Guides

The Bankruptcy Process, Step by Step

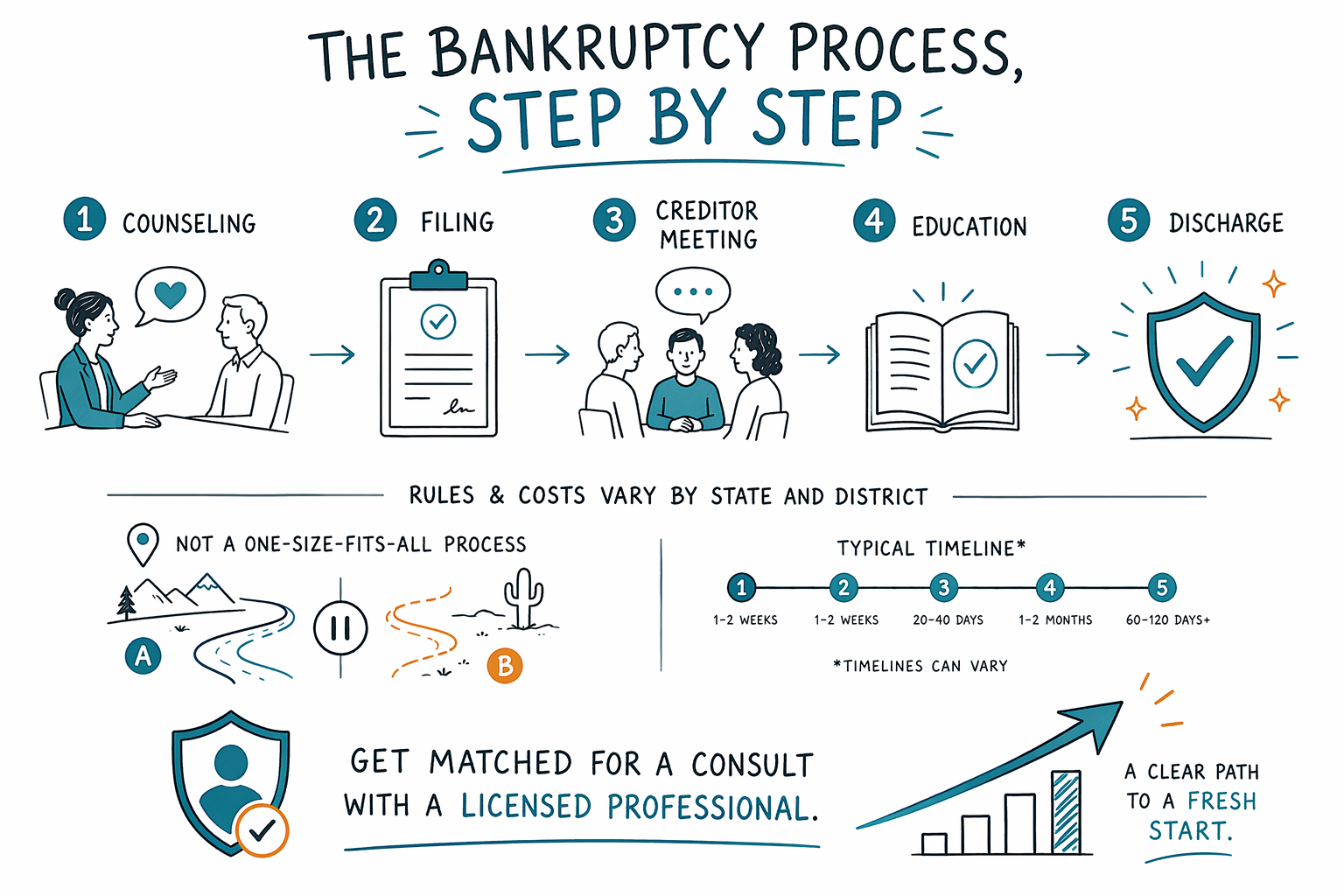

Bankruptcy can feel scary, but the process has clear steps. Below is a plain, real-world timeline of what usually happens from credit counseling to discharge—so you know what to expect.

1) First: choose the chapter (Chapter 7 vs Chapter 13)

The bankruptcy process starts with deciding which chapter fits your situation. Two common consumer options are Chapter 7 and Chapter 13, and the differences matter.

In general terms: Chapter 7 is often used to discharge (wipe out) many eligible debts, and most cases aim for a quicker end. Chapter 13 usually involves a court-approved payment plan over time.

A licensed bankruptcy attorney in your area can explain which chapter is more likely to work for you based on your income, debts, and goals (like keeping your home or car). Rules vary by state and judicial district, so your local process may differ.

- If you’re behind on a mortgage or car, ask about staying in the home/car under exemptions or a repayment plan.

- If you have wages being garnished or a foreclosure pending, timing and local procedures can be very important.

2) Credit counseling (required before you file)

Before you can file, federal law generally requires a credit counseling session from an approved provider. You’ll typically receive a certificate or completion document.

This is one of the earliest steps, and it can feel like paperwork at a stressful time—but it’s a standard part of the process. It also helps you confirm what debts you have and what options exist.

After that, you can move forward to filing, with the guidance of a licensed attorney who knows your local rules.

- The counseling requirement is separate from bankruptcy itself.

- If language is a barrier, ask the approved provider about available language support.

3) Filing the case: your petition and schedules

Next comes the court filing. Your attorney will prepare and submit your bankruptcy petition and the required schedules and statements (like your debts, income sources, assets, and recent financial history).

The information you provide needs to be accurate and complete. Because the details affect eligibility and outcomes, it’s especially important to review every form carefully.

Once filed, an important legal protection usually begins: the automatic stay. It can pause many collection actions such as most lawsuits, collection calls, foreclosure activity, and wage garnishment while the case is pending—though there are exceptions that an attorney can explain for your situation.

- You don’t need to share sensitive financial-account details to get matched—use only contact details plus a general description of your situation.

- Local court rules may affect how quickly hearings are scheduled.

4) The meeting of creditors (often called the “341 meeting”)

After filing, you’ll typically attend a meeting of creditors. Despite the name, it’s usually not like a courtroom trial.

You’ll answer questions about your forms under oath. A trustee appointed for your case may ask questions, and creditors may attend, though they often don’t.

This step is a key moment to be honest and consistent with what you filed. Your attorney will usually help you prepare so you understand what to expect. If you need interpretation or accommodations, tell your attorney early.

- Bring identification and any documents your attorney asks for.

- You can usually stop many collection actions simply by filing, but the court process still continues.

5) Completing required course(s) and dealing with the court process

Most consumer bankruptcy cases also require debtor education (a second course) before discharge. The exact timing and steps can vary depending on the chapter and your district.

During the case, the trustee may review your documents and may ask for additional information. In Chapter 13, the plan process includes proposed payments and confirmation by the court.

If you’re trying to keep property—like a home or car—your chapter, exemptions, and the details of your payments and arrears will matter. A licensed attorney can explain what’s commonly possible in your area, and what is not.

- Exemptions (what you may keep) vary by state and sometimes by district.

- Some debts are treated differently than others depending on the chapter and facts.

6) Discharge (the “end goal”)—and what usually survives

For many people, the goal of bankruptcy is a discharge, which can relieve you from certain debts that are eligible under the law. The date depends on the chapter, your completion of requirements, and court schedules.

However, bankruptcy does not necessarily erase every type of debt. Some debts commonly survive bankruptcy, such as most student loans (usually), certain recent income taxes, child support and alimony, many court fines, and debts involving fraud or other misconduct. What survives and what doesn’t depends on your specific facts and the chapter you file.

Because rules vary by state and judicial district—and bankruptcy law changes—ask a licensed bankruptcy attorney to review your situation and explain, realistically, which debts are most likely to be discharged in your case.

- A discharge can still be a powerful fresh start even if not every debt goes away.

- Do not rely on online guesses—confirm with a lawyer for your district.

Cost and timing: what people typically pay (ranges) and why they differ

Most consumer bankruptcy attorneys charge a flat fee, plus the required court filing fee and a small credit-counseling/education fee. Exact pricing depends on the chapter (7 or 13), the complexity of your case, and your district.

As general ranges people often see: court filing fees are commonly a few hundred to over $300 for Chapter 7, and higher for Chapter 13, with additional required administrative amounts. Attorney flat fees also vary widely by case complexity (for example, how many creditors, whether there’s a foreclosure or wage garnishment, and whether plan work is needed in Chapter 13). Your attorney can tell you the specific flat fee for your case—ranges are not quotes.

If cost feels impossible, it’s still worth getting matched. Some attorneys offer structured payment options, and in the same first consultation you can discuss what’s required to start and whether your local rules offer any relief. Cost and timing are not guaranteed outcomes.

- Flat fee + court fees + required counseling/education fees are the common structure.

- Anything involving more filings, plan confirmation work (Chapter 13), or complex assets usually costs more.

7) After you file: keep your paperwork straight and follow instructions

After filing, the most helpful thing you can do is stay organized and follow your attorney’s instructions. Bankruptcy is paperwork-heavy, but you don’t have to do it alone.

You may need to provide documents for the trustee or complete courses by specific deadlines. In Chapter 13, you’ll also make plan payments consistently for the plan to succeed.

If you speak a language other than English, or you’re not fully comfortable with legal paperwork, ask about interpretation and written materials in your preferred language. You deserve clear communication.

- Missing deadlines can affect whether you get a discharge.

- Your attorney can explain how to handle new collection contacts after the automatic stay begins.

Bankruptcy usually follows a clear sequence—counseling, filing, the creditor meeting, education, then discharge—but rules and costs vary by state and district, so get matched for a consult with a licensed attorney to confirm what will happen in your case.

Common questions

Will bankruptcy stop my wage garnishment or foreclosure right away?

In many cases, once you file, the automatic stay can pause many collection actions, including wage garnishment and foreclosure activity, while the case is pending. But there are exceptions and special rules, so it’s important to confirm what applies to your situation with a licensed bankruptcy attorney in your district.

What’s the difference between Chapter 7 and Chapter 13, in plain terms?

Chapter 7 typically aims for quicker discharge of eligible debts, often based on liquidation of non-exempt assets (if any). Chapter 13 usually uses a court-approved repayment plan over time and may help people catch up on certain debts. The right choice depends on your income, debts, and goals.

Does bankruptcy erase everything I owe?

Not always. Some debts often survive bankruptcy, including most student loans, many child support/alimony obligations, certain recent income taxes, many court fines, and debts tied to fraud or certain misconduct. Your discharge depends on your facts and the chapter, so a lawyer review is essential.

How much does it cost to file?

Many attorneys charge a flat fee plus the court filing fee and required course fees. The total can vary based on the chapter and complexity, and ranges aren’t guaranteed prices. A consultation with a licensed bankruptcy attorney can give a more accurate flat-fee number for your case.

Is CleanSlate Match a law firm? Can it file my bankruptcy?

No. CleanSlate Match is a FREE matching service that helps you connect with a licensed bankruptcy attorney near you. We do not file bankruptcy and we do not create an attorney-client relationship.

Do I need to share my Social Security number or bank account information to get matched?

No. CleanSlate Match collects contact details and general intent (and a general description of your situation and preferred language). Don’t share sensitive financial-account information through the matching form—your attorney will explain what’s needed during a legal consultation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →