Free guides

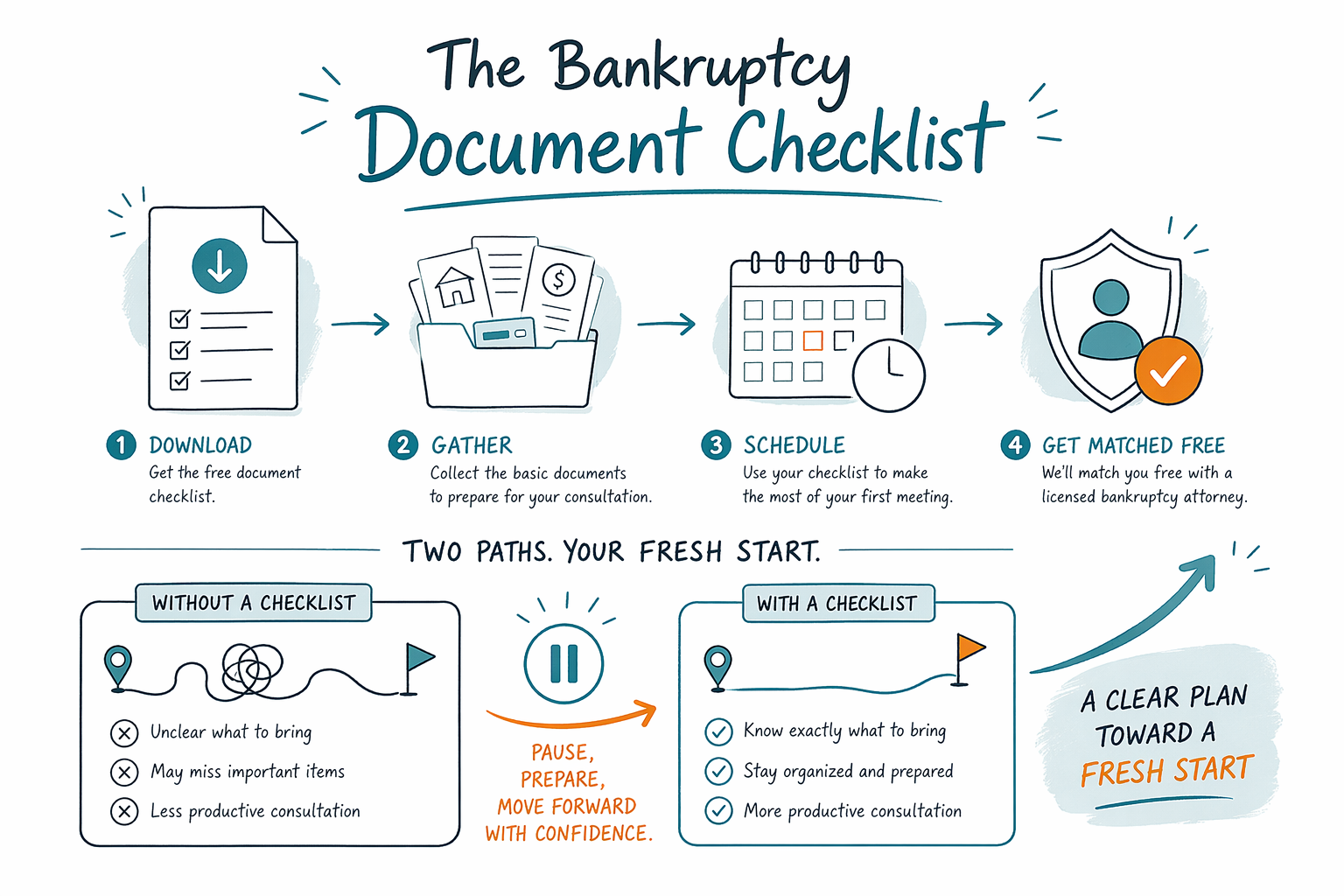

The Bankruptcy Document Checklist

Take a breath—you don’t have to remember everything about your money troubles. This free checklist helps you gather the most important documents so your first bankruptcy consultation is clearer and less stressful.

What this free checklist (PDF) includes

This document checklist is a practical worksheet you can print or fill in while you get ready for a first meeting with a licensed bankruptcy attorney.

It’s organized around the information attorneys typically need to evaluate your situation and choose the right path (often Chapter 7 or Chapter 13). It also includes a section for practical “what happened” details—like missed payments, a pending lawsuit, foreclosure steps, or wage garnishment—so nothing important gets lost.

The goal is not to “prove you deserve help.” It’s to help you bring the basics in an organized way, even if you’re overwhelmed, behind on paperwork, or new to the United States.

Note: This is general educational information. Bankruptcy rules, forms, and what counts as “required” can vary by state and by federal judicial district, and they can change over time.

Who this resource helps most

This checklist is designed for people who feel drowning in debt—credit cards, medical bills, an eviction risk, a mortgage they’re behind on, wage garnishment, or a court case—and want a calm, orderly way to prepare.

It can also help if you’re a non-native English speaker or new to the US. Instead of trying to interpret complicated legal wording, you’ll follow a step-by-step gathering plan.

If you’ve never filed bankruptcy before, or you’re not sure whether Chapter 7 vs. Chapter 13 fits your situation, having your documents ready can make your consultation more efficient and less stressful.

How to use the checklist before you meet an attorney

You can use this as a “pack-it-up” guide over a few days or a few weeks, depending on your situation. Don’t worry if you can’t find everything right away—bring what you have and note what’s missing.

- Start with what’s easiest: recent pay stubs, a recent bank/asset statement (if you have one), and the latest bills/letters from creditors or the court.

- Work section-by-section: tick off each item as you gather it.

- If a document is in another person’s name, or you’re missing paper copies, write down what you know (for example, the creditor name, case number if you have it, and the date you received the notice).

- Make a simple “timeline” using the worksheet space: when you fell behind, when collection actions started, and any upcoming deadlines (like a foreclosure date or hearing date).

If you’re facing urgent deadlines—like an eviction, foreclosure sale, or a court hearing—try to bring everything you have that mentions the date, even if it’s incomplete.

What bankruptcy can and can’t do (so you’re not misled)

Bankruptcy is often a fresh start, but it’s not magic. Outcomes depend on your specific facts, your state, and your district.

In many cases, once a bankruptcy case is filed, an “automatic stay” can pause many collection actions such as lawsuits, wage garnishments, and foreclosure steps while the case proceeds. That can bring immediate breathing room for many people.

However, some debts usually do not get erased in typical consumer bankruptcy cases, including most student loans, recent income taxes, child support/alimony, many court fines, and debts involving fraud or certain misconduct. Your attorney will explain what might be dischargeable (and what usually survives) in your particular case.

This checklist is meant to help you prepare questions and documents—not to guarantee any result.

Costs and expectations for your consultation

Many licensed consumer bankruptcy attorneys charge a flat fee for the work involved in a Chapter 7 or Chapter 13 case, plus the court filing fee and a small required credit-counseling fee. The exact range varies by chapter, complexity, and the district.

Because ranges aren’t quotes, the best next step is to speak with a licensed bankruptcy attorney in your area to confirm the total cost that applies to your situation.

Be cautious of anyone who promises a guaranteed debt wipeout, a specific outcome, or a “one size fits all” answer. A serious attorney will review your documents, explain options honestly, and confirm what can happen in your case.

If you’re ready, you can get matched for free to a licensed bankruptcy attorney near you through CleanSlate Match at Get matched. Before you meet, you should also confirm the attorney’s license through your state bar.

Download and use the free document checklist to gather the basics for your first bankruptcy consultation—then get matched free to a licensed bankruptcy attorney to review your situation.

Common questions

Do I need every document listed to meet with an attorney?

No. Bring what you have and use the checklist to note what’s missing. Attorneys typically can work with incomplete records and may suggest alternatives to obtain needed information.

Is this checklist legal advice or a substitute for an attorney?

No. CleanSlate Match provides general educational information and a free document checklist. It’s not legal advice and it doesn’t replace a consultation with a licensed bankruptcy attorney.

Will the checklist guarantee my debts will be erased?

No. Bankruptcy outcomes vary, and some types of debt usually survive—such as most student loans, recent income taxes, child support/alimony, many fines, and debts involving fraud. Your attorney can explain what may be discharged in your case.

How does this help if I’m new to the US or don’t speak English well?

The checklist is designed to reduce confusion by organizing the basics you need to collect. You can also list any language preference when you request a match so you’re more comfortable during the process.

Related help

A free worksheet to help you weigh which chapter may fit your situation before you talk to a lawyer.

Open → The Means Test Prep GuideA free plain-language guide to the income figures and paperwork the means test looks at.

Open → The Monthly Budget WorksheetA free template to map your income and expenses — useful for credit counseling and a Chapter 13 plan.

Open →