Guides

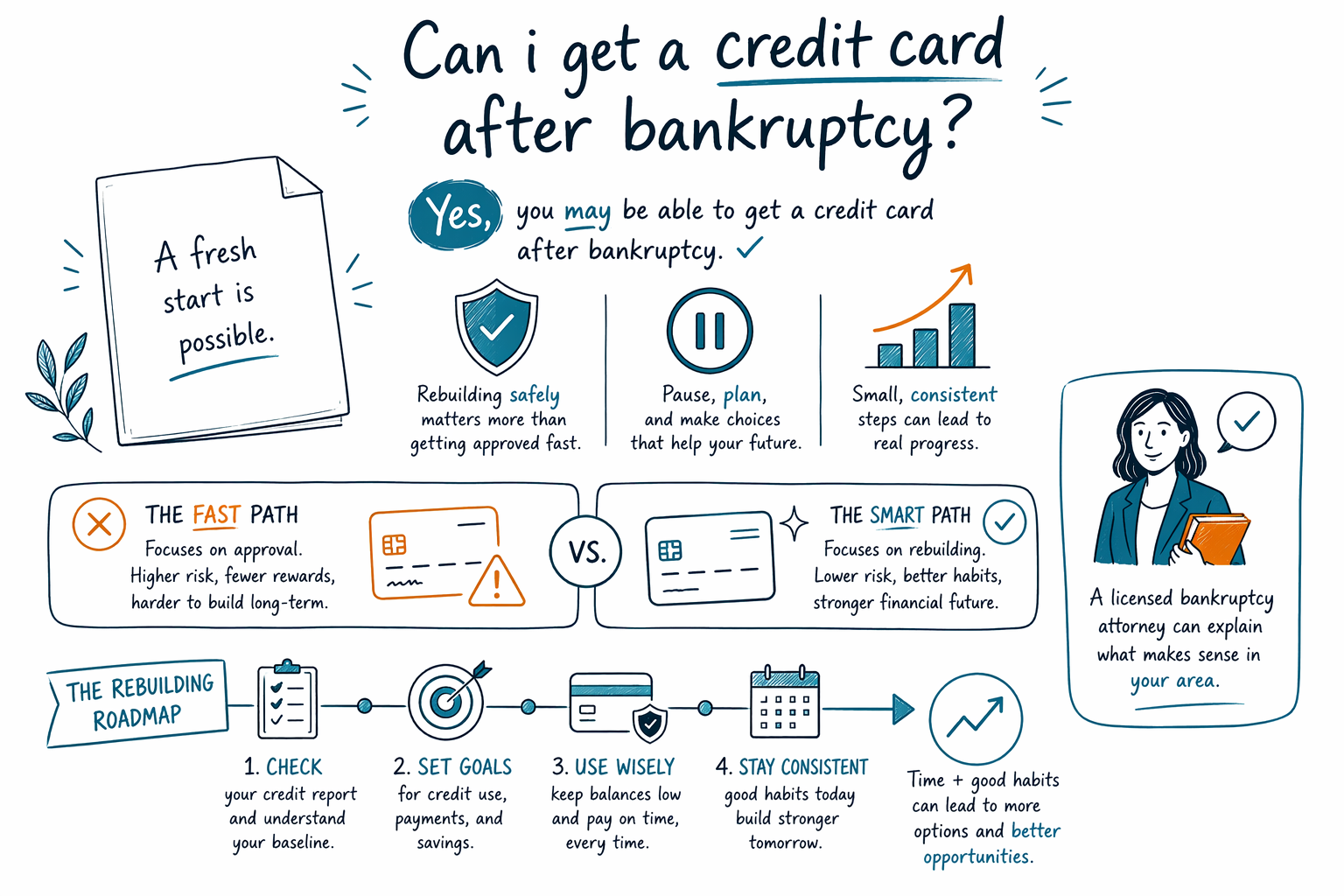

Can i get a credit card after bankruptcy?

Yes, many people can get a credit card after bankruptcy, but it usually starts with a small limit and higher costs. Bankruptcy can be a reset, not a quick fix, and the best next step depends on your full situation.

Short answer: yes, often sooner than people expect

Many people do receive credit card offers after a bankruptcy case is filed or after it is discharged. That can feel surprising, but lenders know bankruptcy may reduce some old debt and make a person easier to evaluate going forward.

Still, getting a card is not the same as getting a good card. Early offers may come with a low limit, annual fees, high interest, or a required security deposit. Approval, timing, and terms depend on the lender, your income, your credit history, and whether you filed Chapter 7 or Chapter 13.

Bankruptcy also does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud. So even if you can get a card after bankruptcy, it is important to rebuild carefully and not rely on new debt to solve old debt problems.

What changes after Chapter 7 or Chapter 13

In a Chapter 7 case, qualifying unsecured debts may be discharged fairly quickly, but the bankruptcy can remain on your credit report for years. Some lenders may still offer credit soon after discharge, especially secured cards, but the terms may be expensive at first.

In a Chapter 13 case, things can be different because you are usually in a court-approved repayment plan for three to five years. During an active Chapter 13, taking on new credit often requires court permission or your attorney's guidance. That means even if a lender is willing to offer a card, you may not be free to accept it without approval.

The details can vary by state, judicial district, and the facts of your case. If you are thinking about filing or rebuilding afterward, a licensed bankruptcy attorney in your area can explain how Chapter 7 and Chapter 13 may affect you.

What kind of credit card might be available

After bankruptcy, the easiest card to qualify for is often a secured credit card. With a secured card, you usually put down a cash deposit, and that deposit helps set your credit limit. It can be a useful tool if the card reports to the major credit bureaus and you keep the balance low.

Some people may also receive unsecured card offers. These do not require a deposit, but they may have higher interest rates, annual fees, monthly fees, or other charges. Reading the terms slowly matters. A card that looks like a fresh start can become expensive very fast.

If your goal is rebuilding credit, one simple card used carefully is usually better than several new accounts. Paying on time every month and keeping your balance low often matters more than chasing a bigger limit.

How to rebuild credit carefully after bankruptcy

A new credit card can help rebuild credit, but only if you use it in a very controlled way. The safest approach is to treat it like a tool, not extra income.

- Start with one card, not many.

- Use it for a small regular expense, like gas or a phone bill.

- Try to keep the balance low compared with the limit.

- Pay on time, every time.

- Watch for annual fees, penalty rates, and late fees.

- Check your credit reports for errors after your bankruptcy updates.

You may also be able to rebuild without rushing into a credit card right away. Stable income, on-time rent, utilities, car payments, and careful budgeting can all support a stronger financial picture over time.

If you are still deciding whether bankruptcy is the right step, our guides can help you understand the basics in plain language.

If you have not filed yet, bankruptcy is about relief first

If you are asking about credit cards because you are overwhelmed by debt now, it may help to pause and focus on the immediate problem. Consumer bankruptcy is mainly designed to give honest people a way to deal with debt pressure, stop collection activity, and create room to recover.

When a bankruptcy case is filed, the automatic stay usually pauses most collection calls, lawsuits, wage garnishments, and foreclosure actions right away. Many people also keep their home or car through exemptions or, in Chapter 13, through a repayment plan. But outcomes depend on the case, and bankruptcy is not the right answer for everyone.

A licensed bankruptcy attorney can explain what bankruptcy can and cannot do in your situation, what debts may survive, and whether there are other debt-relief options worth considering. CleanSlate Match is a free matching service, not a law firm, not a lawyer, and does not file bankruptcy or create an attorney-client relationship.

What legal help usually costs, and how to get matched for free

If you are considering bankruptcy, many consumer bankruptcy attorneys charge a flat fee for a typical case, plus the court filing fee and a small required credit-counseling fee. These are not quotes, and the real number depends on the chapter, your district, and how complex the case is.

As a very general range, Chapter 7 attorney flat fees are often around $1,000 to $2,500, plus a court filing fee that is usually a few hundred dollars and a small counseling-course cost. Chapter 13 attorney flat fees are often higher, sometimes around $3,000 to $6,000 or more, with a court filing fee also usually a few hundred dollars. In some Chapter 13 cases, part of the attorney fee may be paid through the plan, depending on local rules and the case.

Fees can go up if there are business issues, many assets, prior filings, lawsuits, tax questions, property disputes, or unusual income questions. Because rules vary by state and district, it is smart to speak with a licensed bankruptcy attorney near you and confirm the lawyer's bar license before hiring.

CleanSlate Match is free for people looking for help. We only collect contact information and general intent, such as your name, phone, optional email, state, preferred language, and a simple description of what is going on. We do not ask for a Social Security number, bank-account numbers, credit-card numbers, or detailed account balances. If you want, you can get matched with a licensed bankruptcy attorney near you.

Yes, you may be able to get a credit card after bankruptcy, but rebuilding safely matters more than getting approved fast, and a licensed bankruptcy attorney can explain what makes sense in your area.

Common questions

How soon after bankruptcy can I get a credit card?

Sometimes very soon, especially for secured cards, but the terms may not be great. In Chapter 13, you may need court permission or guidance from your attorney before taking on new credit.

Will getting a credit card after bankruptcy help my credit score?

It can help over time if you use the card lightly and pay on time every month. A new card can also hurt if it has high fees, you miss payments, or you carry too much balance.

Will bankruptcy erase all my debt so I can start over with a clean slate?

No. Some debts usually survive bankruptcy, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud. What happens depends on the type of debt and the facts of the case.

Can I apply for new credit while I am in Chapter 13?

Maybe, but you often cannot just take on new debt freely during an active Chapter 13 plan. You should ask your bankruptcy attorney first because local rules and court requirements can matter.

Is CleanSlate Match a law firm?

No. CleanSlate Match is a free matching service that helps connect you with a licensed bankruptcy attorney near you. It is not a law firm, not your lawyer, and does not give legal, tax, or financial advice.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →