Guides

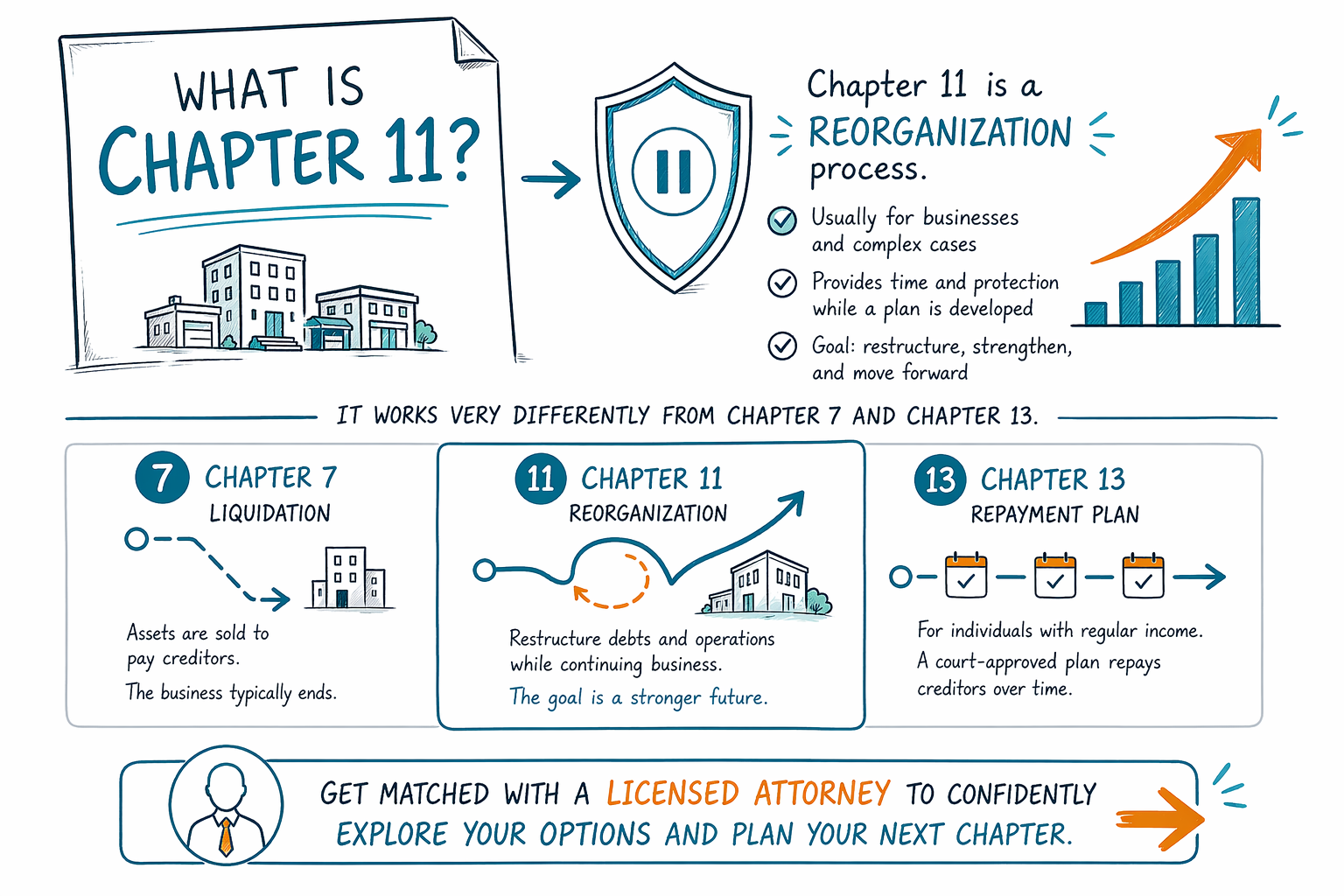

What is chapter 11?

Chapter 11 is a bankruptcy process mainly used by businesses (and in some cases large or complex individuals) to reorganize debts and keep operating. It’s very different from Chapter 7 and Chapter 13.

First, the direct answer: what is Chapter 11?

Chapter 11 is a court-supervised process for reorganizing debts instead of simply liquidating assets. The goal is often to keep a business running (or maintain operations) while working out a workable plan to repay creditors over time.

In many consumer situations, people do not use Chapter 11 because it is usually more complex and can be more expensive than Chapter 7 or Chapter 13. Whether it makes sense depends on your facts, your state, and the local court rules.

Important: CleanSlate Match is a free matching service, not a law firm and not your lawyer. We can help you find a licensed bankruptcy attorney near you who can explain the right chapter for your situation.

Rules vary by state and by federal judicial district, and bankruptcy law can change. A licensed bankruptcy attorney in your area can confirm what applies to you.

How Chapter 11 works (plain language)

Chapter 11 typically involves filing with the bankruptcy court, attending required hearings, and submitting a “reorganization plan.” Creditors get involved through the court process, and the plan generally must meet legal requirements.

Instead of a simple “wipeout” approach, Chapter 11 usually focuses on restructuring: changing payment terms, the timing of payments, and sometimes reducing certain debts (depending on the type of debt and the plan).

Chapter 11 can involve more paperwork, more reporting, and more legal work than other consumer chapters. Because of that, it’s often used when the debt situation is large or complicated.

If you’re considering bankruptcy, ask an attorney to compare Chapter 11 with Chapter 7 or Chapter 13 for your specific case before deciding.

Chapter 11 vs. Chapter 7 and Chapter 13

Chapter 7 is usually a liquidation-style process for many individuals: eligible debts may be discharged, and the court process often moves more quickly. Chapter 13 is a repayment plan over time (often 3–5 years) where you pay creditors through a court-approved plan.

Chapter 11 is built for reorganization and can be more detailed, with longer timelines and more court oversight. In practice, many individuals are guided toward Chapter 7 or Chapter 13 unless there’s a specific reason Chapter 11 is better.

Also, the automatic stay is important across bankruptcy chapters: when a bankruptcy case is filed, the stay generally pauses many collections, foreclosures, lawsuits, and wage garnishment actions. The exact effect depends on the case and timing.

Because outcomes depend on the individual facts and the court, confirm your options with a licensed bankruptcy attorney.

What bankruptcy often can’t erase (including in Chapter 11)

Bankruptcy does not erase every type of debt. Even when debts are dischargeable, the court treats certain obligations differently.

Many debts often survive bankruptcy, including (but not limited to) most student loans (usually unless a specific hardship test is met), recent income taxes, child support and alimony, most court fines/penalties, and debts related to fraud or certain misconduct. The outcome can vary by facts and the type of debt.

This is one reason it’s important to review your full list of debts with a licensed bankruptcy attorney. A good attorney will explain what may be dischargeable and what usually is not—without promising a guarantee.

Cost and timing: why Chapter 11 can be much more than other chapters

Chapter 11 is often more expensive and complex because of the level of legal work, court filings, and ongoing management/reporting that may be required. Fees vary widely based on the complexity of your case and the attorney’s approach.

In general, many consumer bankruptcy attorneys charge a flat fee for Chapters 7 or 13 (plus the court filing fee and a small required credit-counseling fee). Chapter 11 is different—costs are frequently higher because the work is more involved. Your attorney can share a fee structure and estimate based on your circumstances.

As a rough guide for budgeting: total costs in a bankruptcy filing commonly include a court filing fee (often a few hundred to a few thousand dollars depending on the chapter) plus other required fees. Any exact amount depends on your chapter, your district, and what your case needs.

Be cautious of anyone who promises guaranteed outcomes or a “one-size-fits-all” price. Ranges are not quotes, and an attorney’s review is needed to understand your situation.

What to do next if you’re wondering about Chapter 11

If you’re overwhelmed by debt, the first step is to understand which chapter is most appropriate for you—often Chapter 7 or Chapter 13, even if you initially thought about Chapter 11.

You can start by collecting basic information (not bank numbers or sensitive account details): your debts, major creditors, any lawsuits/foreclosures/garnishments, and your general income situation. Then discuss your options with a licensed bankruptcy attorney.

Use the free matching service to connect with an attorney who can explain your chapter options and what may happen to collections, foreclosures, and garnishments after filing.

If you’re unsure whether an attorney is licensed, you can confirm their bar membership through your state’s lawyer directory.

Chapter 11 is a bankruptcy “reorganization” process, usually for businesses and complex cases, and it works very differently from Chapter 7 and Chapter 13—get matched with a licensed attorney to confirm your best option for your state and district.

Common questions

Is Chapter 11 only for businesses?

Mostly, yes. Chapter 11 is designed for reorganization and is commonly used by businesses, though in some situations individuals with very complex or large cases may also consider it. A local bankruptcy attorney can tell you which chapter usually fits your facts.

Will Chapter 11 stop collections, foreclosure, or wage garnishment?

Often, yes—when a bankruptcy case is filed, an automatic stay generally pauses many collection actions, including many foreclosures, lawsuits, and wage garnishments. The exact effect can depend on your case history and timing, so confirm details with a licensed attorney.

Does Chapter 11 discharge all my debts?

Not automatically, and not always. Some debts often survive bankruptcy, such as many student loans, recent income taxes, child support/alimony, many fines/penalties, and debts connected to fraud or certain misconduct. The dischargeability depends on your situation and the specific debt.

What does it cost to file Chapter 11?

Costs vary a lot based on complexity and the attorney’s fee structure. Total costs generally include attorney fees plus court filing fees and required fees. Many consumer attorneys use flat fees for Chapter 7 or 13, but Chapter 11 is often more involved and can cost more—your attorney can explain a case-based range.

Are the rules the same everywhere in the US?

No. Bankruptcy rules and how courts apply them can vary by state and by federal judicial district, and the law can change. It’s important to speak with a licensed bankruptcy attorney near you for guidance that fits your district.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →