Guides

Does bankruptcy clear student loans?

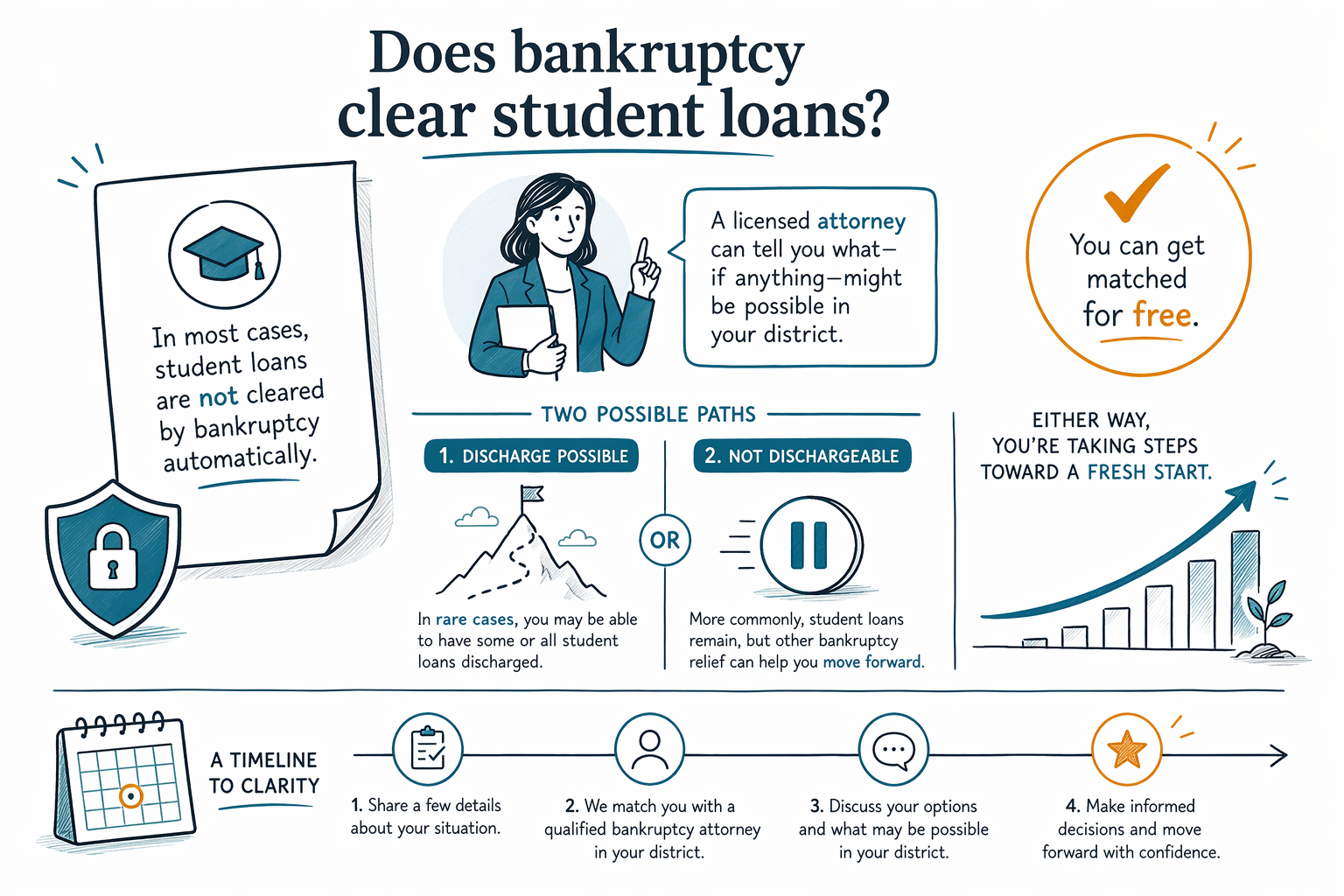

Usually, bankruptcy does not automatically wipe out student loans. This guide explains the general rule, the limited exceptions, and how to talk with a licensed bankruptcy attorney near you for a real answer.

Short answer: usually, no—student loans typically don’t get cleared in bankruptcy

In most cases, student loans are not discharged (cleared) in a Chapter 7 or Chapter 13 bankruptcy just because you file. Federal student loans and many other education debts have specific bankruptcy rules that make discharge difficult.

That said, there can be exceptions. A bankruptcy attorney can review your situation to see whether your student loan qualifies for a discharge in bankruptcy under the narrow rules that apply.

Because student loan treatment and bankruptcy procedure can depend on your district and facts, rules vary by state and judicial district. A licensed bankruptcy attorney can confirm what’s possible where you live.

- Bankruptcy is not an automatic “student loan delete” button

- Some borrowers may qualify for discharge in limited situations

What “discharge” means (and why student loans are different)

A bankruptcy discharge is the court’s order that tells the creditor the debt must be treated as paid/removed under bankruptcy rules. For many debts—like credit cards and medical bills—discharge is often possible.

Student loans are treated differently. In bankruptcy, you generally need to prove a special standard to discharge them. The process can be separate from the main bankruptcy paperwork, and it may require extra evidence.

So even if other debts get reduced or cleared, student loans often remain—at least unless the borrower meets the strict discharge requirements.

Chapter 7 vs. Chapter 13: will either one clear student loans?

Chapter 7 usually focuses on wiping out qualifying unsecured debts. For student loans, discharge usually is still not automatic, and you typically must go through the special student-loan discharge process if you want them removed.

Chapter 13 is a repayment plan over a period of time. Chapter 13 can sometimes help you manage monthly payments, catch up on certain debts, or use the plan to address debts differently. However, student loans usually still require the same narrow showing for discharge—even in Chapter 13.

An attorney can explain which chapter (if any) best fits your overall debt picture—without assuming student loans will be cleared.

Common limits: what student loans usually do NOT do

It’s important to be honest with yourself about expectations. Most student loans survive bankruptcy for most people, even after a Chapter 7 or Chapter 13 case.

Some categories of debt also commonly survive bankruptcy (even when other debts don’t), including: most student loans, recent income taxes, child support/alimony, many court-ordered penalties, and debts tied to fraud. Outcomes depend on the individual case and the specific debt type.

If your goal is to reduce or pause payments, an attorney can also discuss other options that may work alongside or instead of bankruptcy.

What you can do next (practical steps, no pressure)

The most helpful next step is to talk with a licensed bankruptcy attorney who handles consumer bankruptcy in your area. Rules vary by state and judicial district, and student-loan discharge is fact-specific.

Use your first consultation to ask clear questions like: “Do I have a realistic chance of student-loan discharge in my district?” and “If not, what can bankruptcy or other options do for my monthly payments and collection threats?”

CleanSlate Match can connect you with a licensed bankruptcy attorney near you through a free matching service. This is not a law firm and we don’t file anything, but we can help you find someone to get a real, case-specific answer. Start here: Get matched.

- Ask about student-loan discharge standards in your district

- Ask what collections you can stop or slow while your case is pending

- Confirm the attorney is licensed in your state

Costs and expectations: what to ask before you hire

Many consumer bankruptcy attorneys charge a flat fee for a bankruptcy case. In addition, you typically pay court filing fees and a required credit-counseling fee (and possibly other small administrative fees). The exact total depends on the chapter, the complexity of your situation, and your district—so ranges are not quotes.

Don’t let anyone pressure you into a decision or promise a guaranteed outcome. Student-loan discharge is especially not something anyone can responsibly promise without reviewing your facts.

If you want to compare basics, learn more about Chapter 7 vs. Chapter 13 and how the process works in general at Guides for getting started. Then get matched to a licensed attorney for a calm, realistic case review: Get matched.

Usually student loans don’t get erased by bankruptcy automatically, but a licensed attorney can tell you what—if anything—might be possible in your district, and you can get matched for free.

Common questions

If I file Chapter 7, will my student loans be wiped out?

Usually, no. Student loans generally do not automatically discharge in Chapter 7. In limited cases, discharge may be possible under a special, strict standard, but it depends on your facts and your judicial district.

If I file Chapter 13, does that help my student loans get cleared?

Chapter 13 often helps with managing payments for other debts, but student-loan discharge is still typically difficult and usually not automatic. Your attorney can explain whether the student-loan discharge process applies to your situation and what alternative relief may be available.

Are there any student loans bankruptcy always clears?

No. Bankruptcy outcomes depend on the type of student loan and the facts of your case. Even then, student loans are commonly not discharged, and some categories of education debt may survive.

What if my main problem is that I can’t afford the monthly payment—can bankruptcy still help?

It can sometimes help with overall debt pressure, and the automatic stay that starts when a bankruptcy case is filed can pause many collections and legal actions for many debts. However, whether it pauses student-loan collection actions can vary by situation. A licensed attorney can explain what would happen in your case.

Does state or location matter for student-loan discharge?

Yes. Bankruptcy rules and how procedures are handled can vary by state and judicial district, and the details matter for student-loan discharge. Confirm the specifics with a licensed bankruptcy attorney in your area.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →