Guides

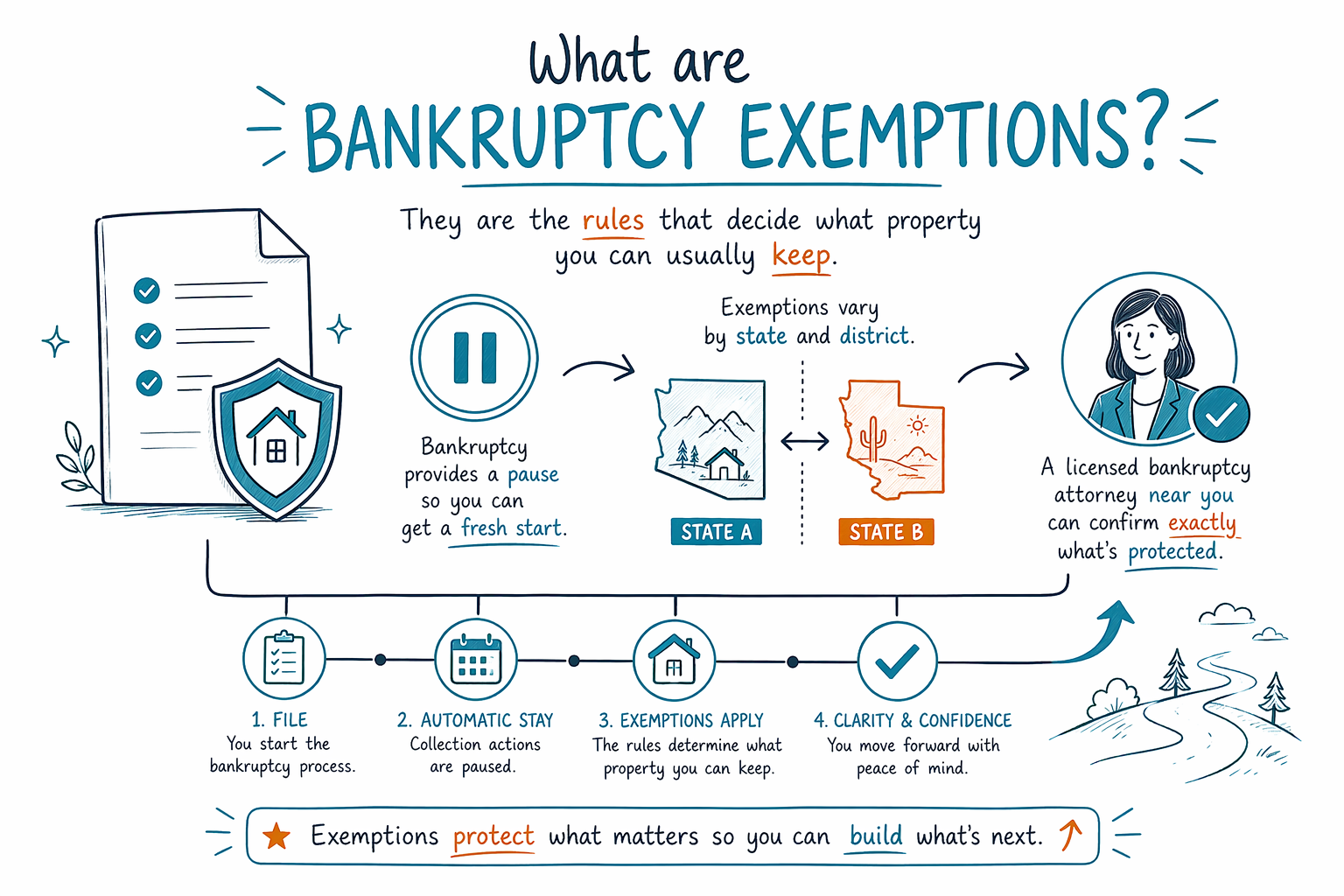

What are bankruptcy exemptions?

Bankruptcy exemptions are the legal rules that let you keep certain property while you handle debt. They can help you protect things like basic household items, a car, or home equity—depending on your state and case.

The direct answer: what bankruptcy exemptions do

Bankruptcy exemptions are the laws that decide what property you’re allowed to keep when you file a Chapter 7 or Chapter 13 bankruptcy case.

They don’t mean you get to keep everything. Instead, they set “protection limits” for certain categories of assets—like some household goods, clothing, tools you need for work, and sometimes home or car equity—so you’re not starting over completely empty-handed.

Because exemption rules are controlled by state law (and also by how your federal district handles certain issues), your exact list and limits can be different depending on where you live.

- Exemptions can help you keep property while the case proceeds

- What’s protected—and how much—depends on your state and type of bankruptcy

Exemptions vs. “debt forgiveness” (they are not the same thing)

A lot of people hear “bankruptcy” and think it automatically wipes out everything they owe. Bankruptcy exemptions are different: they’re about property protection, not about whether a specific debt is erased.

Some debts commonly survive bankruptcy. For example, many student loans, recent income taxes, child support or alimony, many court fines, and debts involving fraud often are not discharged. The result depends on the facts of your case and the specific laws that apply.

A licensed bankruptcy attorney can explain which of your debts may be dischargeable and, separately, which assets may be protected under your exemption rules.

- Exemptions protect property; discharge rules decide which debts may be wiped out

- Some debts usually survive—outcomes depend on your situation

How exemptions work in Chapter 7 and Chapter 13

In Chapter 7, the main idea is to liquidate non-exempt assets (if any) to pay what can be paid to creditors. Exemptions are crucial because they determine whether certain property is “taken” or stays with you.

In Chapter 13, exemptions can still matter, especially for what you keep and what value is treated in the repayment plan. Many people keep their home and car in Chapter 13 because they can catch up over time (if the plan and eligibility requirements are met).

Your best chapter is not always the one people assume. A careful attorney review is important because eligibility, payment capacity, and how exemptions apply can point to different strategies.

- Chapter 7: exemptions often determine what property stays vs. is liquidated

- Chapter 13: exemptions and the plan can help many people keep assets, but it must fit your case

What kinds of property exemptions may protect (examples)

Exemptions vary by state, but many states include protections for essentials. Common examples you might see include household items, clothing, basic furniture, and tools needed for work.

Many states also allow exemptions for certain equity in a home (or sometimes a homestead), and some protect equity in a car. Some exemptions are “wildcard” style, letting you choose categories up to a limit.

Even if something is generally exempt, details matter—like the type of asset, its value, and whether any liens exist. A lien doesn’t always disappear automatically just because the item is exempt; your attorney can explain what usually happens in your situation.

- Household goods and clothing are often exempt in some way

- Home or car equity may be protected, depending on your state’s limits

Why exemptions can feel confusing (and what to ask a lawyer)

Exemptions can be hard to understand because the rules are technical and vary widely. Some states require you to use state exemptions; others may offer options. Limits may change, and exemptions can have different rules for cash, retirement funds, tax refunds, and property with recent purchases.

You don’t need to figure it out alone. When you meet a licensed bankruptcy attorney, a good first consultation will cover both your exemption strategy and your debt discharge options.

Helpful questions to bring include:

1. Which exemption “set” applies in my state?

2. What property can I usually keep in a Chapter 7 or Chapter 13 case?

3. Are my debts likely to be discharged, and which ones usually do not?

4. Will any liens affect what happens to my home or car?

5. How do exemptions and the automatic stay work together in my situation?

Remember: general educational information is not legal advice, and rules vary by state and judicial district.

- Ask your attorney what your state allows you to keep—and what could be at risk

- Bring questions about both exemptions and the debts that may (or may not) be discharged

Costs: how much does exemption-focused bankruptcy help usually cost?

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The exact range depends on the chapter (Chapter 7 vs. Chapter 13), the complexity of the case, and your specific bankruptcy court.

As a rough guide, typical flat-fee ranges are often in the several-hundred to a few-thousand-dollar level, with the court filing fee commonly adding a few hundred dollars more. Still, the real number varies a lot by district and facts, so the only accurate price comes from a consultation with a licensed attorney.

CleanSlate Match is free for you to use. We help connect you with a licensed bankruptcy attorney near you who can review your situation and confirm bar membership before you choose anyone to work with.

- Expect a flat attorney fee plus court filing fee and required counseling fee (amount varies by chapter and complexity)

- CleanSlate Match is free to you—your consultation can confirm the attorney’s license and discuss next steps

Bankruptcy exemptions are the rules that decide what property you can usually keep, and they vary by state and district—so a licensed bankruptcy attorney near you can confirm exactly what’s protected in your case.

Common questions

Do bankruptcy exemptions let me keep my house or car?

Sometimes, depending on your state’s exemption limits, the value of the property, and whether there are liens. In many cases, exemptions and (for some people) a Chapter 13 plan can allow you to keep a home or car, but the details matter.

Will exemptions protect everything I own?

No. Exemptions protect specific types of property up to certain limits. If you have non-exempt assets or assets above the allowed value, they may be treated differently in the case.

If I use exemptions, will my debts definitely be wiped out?

Not necessarily. Exemptions are about keeping property, while discharge rules determine which debts may be erased. Some debts often survive bankruptcy, and outcomes depend on the facts and applicable law.

Do exemption rules change if I file Chapter 7 instead of Chapter 13?

You may still use exemptions in either chapter, but how they affect your case can differ. Chapter 7 focuses more on whether non-exempt assets get liquidated, while Chapter 13 focuses on a repayment plan and often on catching up certain debts.

Why does the state matter so much for exemptions?

Because exemption laws are mostly set at the state level and can also be affected by how courts in your district apply certain rules. A local licensed bankruptcy attorney can tell you exactly which exemption options and limits apply where you live.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →