Guides

Rebuilding Credit After Bankruptcy

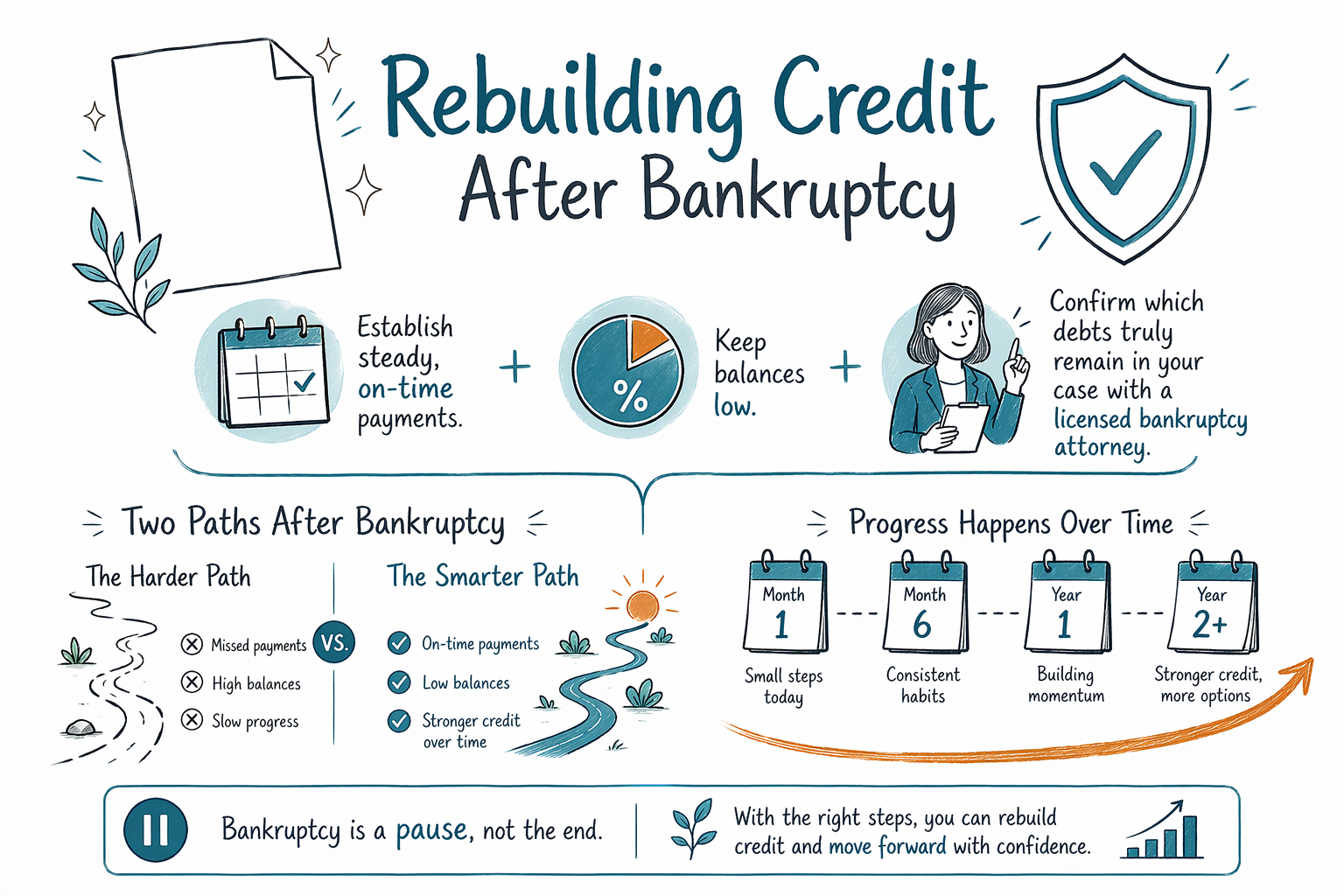

Yes, you can rebuild credit after bankruptcy. This guide explains what changes, what to do next, and what to expect in the months and years after a discharge—without promises or pressure.

First, the honest answer: Can bankruptcy hurt or help your credit?

Bankruptcy usually hurts your credit score at first because it becomes part of your credit report. But it can also be a turning point: once you get a discharge, many people stop falling further behind and can build new payment history.

A key point: credit rebuilding is a process. There’s no instant “fix,” and outcomes vary by your starting credit profile, the credit reporting timelines, and the choices you make after filing.

Also, bankruptcy rules and credit-related details can differ depending on where you live. State and federal rules, plus court practice, vary by state and judicial district—so it’s smart to confirm your situation with a licensed bankruptcy attorney near you.

- Bankruptcy is often visible on your credit report for years

- Your post-bankruptcy behavior (on-time payments, low balances) matters a lot

What happens to credit after a Chapter 7 or Chapter 13 discharge?

Both Chapter 7 and Chapter 13 can lead to a discharge, but the timeline and the path can feel different. In general, a Chapter 7 discharge can happen sooner, while Chapter 13 involves a repayment plan for a period of time.

Credit bureaus may reflect the filing and the discharge at different times. If you’re in Chapter 13, you may need to keep making plan payments and follow any terms required by the court and your attorney.

Because details vary by case, the best way to know what your credit report should show (and when) is to discuss it with your bankruptcy attorney. You can also request your credit reports after the case begins and check for accuracy.

- Chapter 13 usually includes ongoing payments during the plan

- Your credit report updates as the case status changes

Step-by-step: Rebuild your credit in the first 30–90 days

Start with what you can control right away. After discharge, focus on stability first—paying bills you can pay, keeping accounts current, and reducing stress.

Then build a “clean” payment pattern using simple tools. If you have any debts that survived or were not discharged, you’ll want to treat those payments as part of your credit plan.

Try this approach:

1. Check your credit reports from each bureau and look for errors

2. Make sure your surviving obligations are identified and scheduled (with help from your attorney if needed)

3. Pay every current bill on time—utilities and phone plans can matter too

4. Keep utilization low on any revolving credit you still have (like cards that remain open)

If you’re unsure what counts as discharged vs. surviving in your case, confirm with a licensed bankruptcy attorney. That’s not something to guess.

- On-time payments are the foundation of rebuilding

- Accuracy matters—review your reports for mistakes

Credit building options after bankruptcy (what usually works, and what to be careful about)

Many people rebuild credit using secured credit cards, credit-builder loans, or a carefully chosen starter credit card. The goal isn’t to chase rewards—it’s to create consistent, on-time payment history and keep balances low.

Be careful with anything that sounds too good: high-pressure “credit repair” pitches, promises to remove accurate items, or offers that require paying for services that don’t clearly explain what they’ll do.

Also remember: not all debts are discharged. Some debts often survive bankruptcy, including most student loans, many recent income taxes, child support or alimony, most court fines, and debts involving certain wrongdoing (for example, fraud). Outcomes depend on your individual case.

Good credit rebuilding usually looks like this:

- Choose a low-risk credit option (like a secured card)

- Use small amounts and pay on time every month

- Avoid new debt you can’t comfortably repay

If you want help choosing a safe next step, a credit counselor can help with budgeting and plan basics. But for what bankruptcy did (or didn’t) discharge in your case, lean on your licensed attorney.

- Focus on on-time payments and low balances

- Avoid high-pressure “credit repair” promises

How long does it take to see improvement?

Many people see gradual improvement over months, especially once they establish new on-time payment history. Your score may still be affected by the bankruptcy filing, but steady positive activity can help your overall profile.

There’s no universal timeline. Your starting point matters: credit history length, whether you had late payments before, how many accounts are reporting, and what debts survived all play a role.

The most reliable signs of progress are practical ones:

1. Fewer late payments (and none missed) on accounts you’re responsible for

2. Your balances staying low compared to your available credit

3. Credit reports showing consistent current status

If you’re currently overwhelmed, you don’t have to “figure it out alone.” Get matched with a licensed bankruptcy attorney to confirm what applies to your case and discuss next steps—free to you.

- Improvement is usually gradual, not instant

- Consistency beats quick fixes

Before you start rebuilding: confirm what bankruptcy changed in your specific case

Your credit rebuilding plan should match your reality. Bankruptcy can change what you owe going forward, but not every type of debt is handled the same way, and not every case has the same results.

Rules vary by state and judicial district, and details can also depend on whether you filed Chapter 7 or Chapter 13, your exemptions, and the facts of your case. Because of that, it’s important not to rely on generic advice or assumptions.

A licensed bankruptcy attorney can help you understand:

1. Which debts were discharged (and which likely survived)

2. What you should continue paying

3. When and how the automatic stay and case outcome may affect collection activity

If you’d like to learn the basics first, explore our guides on Chapters of bankruptcy and all guides. Then, when you’re ready, use Get matched with a licensed bankruptcy attorney. CleanSlate Match is a FREE matching service—not a law firm, not your lawyer—and it doesn’t file bankruptcy.

- Don’t guess what survived—confirm with an attorney

- Rules and outcomes vary by state/district

You can rebuild credit after bankruptcy by establishing steady, on-time payments and keeping balances low—while confirming which debts truly remain in your case with a licensed bankruptcy attorney.

Common questions

Will I be able to get a credit card or loan again after bankruptcy?

Often, yes. Many people qualify for starter credit after bankruptcy through secured cards or credit-builder products, but approval and terms vary by lender and your specific credit history. Focus on on-time payments and keeping balances low.

Can bankruptcy remove late payments or collections from my credit report?

Bankruptcy itself can change how items appear, but it doesn’t always erase other accurate negative marks. Credit reporting rules differ by situation, and the best way to verify is to check your credit reports for accuracy and discuss your case details with a licensed bankruptcy attorney.

Are all my debts wiped out when my bankruptcy is discharged?

No. Many debts often survive bankruptcy, such as most student loans, certain recent income taxes, child support or alimony, most court fines, and debts related to wrongdoing (like fraud). Outcomes depend on your individual case.

How do I know which bills I still must pay after discharge?

Your discharge notice and your case documents, plus advice from a licensed bankruptcy attorney, are the reliable source. Because rules vary by state and judicial district, don’t rely on assumptions—confirm what applies to you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →