the court later says assets were found. In many cases, the case moves forward without any money being paid to general unsecured creditors.

That does not mean every debt disappears. Whether a debt is discharged depends on the type of debt, the facts of the case, and whether anyone objects. Bankruptcy can help many people, but it has limits.

Debts that often survive bankruptcy include most student loans, recent income taxes, child support, alimony, most court fines, and debts tied to fraud or similar misconduct. Outcomes depend on the individual case.

If you are trying to understand the bigger picture, you can read more on bankruptcy chapters and other plain-language guides.

Why many people still keep their property

The reason many Chapter 7 cases are no asset is that exemption laws protect certain property up to certain limits. Exemptions may cover some or all of the equity in your home, car, household goods, retirement accounts, public benefits, and other basic property.

The exact protection depends heavily on where you live. Some states require you to use that state’s exemptions. In other places, federal exemptions may be available. The dollar amounts and categories can be very different from one state to another.

Even when something is technically non-exempt, a trustee may still decide it is not practical to sell. If the item has little resale value, is hard to sell, or the sale costs would eat up any return, there may be nothing meaningful for creditors.

This is one reason it is so important not to guess based on something you read online. A licensed bankruptcy attorney can look at your state’s exemption rules and your specific property before you file.

What a no asset case does not mean

A no asset case does not mean bankruptcy is automatic, simple, or risk-free. You still have to qualify for the chapter you file, complete required paperwork, disclose your property honestly, and follow court rules.

It also does not mean you can hide property. You must list what you own and what you owe truthfully. If property is not disclosed, or if a transfer looks improper, that can create serious problems.

And it does not mean bankruptcy stops every financial problem forever. Filing a case usually creates an automatic stay that pauses most collections, wage garnishments, lawsuits, and foreclosures as soon as the case is filed. But some actions and some debts are treated differently, and timing matters.

If you are behind on a mortgage or car loan, Chapter 7 may or may not give you enough time or protection to keep that property long-term. In some situations, Chapter 13 may be the chapter that helps a person catch up over time instead.

How much does it usually cost to file?

Many consumer bankruptcy attorneys charge a flat fee for a typical case, plus the court filing fee and a small required credit-counseling fee. The real cost depends on the chapter, how complex the case is, whether you own a home or business interests, whether there are lawsuits or recent transfers, and the district where you file.

For many straightforward Chapter 7 cases, attorney flat fees often fall somewhere around $1,000 to $2,500, plus the court filing fee, which is commonly a few hundred dollars, and a small credit-counseling fee. For Chapter 13, attorney flat fees are often higher, sometimes roughly $3,000 to $6,000 or more depending on the district and the case, plus the court filing fee and course fees.

These are general ranges, not quotes or promises. A local attorney can tell you what they charge for your type of case and what is included.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We do not file bankruptcy cases. We help connect people with a licensed bankruptcy attorney near them for a consultation. It is free for you to get matched.

What to do if you think your case might be no asset

If you think you may need bankruptcy, the next step is usually to speak with a licensed bankruptcy attorney in your state. Ask whether they think your case may be a no asset Chapter 7, what property is protected by exemptions, what debts may survive, and whether Chapter 7 or Chapter 13 makes more sense.

You can also ask practical questions about timing, the automatic stay, whether a wage garnishment might stop, and what documents they would want to review before giving a clearer opinion. It is reasonable to ask them to explain things in simple language and to confirm their state bar license.

When you ask CleanSlate Match for help, we only need basic contact information and your general situation, such as your name, phone, optional email, state, preferred language, and a short description of what is going on. We do not ask for a Social Security number, bank-account numbers, credit-card numbers, or detailed account balances.

If you want, you can get matched for free with a licensed bankruptcy attorney near you.

A no asset case usually means the trustee does not see property worth selling, not that you lose everything, and a licensed local bankruptcy attorney can tell you what that means for you.

Common questions

Does a no asset case mean I own nothing?

No. It usually means the trustee did not find non-exempt property worth selling for creditors. Many people in no asset cases still own normal household items, a car, or even a home, depending on exemption laws.

If my case is no asset, will all my debts be erased?

No. A no asset case does not guarantee a full discharge. Some debts usually survive, including most student loans, recent income taxes, child support, alimony, most court fines, and some debts involving fraud.

Is a no asset case only for Chapter 7?

The term is most commonly used in Chapter 7. Chapter 13 works differently because it usually involves a repayment plan over time rather than a trustee selling non-exempt assets.

Can I keep my car or home in a no asset case?

Sometimes, yes. Many people keep important property through exemptions, and some use Chapter 13 to catch up on missed payments. Whether you can keep a home or car depends on your state’s exemption rules, the loan status, and the facts of your case.

How do I know if an attorney is properly licensed?

You can ask for the attorney’s full name and check their license with the state bar where they practice. It is a smart step before hiring anyone.

What does CleanSlate Match do?

CleanSlate Match is a free matching service. We are not a law firm, not a lawyer, and we do not give legal advice or file bankruptcy cases; we help connect you with a licensed bankruptcy attorney near you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →