Guides

What is a bankruptcy discharge?

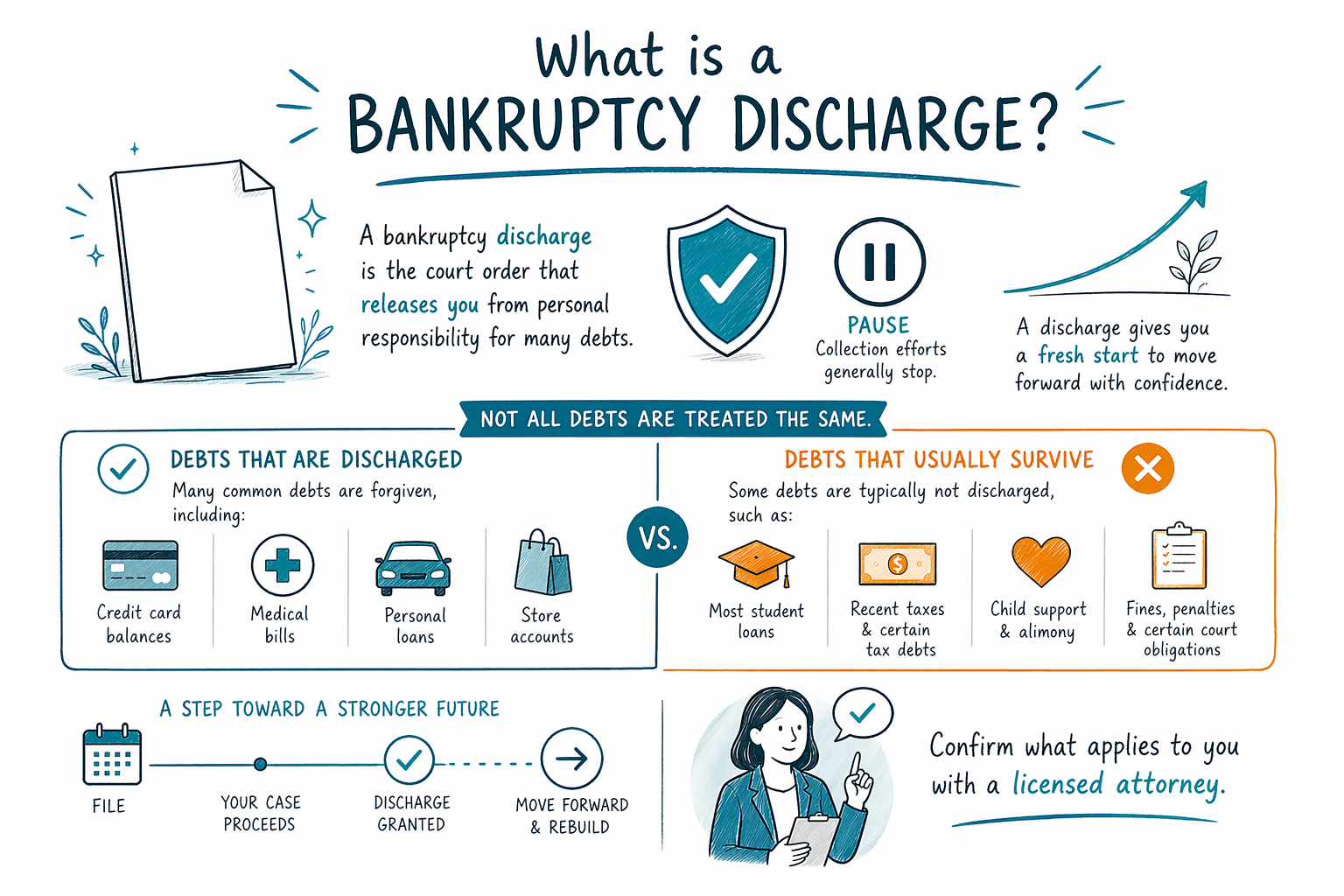

A bankruptcy discharge is the court order that releases you from personal legal responsibility for many debts. It can feel like a “fresh start,” but not everything is dischargeable—so the details depend on your case.

The direct answer: what a discharge means

A bankruptcy discharge is a court decision that says many of your debts must stop being collected from you personally. After the discharge is entered, creditors generally cannot legally pursue you for those discharged debts (though they may still have rights against certain property in some situations).

What you’re hoping for is protection from ongoing collection—calls, letters, and lawsuits—because the discharge is the legal end of the line for most personal debts in that chapter.

A key point: you don’t “automatically” get a discharge just by filing. You must follow the rules in your case, complete required steps, and qualify for discharge under the specific chapter and your facts.

Chapter 7 vs. Chapter 13: when a discharge can happen

In most Chapter 7 cases, if you qualify, a discharge is usually entered after the required process is completed (for many people, this is relatively faster than Chapter 13). In Chapter 13, you generally make payments through a court-approved plan first, and the discharge—if you complete the plan and meet requirements—comes later.

The “means test” and other eligibility rules can affect whether you can file Chapter 7, but discharge timing and eligibility are also influenced by what happens in your case.

If you’re trying to decide between chapters, it helps to understand that a discharge is tied to the chapter process—not just a form you file. Learn the basics at chapters.

What bankruptcy discharge usually does (and what it doesn’t)

Many common consumer debts may be dischargeable, such as credit card balances, many medical bills, personal loans, and many past-due amounts from unsecured accounts. The exact list depends on your state, your district, the chapter you file under, and the details of each debt.

However, some debts usually survive bankruptcy discharge, including:

- Most student loans (often not discharged unless a special legal standard is met)

- Certain recent income taxes

- Child support and alimony

- Most criminal fines and some court-ordered penalties

- Debts from fraud, certain misconduct, or willful wrongdoing (these can be treated differently)

Also, even when a debt is discharged, secured creditors (like mortgage or car lenders) may still have rights related to the collateral—your attorney can explain how that works for your situation.

The rules vary—why your district and state matter

Bankruptcy is federal law, but the practical rules and details can vary by state and by the specific federal district where your case is filed. Exemptions, local procedures, and how certain issues are handled can differ.

Because of that, the same type of debt may have a different outcome in different places, and discharge questions can depend on facts like how the debt was incurred and whether it involves fraud or other special categories.

A licensed bankruptcy attorney in your area can confirm what discharge likely covers for you after reviewing your documents—no guessing.

How a discharge connects to stopping collections (automatic stay vs. discharge)

It’s easy to mix these up. The automatic stay and the discharge are related, but they are not the same thing.

- The automatic stay begins when you file (with limited exceptions). It can pause many collections immediately, including lawsuits, wage garnishment, and foreclosure actions.

- The discharge is what comes later (after the case process), and it’s what releases you from personal liability for many debts.

So even if discharge is the “fresh start,” the automatic stay often provides immediate breathing room. If you’re dealing with a lawsuit or wage garnishment, that first pause can be very important.

If you’re overwhelmed, you don’t have to handle this alone—see get-matched to connect with a licensed bankruptcy attorney near you.

What to ask in a first consultation about discharge

When you meet with a bankruptcy attorney, you can ask practical, discharge-focused questions to understand what “fresh start” could realistically mean in your case. Guides can also help you get ready.

Bring your questions, and expect an honest answer about limits, timing, and what depends on the facts. Helpful questions include:

- Which of my debts are likely to be discharged, and which likely won’t?

- Does my situation look more like Chapter 7 or Chapter 13 for discharge purposes?

- Will I get the benefit of the automatic stay quickly, and are there exceptions in my case?

- Are any of my debts potentially non-dischargeable because of how they were incurred?

- What steps do I need to complete to get a discharge?

Be wary of anyone who promises a guaranteed wipeout of all debt. Outcomes depend on eligibility, compliance, and the category of each debt—your attorney should explain that clearly.

A bankruptcy discharge is the court order that releases you from personal responsibility for many debts, but some debts usually survive—so confirm what applies to you with a licensed attorney.

Common questions

Will a bankruptcy discharge get rid of all my debt?

Usually it can discharge many types of debts, but not all of them. Common debts that often survive include student loans, certain recent income taxes, child support/alimony, many fines, and debts related to fraud or certain misconduct. Your specific discharge depends on your facts, the chapter, and your state/district.

Do I get the discharge the day I file?

Not typically. Filing can trigger an automatic stay that pauses many collection actions right away, but discharge usually happens later—after required steps are completed and eligibility requirements are met in your case.

What happens to collection calls and lawsuits after discharge?

For debts that are discharged, creditors generally should stop trying to collect them from you personally after the discharge is entered. If you had an active lawsuit, the discharge can affect what the creditor can do going forward. The automatic stay and discharge work together, but they apply at different times.

Is the discharge the same in every state?

Bankruptcy is federal, but rules and practical outcomes can vary by state and the federal district where your case is filed—especially around exemptions and local procedures. A licensed attorney near you can explain how discharge works for your location.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →