Free guides

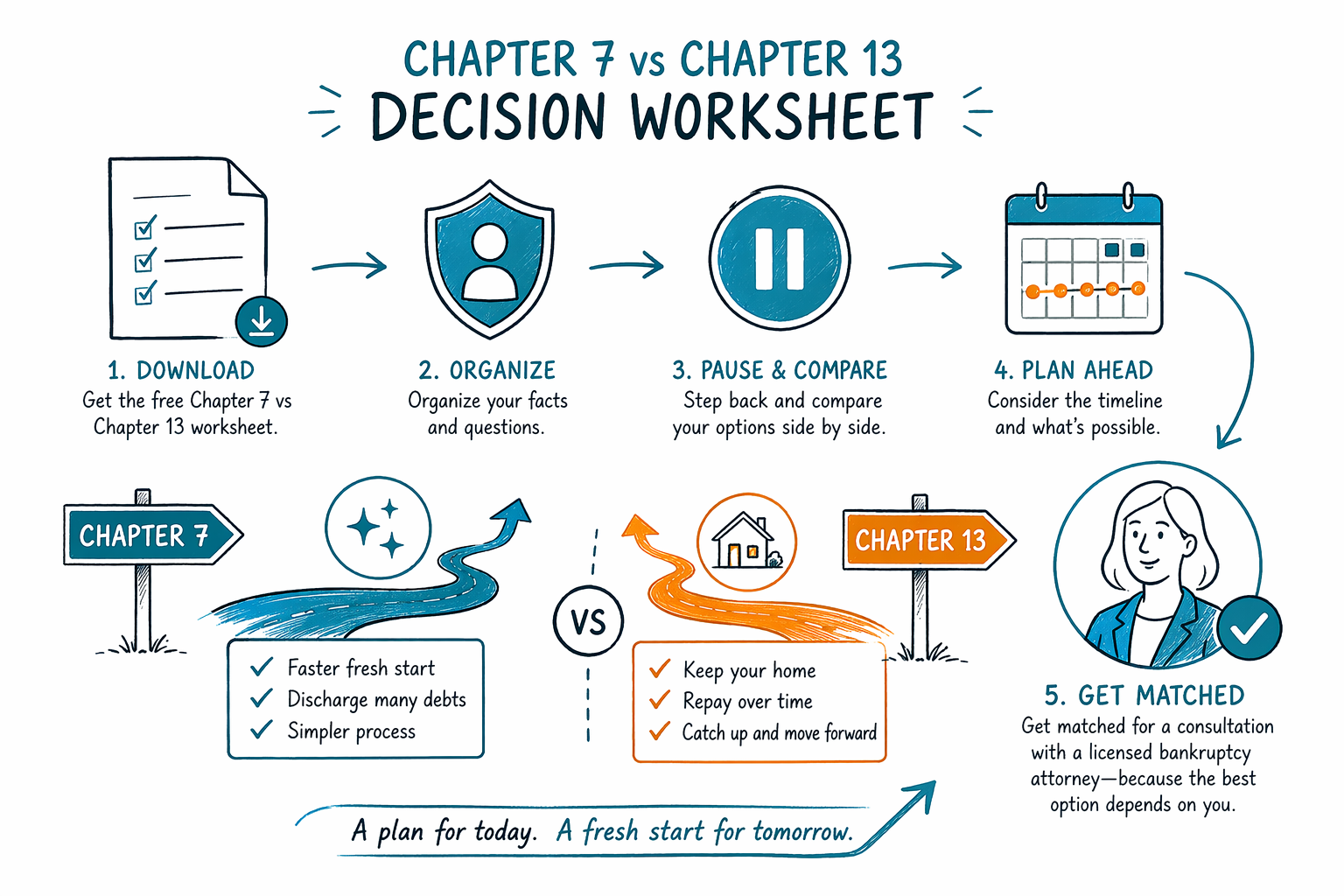

Chapter 7 vs Chapter 13 Decision Worksheet

If you’re overwhelmed by debt, this free worksheet can help you organize the facts that matter when deciding between Chapter 7 and Chapter 13. You’ll leave with clearer questions for a licensed bankruptcy attorney.

What this free worksheet helps you do

This PDF checklist is designed to help you think through Chapter 7 vs. Chapter 13 in a calm, step-by-step way—before you talk to a lawyer.

It does not file anything and it does not decide your case for you. Bankruptcy outcomes depend on your full situation, and bankruptcy rules can vary by state and federal district. A licensed bankruptcy attorney will review the details and tell you what’s realistic for you.

You can use this guide even if English isn’t your first language—by taking your answers (in your language if you prefer) to your consultation so you can explain what’s happening clearly.

What’s inside the Chapter 7 vs Chapter 13 Decision Worksheet (PDF)

The worksheet is built to capture the common “decision points” that attorneys review first. It’s also meant to reduce stress by turning confusing problems into a simple list.

You’ll typically see sections like:

- Your debt types (credit cards, medical bills, personal loans, collections, lawsuits, mortgage arrears, etc.)

- Whether you’re dealing with foreclosure, eviction threats, wage garnishment, or an active lawsuit

- Your income situation (for example, whether your income seems steady, changing, or recently reduced)

- Whether you may need more time to catch up on certain debts (like a home)

- Key deadlines and notices you’ve received (without needing account numbers)

- Questions to ask an attorney about your best chapter option, costs, and what will happen after filing

Tip: Bring the worksheet to your appointment. It helps you remember details and makes it easier for the attorney to assess the right next step.

Who this worksheet is for

This download is especially helpful if you feel stuck between two thoughts: “I want a fresh start” and “I’m not sure I can handle a repayment plan.”

It can help if you’re:

- Behind on bills and getting collection calls

- Facing wage garnishment or a lawsuit

- Worried about losing a home or car

- Considering Chapter 7 but unsure whether Chapter 13 might fit better

- Considering bankruptcy for the first time (including people new to the US)

Even if you end up learning that bankruptcy may not be the best fit, the worksheet still helps you understand what to ask and what documents to gather for a truthful legal consult.

How to use it before you meet an attorney

Use the worksheet when you have a little quiet time—then save a copy so you can update it as new notices come in.

- Read the instructions once, then go section by section.

- Write down what you know in plain language (for example: “garnishment started last month” or “received foreclosure notice”).

- If you don’t know something yet, leave it blank—an attorney can help you identify what matters.

- Do not include sensitive account details. You don’t need SSNs, bank numbers, or login info.

- Circle the areas that feel most urgent (foreclosure, garnishment, lawsuit, or threats to a vehicle).

- Bring the completed worksheet to your consultation and confirm the attorney’s bar license.

If you want extra background before you decide, you can also review our educational hubs here: guides and chapters.

Honest limits: what bankruptcy may and may not do

It’s normal to hope a filing will “erase everything.” But bankruptcy is not a magic wipe. Some debts usually survive bankruptcy, and outcomes depend on your exact facts.

In many cases, bankruptcy does not automatically erase:

- Most student loans

- Certain recent income taxes

- Child support or alimony

- Many court fines/penalties

- Debts involving fraud or other misconduct

A licensed attorney can explain which debts are commonly dischargeable in your situation and what might require separate handling. For more context on chapter differences, see chapters and get matched for a legal consult via get-matched.

Next step: download free, then get matched to a licensed bankruptcy attorney

This worksheet is a free starting point. It helps you show up to your first meeting organized and ready—so you can get clear answers without feeling rushed.

CleanSlate Match is a free matching service. We are not a law firm, we are not a lawyer, and we do not file bankruptcy or create an attorney-client relationship. A participating licensed attorney will review your case and advise you based on the law in your area.

Cost can vary. Most consumer bankruptcy attorneys charge a flat fee (in addition to the court filing fee and a small required credit-counseling fee), and the total range depends on the chapter, complexity, and your district. A good attorney will explain costs clearly upfront—without guarantees about results.

Download the free Chapter 7 vs Chapter 13 worksheet to organize your facts and questions—then get matched for a consultation with a licensed bankruptcy attorney, because the best option depends on your specific situation.

Common questions

Is this worksheet legal advice?

No. The worksheet is general educational information to help you organize questions and facts. Bankruptcy rules vary by state and federal district, so your specific options should be reviewed by a licensed bankruptcy attorney.

Do I need to bring my bank statements or account numbers?

Usually you should avoid sharing sensitive financial-account details unless your attorney specifically asks for them. For the worksheet and first meeting, your goal is to describe what’s happening—without SSNs or account numbers.

Will Chapter 7 or Chapter 13 definitely eliminate my debt?

Not necessarily. Some debts often survive bankruptcy, such as many student loans, certain recent taxes, child support/alimony, many court fines, and debts related to fraud. Your attorney can explain what may be dischargeable in your case.

How do I use this if I’m dealing with foreclosure or garnishment?

Mark what notices you received and what date things started (as best as you can). When a bankruptcy case is filed, an automatic stay often pauses many collections, garnishments, foreclosures, and lawsuits—your attorney can explain how that applies to your situation.

Related help

A free, printable checklist of the documents to gather before you meet a bankruptcy attorney.

Open → The Means Test Prep GuideA free plain-language guide to the income figures and paperwork the means test looks at.

Open → The Monthly Budget WorksheetA free template to map your income and expenses — useful for credit counseling and a Chapter 13 plan.

Open →