Guides

Joint Vs Individual Bankruptcy

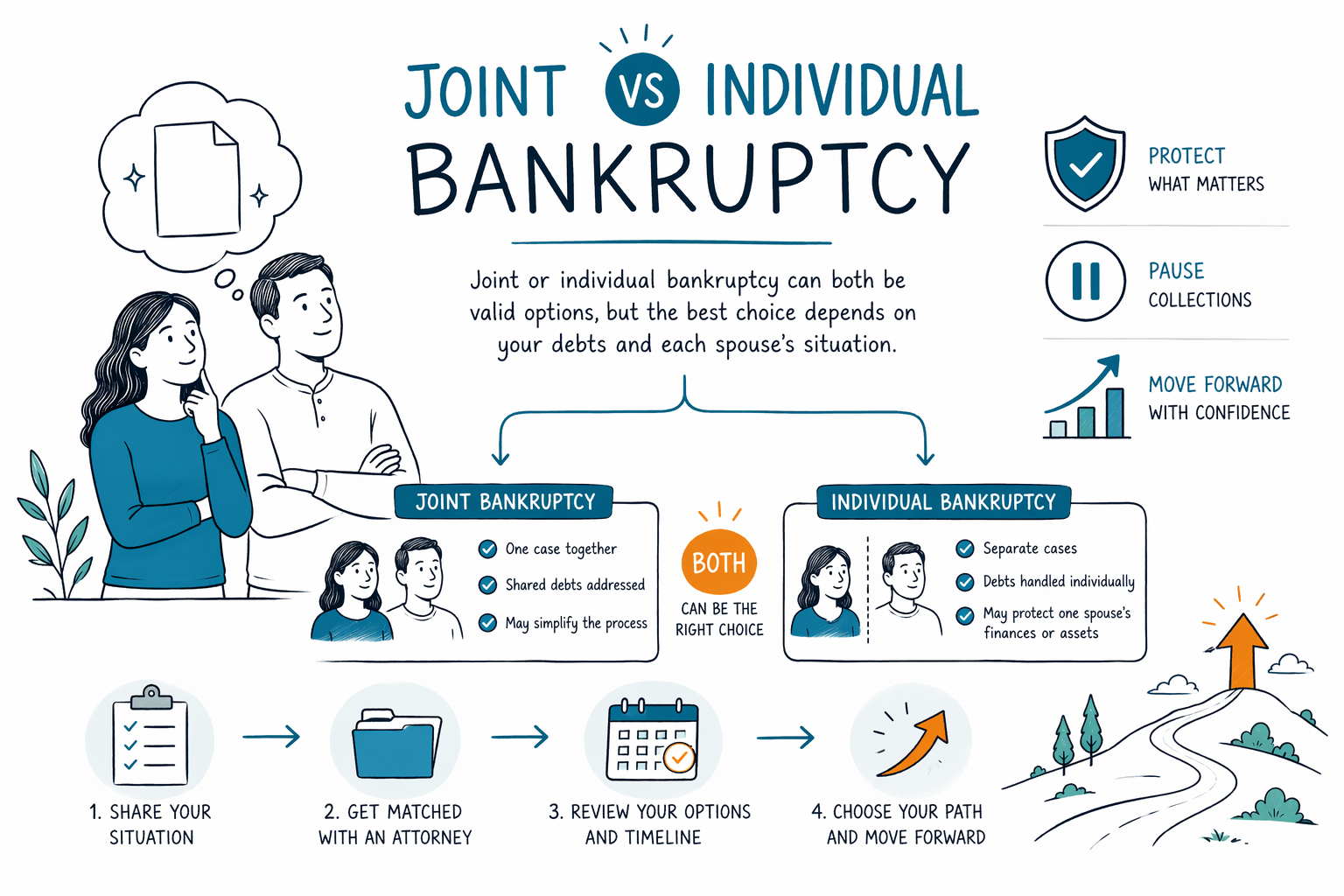

If you and your spouse are both in debt, you may be able to file together or separately. Here’s the plain-language difference, what usually matters most, and how to choose with a licensed bankruptcy attorney in your area.

Quick answer: Joint vs individual bankruptcy—what’s the difference?

In US consumer bankruptcy, a “joint” filing usually means both spouses file in the same case (most often Chapter 7 or Chapter 13). An “individual” filing means only one spouse files.

Whether you can file together depends on the chapter, your situation, and how your debts are connected (like shared credit cards or a shared mortgage). For many couples, deciding between joint and individual affects paperwork, strategy, and how each person’s income and debts are handled.

This guide is general education, not legal advice. Bankruptcy rules, exemptions, and procedure vary by state and federal court district, so the best answer for you should come from a licensed bankruptcy attorney after reviewing your specific facts.

- Joint filing = both spouses are included in the same bankruptcy case.

- Individual filing = only one spouse files; the other spouse is not included.

Why couples consider filing together

Many married couples file together when they share major debts (for example, joint credit cards, a shared car loan, or a mortgage both people are listed on). A joint case can simplify the process because the court looks at both spouses’ situations within one filing.

Filing together may also help if you want both credit histories and collections to be addressed through bankruptcy at the same time. In a Chapter 7 or Chapter 13 case, the automatic stay generally pauses many collection actions after the case is filed, but the details still depend on the facts and the chapter.

Still, a joint filing isn’t always the best choice. If one spouse has little or no debt, very different income, or assets that may be treated differently, an attorney may recommend an individual filing for a clearer outcome.

Why couples sometimes file separately (and what can change)

Some couples choose individual bankruptcy when only one spouse is mainly responsible for the debts. For example, if one spouse’s credit cards are in their name only, or the foreclosure/wage garnishment is tied primarily to that person, a separate filing may be more targeted.

It may also matter if one spouse has income that could affect Chapter 7 eligibility (the “means test” rules) or if your plan payments in Chapter 13 would be very different for each person. In Chapter 13, the plan is designed around your household’s situation and the debts included—so who is filing can change the plan.

Even if only one spouse files, bankruptcy can still create an automatic stay effect for certain collection actions, but it does not automatically erase every issue affecting the non-filing spouse. A bankruptcy attorney can explain what typically stops and what may continue in your specific situation.

- Separate filing can be useful when only one spouse’s debts or income are the main problem.

- Who files can affect Chapter 7 eligibility and/or Chapter 13 plan payments.

Chapter 7 vs Chapter 13: joint or individual choices depend on the chapter

Chapter 7 is often described as a liquidation chapter. Many people use Chapter 7 to discharge (wipe out) qualifying unsecured debts, while keeping certain property protected by exemptions. Chapter 7 may not be available for everyone because eligibility rules (including the means test) can apply.

Chapter 13 is a reorganization chapter with a court-approved repayment plan. It can be a strong option if you need time to catch up on certain debts (like a mortgage arrearage) or if Chapter 7 isn’t available. In Chapter 13, the plan length and payment amount are influenced by the filer(s) and the household’s financial picture.

Whether you file jointly or individually, a licensed attorney can explain how your state’s exemptions, the means test in your area, and the type of debts you have affect what’s possible. Rules and interpretations can vary by state and district.

Important limits: bankruptcy doesn’t erase all debts

It’s understandable to hope bankruptcy will remove everything. But in real life, some debts usually survive bankruptcy, even when the case is properly filed. Outcomes depend on the individual case, the chapter, and the type of debt.

Common debts that often do not get discharged include: most student loans (with limited exceptions), recent income taxes, child support and alimony, many court fines/penalties, and debts involving fraud or certain misconduct. If you’re facing allegations, a claim in court, or a garnishment tied to specific conduct, an attorney should review it carefully.

Also, even when debt is discharged, the timeline, property rules, and plan requirements (especially in Chapter 13) still apply. A good consultation will be honest about what can be discharged in your case and what usually remains.

What to do next: get matched with a licensed attorney (free) and confirm the facts

A calm, judgment-free first step is to talk with a licensed bankruptcy attorney near you. CleanSlate Match is a FREE matching service that connects you with participating attorneys for a consultation. We are not a law firm, we are not your lawyer, and we do not file bankruptcy.

To get matched, you’ll share contact information and a general intent (for example, your state and preferred language, plus a basic sense of what you’re dealing with). You do not need to provide sensitive financial details like Social Security numbers or bank-account information.

During your consultation, bring any notices you have (like foreclosure or garnishment papers) and ask direct questions such as whether joint or individual filing is better for your debts and your household. Also confirm the attorney’s bar license and ask about fees—most consumer bankruptcy attorneys charge a flat fee, plus required court filing fees and a small required credit-counseling fee. The total cost can vary depending on the chapter and the complexity of the case, and ranges are not guarantees.

Joint or individual bankruptcy can both be valid options, but the best choice depends on your debts and each spouse’s situation—get matched with a licensed bankruptcy attorney near you for a clear, honest answer at no cost to you.

Common questions

Can married couples file bankruptcy together if we have shared debt?

Yes—many couples can file together (jointly in one case). But whether it’s the better choice depends on the chapter, who has which debts, each spouse’s income and assets, and state/district rules. A licensed attorney can explain what typically works best for your specific debts.

If only one spouse files, will the other spouse’s debts be wiped out?

Usually, no. If the non-filing spouse is not in the bankruptcy case, their debts generally are not discharged in that case. However, some collection activity may be paused depending on the type of debt and how it’s enforced—your attorney can clarify for your situation.

Does bankruptcy automatically stop foreclosure or wage garnishment right away?

Often, when a bankruptcy case is filed, an automatic stay goes into effect and can pause many collection actions, including many foreclosure and garnishment efforts. The exact effect can vary based on your case facts and timing, so it’s important to discuss your documents with a licensed attorney.

What debts usually survive bankruptcy?

Some debts often survive, such as most student loans, recent income taxes, child support/alimony, many fines/penalties, and debts involving fraud or certain misconduct. Whether a specific debt can be discharged depends on the case, so don’t assume one outcome without legal review.

How much does it cost to file, and will I get an exact price?

Many consumer bankruptcy attorneys charge a flat fee, plus the court’s required filing fee and a small required credit-counseling fee. Total costs vary by chapter and complexity, and any numbers you hear are ranges, not guarantees. Your consultation should confirm what you can expect for your specific case.

Is CleanSlate Match a law firm?

No. CleanSlate Match is a FREE matching service. We do not file bankruptcy and we do not create an attorney-client relationship. Participating attorneys provide the legal advice after you consult with them.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →