Guides

Bankruptcy And Your Bank Account

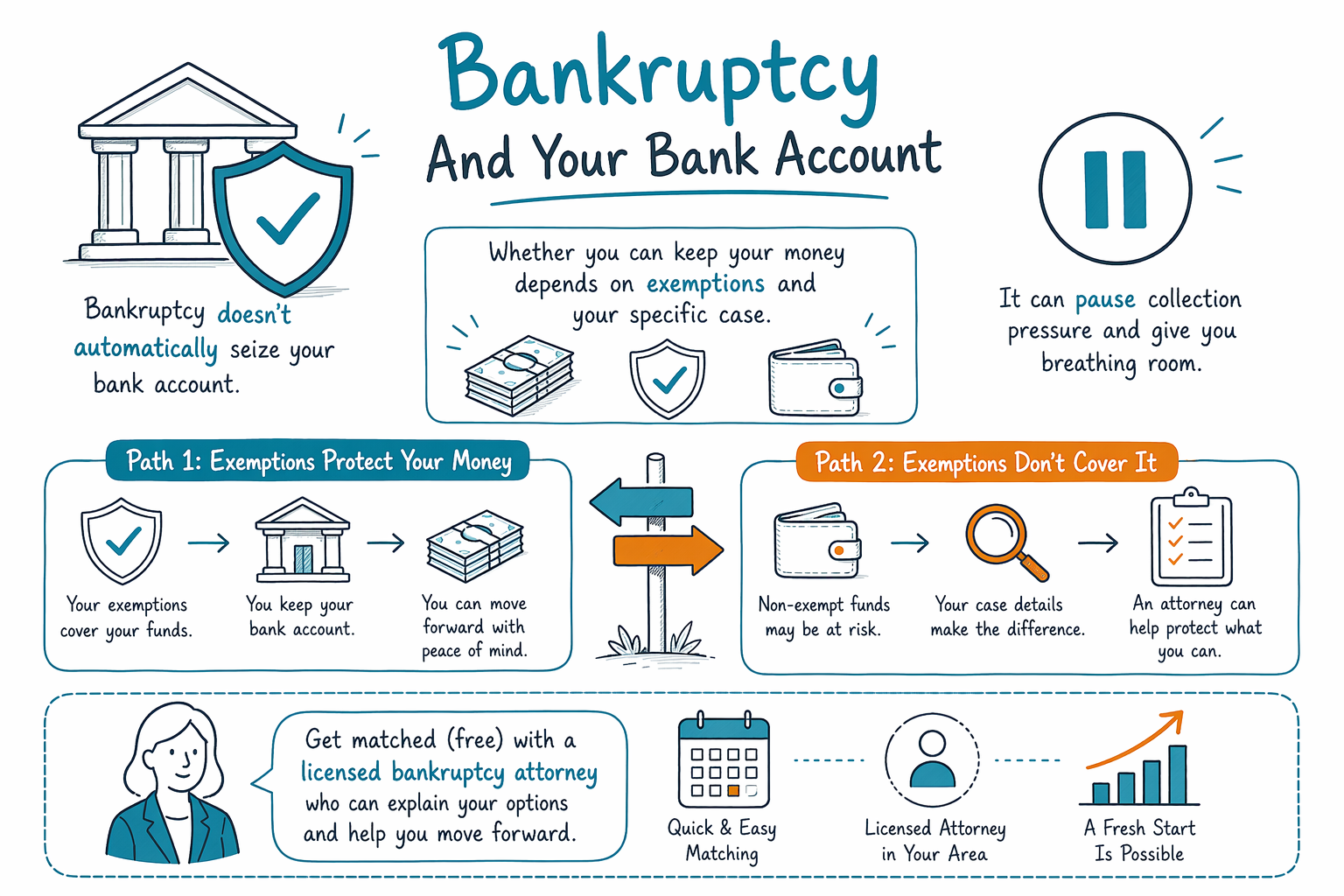

Worried about what bankruptcy will do to your bank account? This guide explains the general rules in plain language—what usually happens, what to watch for, and how to get matched with a licensed bankruptcy attorney near you.

Quick answer: will bankruptcy take your money from your bank account?

Often, bankruptcy does not automatically “empty” your bank account. When a case is filed, your situation is reviewed under bankruptcy exemptions, and many people are allowed to keep necessary funds—especially for basic living needs.

That said, outcomes vary a lot by state, the specific chapter (Chapter 7 vs. Chapter 13), and the facts of your case. Some cash may be treated differently depending on where it came from and whether it can be protected by exemptions.

Because rules change and can be technical, the safest next step is to talk with a licensed bankruptcy attorney in your area and confirm what would happen to your particular account.

- Bankruptcy usually isn’t an automatic “bank account sweep,” but details matter.

- Exemptions and chapter choice can determine whether funds are protected.

How a bankruptcy case affects your bank account (in general)

When you file, the goal is to handle your debts through the bankruptcy court process—not to punish you for having a bank account. The court and trustee may look at assets, including cash in accounts, using the exemption rules for your state.

In many cases, you can keep money that’s protected by exemptions. Attorneys often help people plan what to disclose and how to protect certain funds lawfully.

If you have money that isn’t protected (or it looks like money was moved around close to filing), the trustee may have questions and the outcome may be different. That is why it’s important to get individualized guidance before you make changes.

Chapter 7 vs. Chapter 13: what’s different for bank accounts?

Chapter 7 typically focuses on whether non-exempt assets exist. If certain assets (including unprotected cash) are available, a trustee may use them for the benefit of creditors. Many people still keep their essential property through exemptions.

Chapter 13 reorganizes your debts and creates a court-approved payment plan over time. Your income is involved in the plan, and your bank account activity can matter because the plan must be feasible. In return, Chapter 13 can sometimes help people catch up on certain debts (like some mortgage arrears) while making steady payments.

Which chapter is a better fit depends on your income, your debts, your state’s exemptions, and other details. Your attorney can explain what’s likely for your situation and what you’d need to document.

- Chapter 7 is often about non-exempt assets; Chapter 13 is about a repayment plan.

- Your state’s exemptions and your facts drive what you can keep.

Exemptions: the key concept that can protect money

Exemptions are rules that allow you to keep certain property or amounts of value, even in bankruptcy. Many states have specific exemption categories for money and certain necessities.

Because exemptions vary by state (and sometimes by district), the same amount of cash could be protected in one place and not in another. That’s why your attorney will review your state and the timing and source of the funds.

If you’re worried, that’s understandable. A licensed bankruptcy attorney can walk you through what exemptions may apply and what questions the court or trustee is likely to ask—so you’re not guessing.

Important limits: what bankruptcy usually cannot erase, and what to be careful with

Bankruptcy can help discharge many consumer debts, but it does not automatically wipe out everything. Common debts that often survive include: most student loans, recent income taxes, child support and alimony, most court fines, and debts tied to fraud or certain wrongdoing. Outcomes depend on the individual case.

For bank accounts specifically, avoid “last-minute” moves that could look like hiding assets. For example, transferring money to friends or family, moving funds to keep them out of reach, or spending large amounts right before filing can create serious problems.

If you’re unsure whether something is safe, ask a licensed attorney before you act. If you already filed or are about to file, tell your attorney about your accounts and recent deposits so they can advise you within the rules.

Get matched with a licensed bankruptcy attorney (free) and bring the right information

CleanSlate Match is a FREE matching service—not a law firm and not your lawyer. We help connect you with a licensed bankruptcy attorney near you who can review your situation and explain what bankruptcy can and cannot do for your accounts, debts, and goals.

To protect your privacy, we only collect contact and general intent information (like your name, phone number, optional email, your state, and your preferred language). We do not ask for your Social Security number, bank-account numbers, or account balances.

When you meet the attorney, be ready to discuss the type of debts you have and the basics of your financial situation. Your attorney will explain the chapter options, any likely impact on your accounts, court procedures, and the honest cost range for your area.

- CleanSlate Match is free for you and does not file bankruptcy.

- Rules vary by state and district—confirm details with a licensed bankruptcy attorney.

Bankruptcy doesn’t automatically seize your bank account, but whether you can keep your money depends on exemptions and your specific case—so get matched (free) with a licensed bankruptcy attorney to confirm what applies to you.

Common questions

Will I be able to keep money in my checking or savings account after I file?

Often, yes—if the funds are protected by your state’s bankruptcy exemptions and your case facts. The exact result depends on your state and chapter (Chapter 7 vs. Chapter 13), and whether the money is considered “exempt” or not.

Can I withdraw money or move it to another account right before filing?

Be very careful. Last-minute transfers or unusual spending can raise problems and may affect the case. The best approach is to discuss your accounts and recent activity with a licensed bankruptcy attorney before making changes.

Does Chapter 7 or Chapter 13 affect my bank account differently?

Yes. Chapter 7 generally focuses on whether there are non-exempt assets, while Chapter 13 focuses on your ability to make plan payments over time. Your attorney can explain what that likely means for your accounts in your state and district.

What debts will still be there after bankruptcy?

Many debts can be discharged, but some usually survive, including most student loans, certain recent income taxes, child support/alimony, many fines, and debts related to fraud or certain misconduct. Your attorney can review your specific debts and explain likely outcomes.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →