Guides

Does bankruptcy clear payday loans?

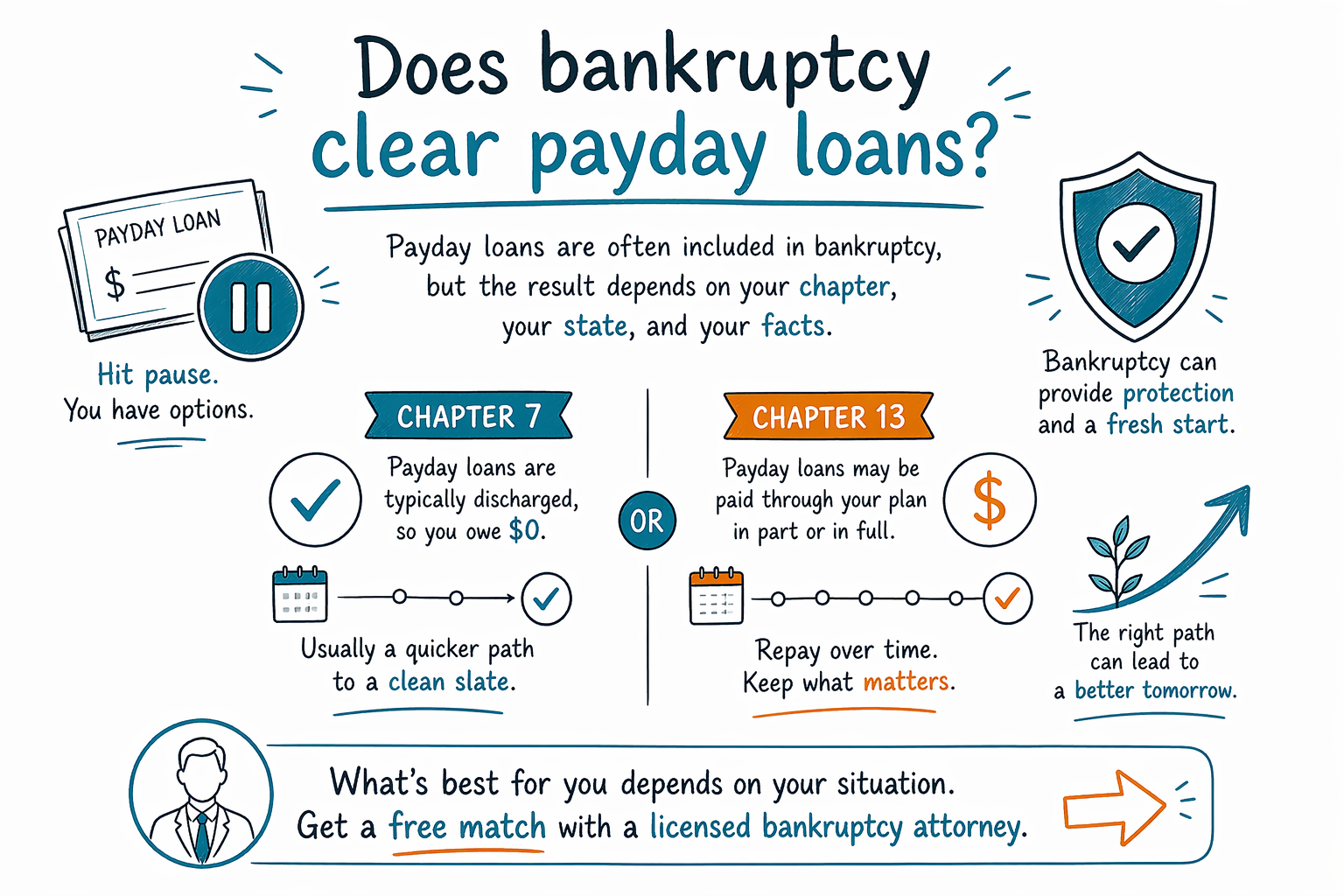

Usually, yes—payday loans can often be included in bankruptcy, but the exact result depends on your chapter, your state, and the facts of your case. Bankruptcy does not erase every debt, so a licensed bankruptcy attorney should review your situation.

Short answer: payday loans are often dischargeable

For many people, payday loans are treated like other unsecured debts, such as credit cards or medical bills. In a Chapter 7 case, they may be wiped out if the case qualifies and no special problem applies. In Chapter 13, they are usually handled through a repayment plan, and some or all of the balance may be paid over time.

That said, bankruptcy rules vary by state and judicial district, and the outcome depends on the full facts of your case. A lawyer in your area can tell you how local exemptions, filing practices, and timing rules may affect your payday loan debt.

If you want a plain-English overview of the two main consumer bankruptcy chapters, see Chapter 7 vs. Chapter 13.

When a payday loan may be harder to erase

A payday loan is not always simple. Problems can come up if the loan was very recent, if the lender claims fraud, or if you used a bank account in a way that led to an overdraft or other related debt. If you wrote a post-dated check or gave an authorization that has already triggered bank fees, those side issues may need separate review.

Bankruptcy also does not usually erase every type of debt. Common debts that may survive include most student loans, recent income taxes, child support and alimony, many court fines, and debts tied to fraud or certain wrongful conduct. Every case is different, so it is important to get specific advice.

What happens when you file

When a bankruptcy case is filed, the automatic stay usually starts right away. That can pause many collection actions, including calls, lawsuits, wage garnishment, and some bank collection activity.

This does not mean every problem stops in every case, and it does not mean the debt is already gone. It means you may get breathing room while the court case moves forward. If you are behind on rent, a mortgage, or a car payment too, ask a lawyer whether Chapter 7 or Chapter 13 may better fit your situation.

If you are still learning how bankruptcy works in general, you can start with our guides.

What to bring to a bankruptcy lawyer

A licensed bankruptcy attorney can usually help faster if you bring a simple list of your debts, the names of the lenders, and any letters or court papers you have received. You do not need to collect every financial detail before asking for help.

Do not send Social Security numbers, bank account numbers, credit card numbers, or full account balances through an online form unless a lawyer specifically asks for them in a secure way. CleanSlate Match only collects contact information and general intent, such as your state, preferred language, and a short description of the problem.

If you are ready, you can get matched with a licensed bankruptcy attorney near you. It is free for you.

What bankruptcy usually costs

Most consumer bankruptcy attorneys charge a flat fee, and you also pay the court filing fee plus a small required credit-counseling fee. The total cost depends on the chapter, how complicated the case is, and where you file.

As a general range, Chapter 7 cases are often less expensive than Chapter 13 cases, because Chapter 13 is usually more involved. But these are only rough ranges, not quotes. A local attorney can tell you the real cost for your district after looking at your situation. CleanSlate Match is free to use, and participating attorneys pay a flat fee to take part; you do not pay us.

Payday loans are often included in bankruptcy, but the result depends on your chapter, your state, and your facts—so the safest next step is a free match with a licensed bankruptcy attorney.

Common questions

Will a payday lender still be able to collect after I file bankruptcy?

Usually, the automatic stay pauses most collection once the case is filed, but not every action is the same in every case. A local bankruptcy lawyer can explain what should stop right away where you live.

Can bankruptcy remove payday loan debt if the loan is very recent?

Maybe, but recent loans can raise extra questions, especially if the lender claims fraud or if there were bank overdraft issues. A licensed attorney should review the timing and documents before you decide.

Is CleanSlate Match a law firm?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help connect people with a licensed bankruptcy attorney near them.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →