Guides

How to prepare for bankruptcy?

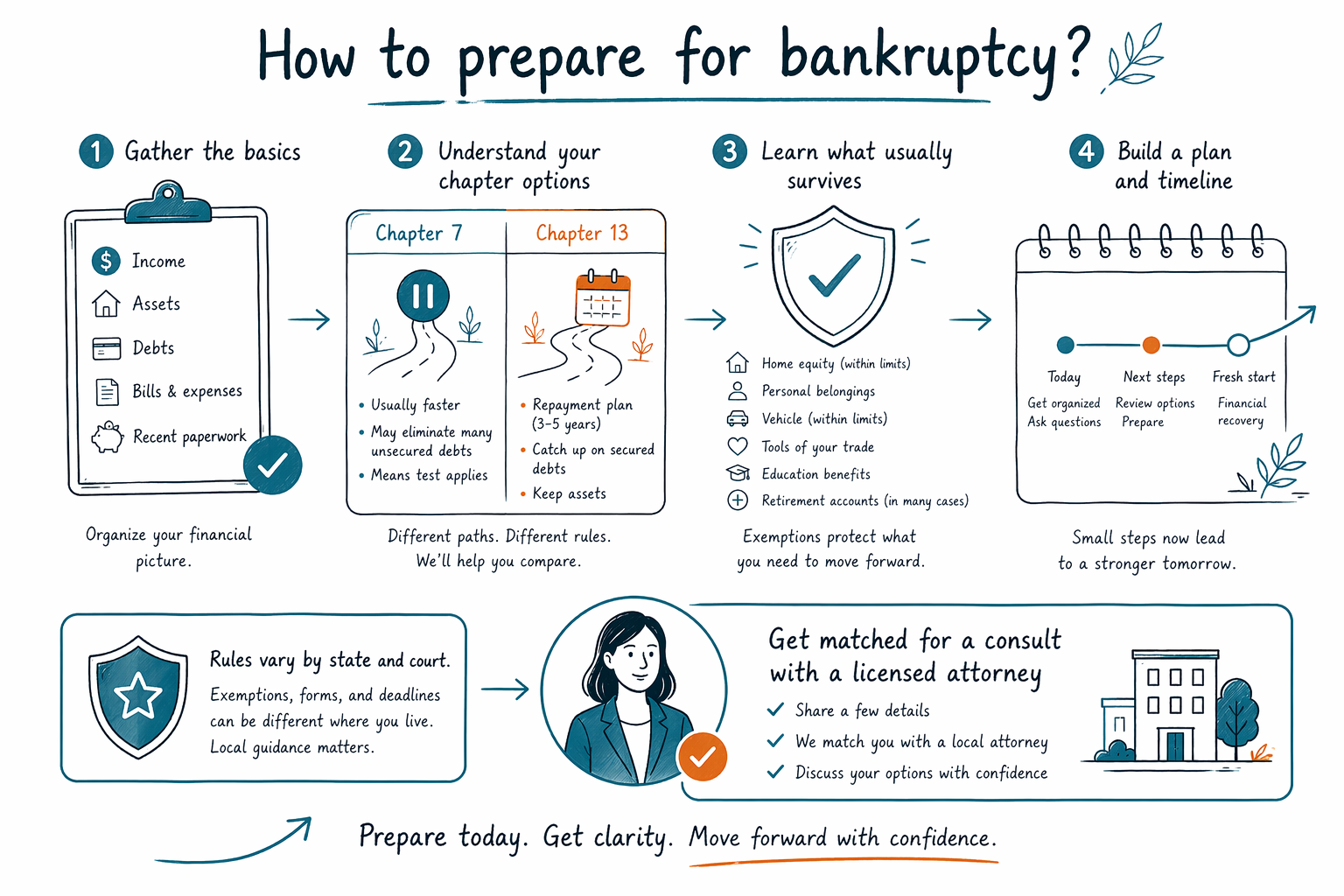

If you’re considering bankruptcy, the best preparation is simple: gather key documents, understand your options (usually Chapter 7 or Chapter 13), and talk with a licensed bankruptcy attorney. You’ll feel more grounded fast.

Step 1: Take a breath—and confirm you’re asking the right question

Many people don’t need to “fix everything” before they meet an attorney. They just need a clear, honest picture of what’s happening so the attorney can explain what bankruptcy could do in their specific situation.

Start by writing down (in your own words) what debts you have and what collection actions are happening now—like missed mortgage payments, wage garnishment, bills in collections, or a court case. This helps the first consultation stay focused.

CleanSlate Match is a FREE matching service that can connect you with a licensed bankruptcy attorney near you, but we are not a law firm and we don’t file bankruptcy for you. A lawyer will review your details and tell you the real options for your area.

Rules and eligibility requirements vary by state and by the federal court (judicial district), so it’s important not to rely on general advice alone.

Step 2: Understand Chapter 7 vs. Chapter 13 (so you can ask better questions)

A bankruptcy attorney will usually discuss two consumer options: Chapter 7 and Chapter 13.

- Chapter 7 (often called “liquidation”) may discharge many qualifying unsecured debts, but whether you qualify can depend on your income and the “means test,” and you may lose non-exempt assets.

- Chapter 13 (a “reorganization”) creates a repayment plan, often allowing you to catch up on certain debts (like past-due mortgage or car payments) over time while making ongoing plan payments.

Because rules vary by state and district—and because exemptions differ—your best choice depends on your debts, income situation, property, and what you’re trying to protect. Review chapters for a plain-language overview before you meet a lawyer.

Step 3: Gather your documents (you don’t need everything, but you do need the basics)

For the first meeting, attorneys commonly request documents that show your identity, debts, income, and any collection or court activity. You can start with what you have right now—even photos of papers or screenshots are often better than nothing.

A helpful starter checklist:

- A list of your debts (credit cards, medical bills, personal loans)

- Any notices you received about collections, judgments, or lawsuits

- Mortgage or landlord paperwork showing missed payments (if relevant)

- Car loan or lease paperwork (if relevant)

- Recent pay stubs and proof of income (if you have wages)

- Proof of benefits (if applicable)

- Any tax return-related documents you already have (especially if there are tax issues)

Do not include sensitive account numbers when you first reach out to a matching service. CleanSlate Match collects contact and general intent only (like your name, phone, state, and preferred language). You can share more details directly with your attorney during the legal consult, following their instructions.

Step 4: Learn what bankruptcy can and cannot erase (so there are no surprises)

Bankruptcy can offer a fresh start, but it does not erase every type of debt in every case. Your attorney will explain what is likely to be discharged and what may remain.

Common examples of debts that often survive bankruptcy include:

- Most student loans (generally) unless a specific, difficult hardship standard is met

- Recent income taxes in many situations

- Child support and alimony

- Many court fines and penalties

- Debts connected to fraud or certain willful misconduct

Also, some debts may not be discharged if they are secured by property and the plan or case doesn’t address them the right way. Exemptions, state law, and the facts of your case matter a lot.

If you’re worried that you’ll “lose everything,” that fear is understandable. Many people keep a home and/or car through exemptions or by using Chapter 13 to keep paying under a plan—but only a licensed attorney can tell you what applies to your situation and location.

Step 5: Prepare for the cost conversation (what people usually pay)

It’s normal to be anxious about attorney fees. Most consumer bankruptcy attorneys charge a flat fee, plus the required court filing fee and a small required credit-counseling fee.

Typical total ranges (not quotes) are often:

- Chapter 7: roughly $1,500–$3,500 for attorney + court costs (varies by district and case complexity)

- Chapter 13: roughly $3,000–$6,500+ for attorney + court costs (varies more widely because of plan length and complexity)

The amount can go up or down depending on things like: how many creditors you have, whether there are assets to protect, whether there’s a lawsuit or judgment, how complicated your income situation is, your state’s exemption issues, and how involved plan administration becomes.

CleanSlate Match is free for you. If you use our matching service, participating attorneys pay a flat fee to participate—there’s no percentage, contingency, or share of your debt or of attorney fees from you.

Step 6: Know what happens when you file (the “automatic stay”)—and act calmly

One reason people pursue bankruptcy is the automatic stay. When a bankruptcy case is filed, it generally pauses many collection actions, such as:

- Foreclosure activity (in many circumstances)

- Wage garnishment

- Phone calls and collection efforts

- Lawsuits and other legal collection steps

The stay is powerful, but it isn’t magic for every situation (for example, certain cases can limit the effect, and specific exceptions can apply). Your attorney will confirm what it means for your case.

If you’re overwhelmed, you don’t have to figure this out alone. You can browse guides for structured checklists, then get matched for a consult with a licensed bankruptcy attorney near you through get-matched.

Prepare by gathering the basics, understanding Chapter 7 vs. Chapter 13, learning what usually survives, and then get matched for a consult with a licensed attorney—rules vary by state and court.

Common questions

What should I bring to my first bankruptcy consultation?

Bring a list of your debts and creditors, any collection letters or court papers, and documents that show your income and key obligations (like mortgage or car statements). If you don’t have everything, bring what you have—an attorney can explain what’s missing and what matters most.

Will bankruptcy stop my wage garnishment or foreclosure right away?

In many cases, filing bankruptcy triggers the automatic stay, which can pause garnishments, foreclosures, and many collections. The details depend on your situation and your court’s rules, so it’s important to confirm specifics with a licensed bankruptcy attorney.

Does bankruptcy wipe out all my debt?

Usually not. Many types of debts can be discharged in bankruptcy, but some commonly survive, such as most student loans, recent income taxes, child support/alimony, many fines/penalties, and debts involving fraud or willful misconduct. The outcome depends on your individual facts and your location.

How much does a bankruptcy attorney cost?

Most consumer bankruptcy attorneys charge a flat fee plus the court filing fee and a small required credit-counseling fee. Total costs vary by chapter, district, and complexity—commonly something like $1,500–$3,500 for Chapter 7 and $3,000–$6,500+ for Chapter 13 (not quotes).

Is CleanSlate Match a law firm that files bankruptcy for me?

No. CleanSlate Match is a FREE matching service. We connect you with a licensed bankruptcy attorney near you, but we do not file bankruptcy and we are not your lawyer.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →