Guides

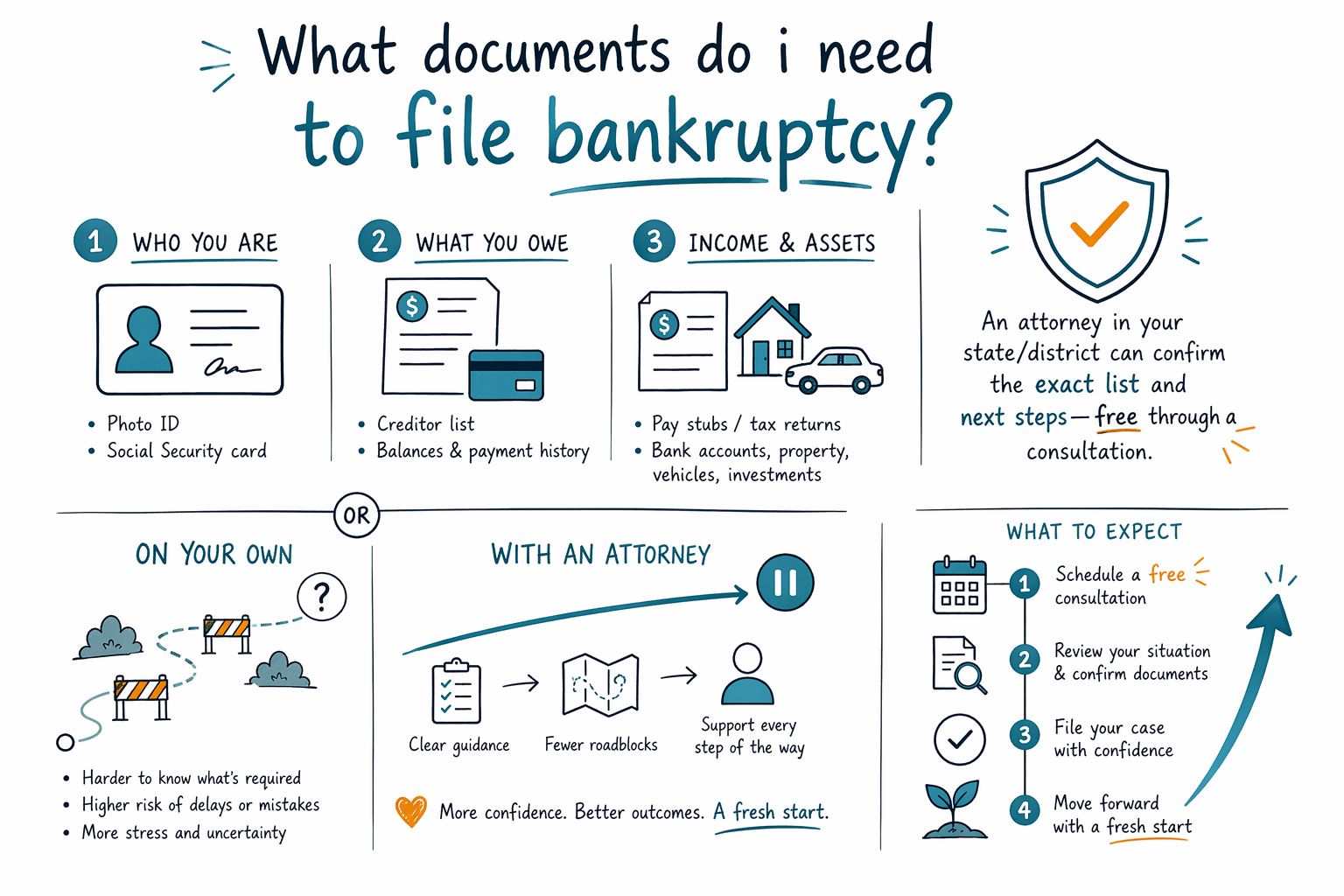

What documents do i need to file bankruptcy?

Yes—there are documents bankruptcy courts usually require, and gathering them can feel overwhelming. This guide explains the most common paperwork, what to bring first, and how a licensed attorney will help you organize it.

First: what you usually need to file (the honest overview)

Bankruptcy paperwork is mainly about your identity, your debts (who you owe and how much), your income (what you earn), and your assets (what you own). The exact forms and required documents vary by state and by federal judicial district, so your attorney may ask for a slightly different set.

CleanSlate Match is a FREE matching service—we don’t file bankruptcy and we’re not a lawyer. For legal advice about what to submit in your area, you’ll want to confirm details with a licensed bankruptcy attorney near you.

In general, most people get the best results by starting with the debt list and recent income documents, then filling in the rest. If you don’t have something, tell your attorney—there are often ways to reconstruct records.

- Rules and document needs vary by state and district (and can change over time).

- If you’re missing documents, that doesn’t always mean you can’t file—your attorney will guide you.

Documents you need for Chapter 7 (common categories)

Chapter 7 is often chosen when you can’t repay debts through a plan. Courts still require detailed information, including income, expenses, assets, and your list of creditors.

Common documents include:

1. Your photo ID and proof of your Social Security number are typically requested by your attorney for filing, but CleanSlate Match never asks for SSNs—your attorney will.

2. Pay stubs and recent income documents (and any proof of other income).

3. A list of all debts: credit cards, medical bills, utilities, personal loans, and any lawsuits or judgments.

4. Bank statements and statements for any accounts you use—some attorneys request a specific number of months.

Because Chapter 7 can include a means test, your attorney may also request documents that show your income and household expenses in the correct way for your district.

- You’ll typically provide proof of identity, income, expenses, assets, and a complete creditor list.

- The means test documentation requirements depend on your district and your situation.

Documents you need for Chapter 13 (common categories)

Chapter 13 focuses on creating a repayment plan, usually over several years. That means courts require more detail about your income and your plan-related expenses.

Common documents include:

1. Recent pay stubs or income records, plus documentation of any other income.

2. Tax returns (many attorneys request recent years).

3. A list of all debts, including secured debts (like a car loan or mortgage).

4. Proof of value for certain assets, especially vehicles, and sometimes proof of insurance.

Your attorney will also collect information needed to set up the payment plan and handle special items like past-due mortgage amounts, arrears, or creditor claims. Outcomes vary—your attorney will review what can be kept under exemptions and what the plan can address in your case.

- Chapter 13 usually requires extra paperwork because a repayment plan must be supported with documents.

- What you can keep and how debts are treated depends on your state and district.

The “debt and property” documents that matter most

Even if you’re scared or embarrassed, the court needs clear lists. Start by gathering anything that shows who to contact and how much you owe.

Most helpful debt documents include:

- Billing statements or account summaries (credit cards, store cards, personal loans)

- Medical bills and collection notices

- Letters from creditors, debt collectors, or attorneys

- Lawsuit papers or judgment documents (if you received any)

- Mortgage statements and notices of default/foreclosure (if you have a mortgage issue)

For assets and expenses, many attorneys ask for:

- Recent bank statements and statements for retirement accounts (if applicable)

- Lease agreement (if you rent)

- Car loan/lease documents, recent payment history, and insurance info

- Pay stubs, utility bills, and proof of household expenses

If you don’t have a document, tell your attorney. Sometimes you can request duplicate copies from creditors or reconstruct totals from your records.

- If you gather only two things first: your complete creditor list and your most recent income documents.

- Missing records are common—your attorney can often help you fill gaps.

Important limits: bankruptcy doesn’t erase every kind of debt

Many people come to bankruptcy hoping for relief, and a lot of collectors stop quickly once a case is filed. Still, it’s important to be honest: some debts usually don’t go away in bankruptcy.

Debts that often survive include (depending on the details):

- Most student loans (very specific hardship rules apply)

- Recent income taxes in many cases

- Child support and alimony

- Many court fines and penalties

- Debts from fraud or certain willful/wrongful conduct

Also, which debts are included can depend on your chapter, the facts of your case, and your district’s procedures. Your licensed attorney will review your documents and tell you which debts may be discharged and which may not.

- The filing process can pause many collections, foreclosures, and lawsuits, but it doesn’t guarantee all debt will be wiped out.

- Ask your attorney what is likely to survive in your specific case.

How to prepare before you meet an attorney (a simple checklist)

If you’re ready to take the next step, you don’t have to have everything perfect. The goal is to bring what you have and organize it so your attorney can quickly understand your situation.

Before your consultation, try this:

1. Make a list of every creditor and account (name of company, what it’s for, and roughly how much you owe).

2. Gather your most recent pay stubs or income documents.

3. Collect recent bank statements and a summary of monthly expenses (rent/mortgage, utilities, transportation, food).

4. Gather loan/lease documents for your car and mortgage statements if you have them.

5. Put aside any court papers: lawsuits, garnishment notices, or judgments.

When you’re ready, you can use get matched to connect with a licensed bankruptcy attorney near you. You can also explore chapters and our guides to understand the basics before your call.

- Be prepared, not perfect—your attorney can help you fill gaps.

- Document needs vary by state and district, so confirm your exact list with a licensed attorney.

What it typically costs to get help (so there are no surprises)

Most consumer bankruptcy attorneys charge a flat fee, plus the required court filing fee and a small required credit-counseling fee. The exact total depends on whether you file Chapter 7 or Chapter 13, how complex your case is, and your judicial district.

As a general sense of budgeting, flat fees often fall in ranges like these (not quotes):

- Chapter 7: often around $1,000–$3,500 plus the court and counseling fees.

- Chapter 13: often around $3,000–$6,000+ plus the court and counseling fees.

These ranges can go up if there are multiple assets, a foreclosure or significant secured debt, recent income complexity, prior filings, or additional filings needed in your district. Your attorney will review your documents and explain the expected cost before you move forward.

- These are typical educational ranges, not guarantees or quotes.

- Your consultation with a licensed attorney should include total expected fees and court costs.

Most bankruptcy filings require documents showing who you are, what you owe, and your income and assets—and an attorney in your state/district can confirm the exact list and next steps, free through a match.

Common questions

I’m overwhelmed. Do I need to gather every document before I talk to an attorney?

Not always. Most attorneys prefer you bring what you have—especially your creditor list and income documents—then they’ll tell you what’s missing and how to get it. Rules and document lists vary by state and district, so your attorney will confirm your exact needs.

What if I don’t have pay stubs or tax returns?

That happens. Your attorney will review your situation and may ask for substitutes such as employer statements, bank records, or transcripts. Don’t guess totals—tell your attorney what you do have.

Will CleanSlate Match ask me for my Social Security number or bank account details?

No. CleanSlate Match is a FREE matching service and we only collect contact and general intent (name, phone, optional email, state, language, and a general sense of your situation). We do not ask for SSNs or financial-account numbers.

Will filing bankruptcy stop foreclosure or a wage garnishment?

Often, yes. Once a bankruptcy case is filed, an “automatic stay” generally pauses many collections, including many foreclosures and wage garnishments. The details depend on your case and timing, so confirm specifics with a licensed bankruptcy attorney near you.

If I file bankruptcy, will all my debts be wiped out?

Not always. Some debts usually survive, such as most student loans, certain recent income taxes, child support/alimony, many fines/penalties, and debts involving fraud or certain misconduct. A lawyer can review your documents to explain what may or may not be discharged in your specific situation.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →