Guides

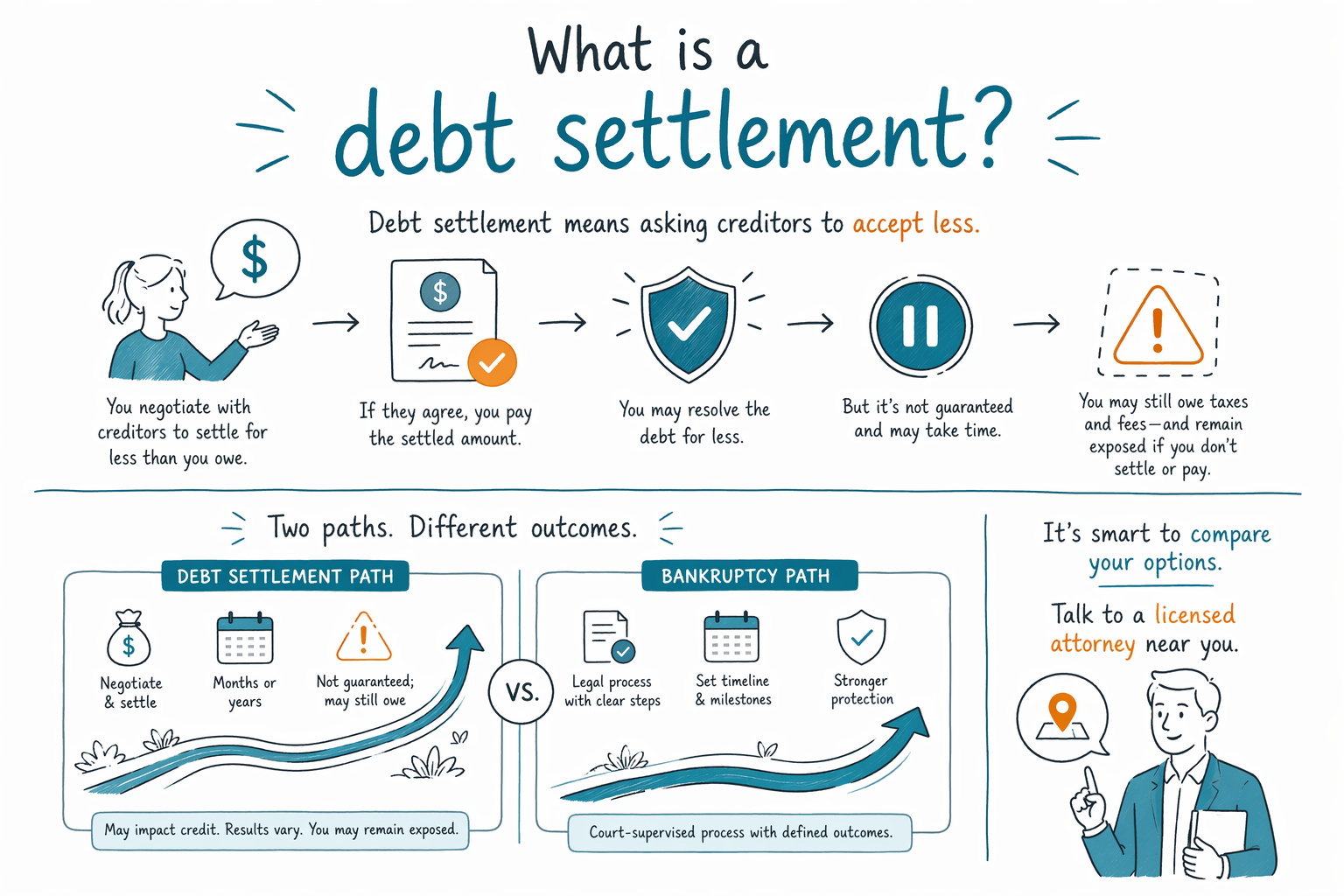

What is a debt settlement?

Debt settlement is an attempt to negotiate with creditors to pay less than what you owe. It can help some people, but it also has risks and it may not fix everything—especially if you still want to protect your paychecks or home.

Debt settlement, in plain words: what it is (and isn’t)

Debt settlement usually means contacting your creditors (or a company that negotiates for you) and asking for a reduced payoff—often after you fall behind.

It is different from bankruptcy. Bankruptcy is a court process with legal rules, deadlines, and protections. Debt settlement is not a court order, and creditors do not have to agree to reduce what you owe.

Before you consider settlement, it helps to understand the tradeoffs: settlement can take time, may affect your credit, and may create new issues like lawsuits, wage garnishment, or tax concerns depending on your situation. If you’re already facing urgent actions (like foreclosure, garnishment, or a lawsuit), you deserve a clear plan quickly—sometimes bankruptcy can pause collections sooner.

Rules vary by state and federal “local practice” in different court districts, so the safest next step is to talk with a licensed bankruptcy attorney in your area and confirm your options for your exact debts and circumstances.

How debt settlement typically works

While details vary, the common pattern is:

- You stop paying (or reduce payments) so the account shows you may be “willing but unable” to pay as agreed.

- You or a negotiator reaches out to ask for a reduced settlement amount.

- If the creditor agrees, you pay the agreed lump sum or schedule.

- Anything you don’t pay may remain your responsibility unless it is formally released in writing.

Because creditors can refuse, settlement often involves uncertainty. Also, if you do not pay for a period, your account may be sent to collections or you may be sued or garnished. You can’t assume settlement will prevent those outcomes.

If you’re considering settlement, ask practical questions up front: Will the creditor provide a written release? How will you make sure you have proof of payment? What happens if the negotiation fails? And what plan do you have if collections actions are already underway?

Risks and downsides to know before you choose settlement

Debt settlement can be tempting when you feel overwhelmed, but it comes with real risks.

- Credit impact: Your credit score often takes a hit before any settlement is reached.

- Lawsuits and wage garnishment: Falling behind can lead to court cases, garnishment, or other collection actions.

- Timing: Settlement is not usually quick, and progress depends on creditor decisions.

- “Not all debts settle the same”: Some debts are harder to settle than others.

There may also be tax-related issues in some situations when a debt is forgiven or reduced. That can be complex and depends on your personal circumstances. A licensed professional can explain what may apply to you.

If you want to explore options that include court protections—like pausing collections or stopping certain garnishments—you’ll want to compare settlement with bankruptcy. Bankruptcy rules vary by state and district, and your best path depends on your income, household situation, and the specific debts involved.

Debt settlement vs. bankruptcy: what’s the difference for you?

Debt settlement is a negotiation. Bankruptcy is a legal process in bankruptcy court.

A key difference is timing and protection. When a bankruptcy case is filed, an automatic stay generally goes into effect, which can pause many collection actions—like most collection calls, lawsuits, garnishments, and foreclosures—while the case is pending.

With bankruptcy, the outcome depends on what chapter applies to you:

- Chapter 7 often can discharge many qualifying unsecured debts, but rules vary, and some debts usually survive.

- Chapter 13 creates a court-approved repayment plan, which can sometimes help you catch up on certain debts over time.

Either way, bankruptcy can be a structured way to regain control—but it is not a magic eraser. Many debts often survive, including most student loans (usually require special handling), recent income taxes, child support or alimony, many court fines, and debts related to fraud or certain wrongdoing. Exact results depend on your case.

If you’re unsure whether settlement or bankruptcy makes more sense, that first conversation with a licensed bankruptcy attorney is important. They can review your situation, explain what likely survives, and help you choose the safest option based on your state and district.

What to do next if you’re considering settlement (or you’re not sure)

If you’re stressed and trying to make a decision, start by getting clear answers—not promises.

- List the debts that feel most urgent (mortgage/late housing, garnishment, lawsuit, biggest creditor).

- Find out whether you’re already in a legal process (court papers, garnishment orders, foreclosure notices).

- Get a local licensed bankruptcy consultation to compare settlement vs. bankruptcy for your actual situation.

CleanSlate Match can help you get connected with a licensed bankruptcy attorney near you. It’s free for you and it does not file anything—our role is matching you for a conversation.

To get matched, use get matched. Share only contact information and a general sense of your situation and preferred language—never SSNs, bank details, or account balances.

And one more honest reminder: bankruptcy and its available protections vary by state and bankruptcy district, and rules can change. Confirm details with a licensed attorney in your area.

Debt settlement means asking creditors to accept less, but it’s not guaranteed and it may still leave you exposed—so it’s smart to compare it with bankruptcy by talking to a licensed attorney near you, with help from CleanSlate Match.

Common questions

Will debt settlement stop collectors or wage garnishment?

Debt settlement itself is not a court order, so collectors may continue their actions while you negotiate. In contrast, bankruptcy can create an automatic stay that pauses many collections after a case is filed. If you already have garnishment, a lawsuit, or foreclosure, talk to a licensed bankruptcy attorney right away to understand the fastest safe option for your situation.

What debts usually can be settled?

Many unsecured debts (like some credit cards or some medical bills) are sometimes negotiable, but creditors can refuse and settlement terms vary. Secured debts (like a mortgage or car loan) usually follow different rules. A local bankruptcy attorney can explain how these debts typically work in your state and district.

Is debt settlement a guaranteed way to pay less and get out of debt?

No. Creditors do not have to agree, and settlement can take time and may require you to fall behind first. Even if a settlement is reached, some issues may remain unless the creditor provides a clear written release of the obligation.

How does bankruptcy compare if I’m thinking about settlement?

Bankruptcy is a legal process with specific chapters and court protections. Depending on your case, it may pause certain collections through the automatic stay, and it may discharge or repay certain debts—but some debts commonly survive, like many student loans, recent income taxes, child support/alimony, most fines, and debts tied to fraud. A licensed bankruptcy attorney can review what likely applies to you.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →