Your situation

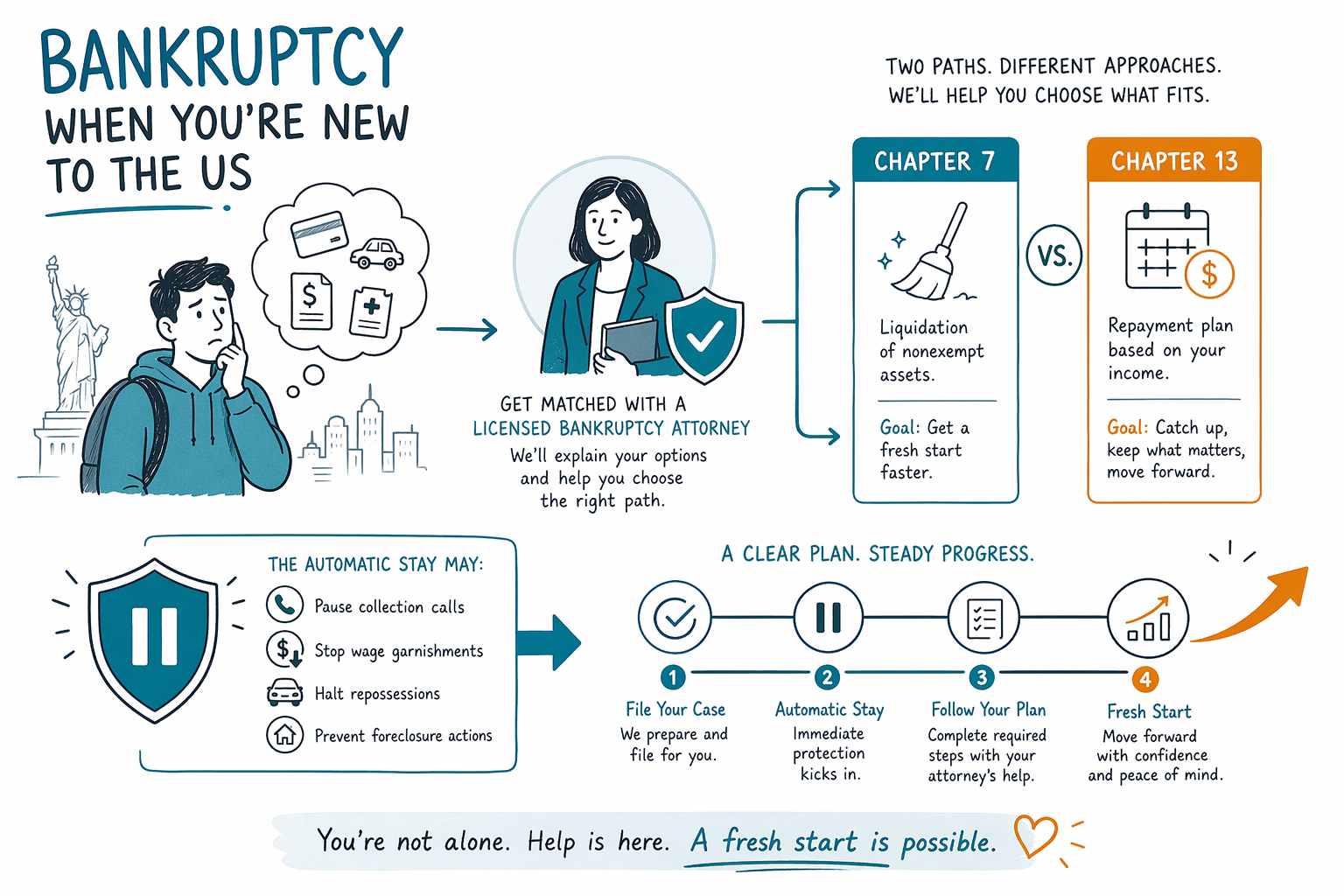

Bankruptcy When You're New to the US

If you’re new to the US and overwhelmed by debt, you don’t have to guess your next steps alone. CleanSlate Match is free and can connect you with a licensed bankruptcy attorney near you—often in your language.

You’re not alone—being new to the US can make debt feel impossible

When you arrive in a new country, the rules, letters, and deadlines around debt can feel overwhelming. You may be dealing with credit cards, medical bills, housing trouble, wage garnishment, or a lawsuit.

It’s also common to feel embarrassed or afraid to ask for help. Please know: debt problems happen to real people, and getting clear guidance early can make a big difference.

CleanSlate Match does not file bankruptcy or give legal advice. We’re a free matching service that collects only basic contact and general intent, then helps you connect with a licensed bankruptcy attorney who can explain your options for your specific situation.

Start with the basics: bankruptcy isn’t the same for everyone

Bankruptcy is a federal court process, but the details depend on where you live and what your case looks like. Chapter 7 and Chapter 13 are the two most common consumer options.

A licensed bankruptcy attorney can review your debts, income, and the timing of any collections actions (like garnishment or foreclosure) and then explain which chapter—if any—fits your situation. Rules can also change over time, so it’s important to get current, local information.

Chapter 7 vs. Chapter 13—what’s the difference?

Chapter 7 is often discussed when someone needs a quicker path to discharge for many types of debts, if they qualify under the means test. Chapter 13 is a court-approved repayment plan, usually lasting several years, that can help you catch up or restructure payments.

In many cases, Chapter 13 can be useful when you’re behind on a mortgage, have certain debts that need a structured plan, or want a specific way to manage payments. In other situations, Chapter 7 may be the better fit.

Your attorney will also discuss what most people usually learn the hard way: bankruptcy does not automatically erase every type of debt. Some debts commonly survive, and the outcome depends on the individual facts and the law in your area. If you’re unsure what applies to you, that’s exactly what an attorney consultation is for—no judgment.

Good news: collections often pause after a case is filed

If you file a bankruptcy case, an automatic stay generally goes into effect. This stay can pause many actions like most collection calls and letters, wage garnishment, and some foreclosure activity.

If you’re being sued or served with legal papers, timing matters. In the right situation, bankruptcy may stop or slow certain steps while your attorney reviews your options.

Because rules and enforcement vary, ask a licensed bankruptcy attorney about what the automatic stay means in your specific case—especially if you’ve received notice of garnishment, foreclosure, or a pending court date.

What bankruptcy usually cannot erase (and why you should ask)

Bankruptcy can help with many consumer debts, but it doesn’t necessarily “wipe out” everything. In many cases, certain debts often remain after bankruptcy, such as most student loans, recent income taxes, child support and alimony, many criminal fines, and debts connected to fraud or certain misconduct.

Also, even for debts that may be dischargeable, the court process and the facts matter. Some creditors may object, and outcomes can differ from case to case.

Because outcomes depend on your situation and the local rules, avoid anyone who promises guaranteed elimination. A good first consultation should be honest about limits while explaining your most realistic options.

What to do next (especially if you’re new to the US)

If you’re feeling overwhelmed, you don’t need to have everything perfect before you reach out. You just need to start with the right help and bring what you can.

Try these steps:

1. Make a list (in any format) of the debts you’re most worried about: housing, wages, medical bills, credit cards, and any court papers.

2. Gather notices you already have—letters, summons/complaints, garnishment paperwork, or foreclosure notices—without sharing sensitive financial account details.

3. Note key dates you can remember: when you fell behind, when you were served, and any deadlines for responses.

4. Decide what language you feel most comfortable using. You can request help in your preferred language when you get matched.

5. Book an initial consultation with a licensed bankruptcy attorney to review Chapter 7 vs. Chapter 13 and the likely impact on your specific debts and collections actions.

When you’re ready, get matched with a licensed bankruptcy attorney. You can also browse helpful overviews at bankruptcy chapters and other situations.

- CleanSlate Match is free for you and does not ask for SSNs or bank details.

Cost and what to expect from a real consultation

Attorney fees vary by complexity, the chapter you’re considering, and your local court and district procedures. Many consumer bankruptcy attorneys charge a flat fee, plus the required court filing fee and a small required credit-counseling fee.

A typical total cost can fall into a range (often a few hundred dollars for the court-related items, plus an attorney flat fee that can be higher for more complex cases). Because districts and cases differ, ranges are not guarantees, and the only way to know your realistic number is to discuss it with a licensed attorney.

In the first meeting, ask clear questions:

- Which chapter fits my situation and why?

- What debts are likely to be discharged, and what may not be?

- How does the automatic stay apply to my foreclosure, garnishment, or lawsuit?

- What is your flat fee, and what are the additional court and required fees?

- What documents do you need from me (and what should I avoid sending)?

How to verify your attorney is licensed (and avoid scams)

In bankruptcy matters, you deserve a licensed, qualified attorney. During your search and consultation, ask for the attorney’s bar status and confirm they’re authorized to practice in your state and the relevant federal bankruptcy court.

If someone pressures you, promises guaranteed results, asks for your Social Security number or bank-account numbers upfront, or refuses to explain the limits of bankruptcy clearly—that’s a red flag.

A trustworthy attorney will explain the process calmly, confirm what may or may not be dischargeable, and outline realistic next steps based on your facts.

If you’re new to the US and drowning in debt, the next step is to get matched with a licensed bankruptcy attorney who can explain Chapter 7 vs. Chapter 13 and what the automatic stay may do for your case.

Common questions

I’m new to the US. Will bankruptcy affect my immigration status?

Bankruptcy can have different effects depending on your immigration situation and the reason you filed. This is very case-specific, so ask a licensed attorney and also consider getting guidance from a qualified immigration professional if that applies to you.

I’m worried I’ll lose my home or car if I file.

Some people are able to keep their home or car in bankruptcy depending on exemptions and the type of debts they’re dealing with. An attorney can explain what may be protected in your state and how the chapter you choose could affect your assets.

Does bankruptcy stop wage garnishment and foreclosure right away?

Often, filing creates an automatic stay that can pause many collection actions, including wage garnishment and some foreclosure steps. Timing and details matter, so confirm with a licensed bankruptcy attorney based on the notices and dates you have.

Will bankruptcy erase my medical bills or credit cards?

Many credit card and medical debts may be dischargeable in the right case, but not all debts are treated the same. Your attorney can review your specific debts and explain what is likely to change after discharge.

How much does it cost to file?

Many attorneys use a flat fee, plus the court filing fee and required counseling fees. The real number depends on your chapter, your district, and how complex your situation is—so ask for a clear breakdown at the consultation. CleanSlate Match is free to use.

Related help

How the automatic stay and Chapter 13 can pause foreclosure and help you keep your home.

Open → Bankruptcy When Your Wages Are Being GarnishedHow filing can stop a garnishment quickly and protect your paycheck.

Open → Bankruptcy When You're Buried in Medical DebtHow bankruptcy treats medical bills and why it's one of the most common reasons people file.

Open →