Guides

Is debt consolidation better than bankruptcy?

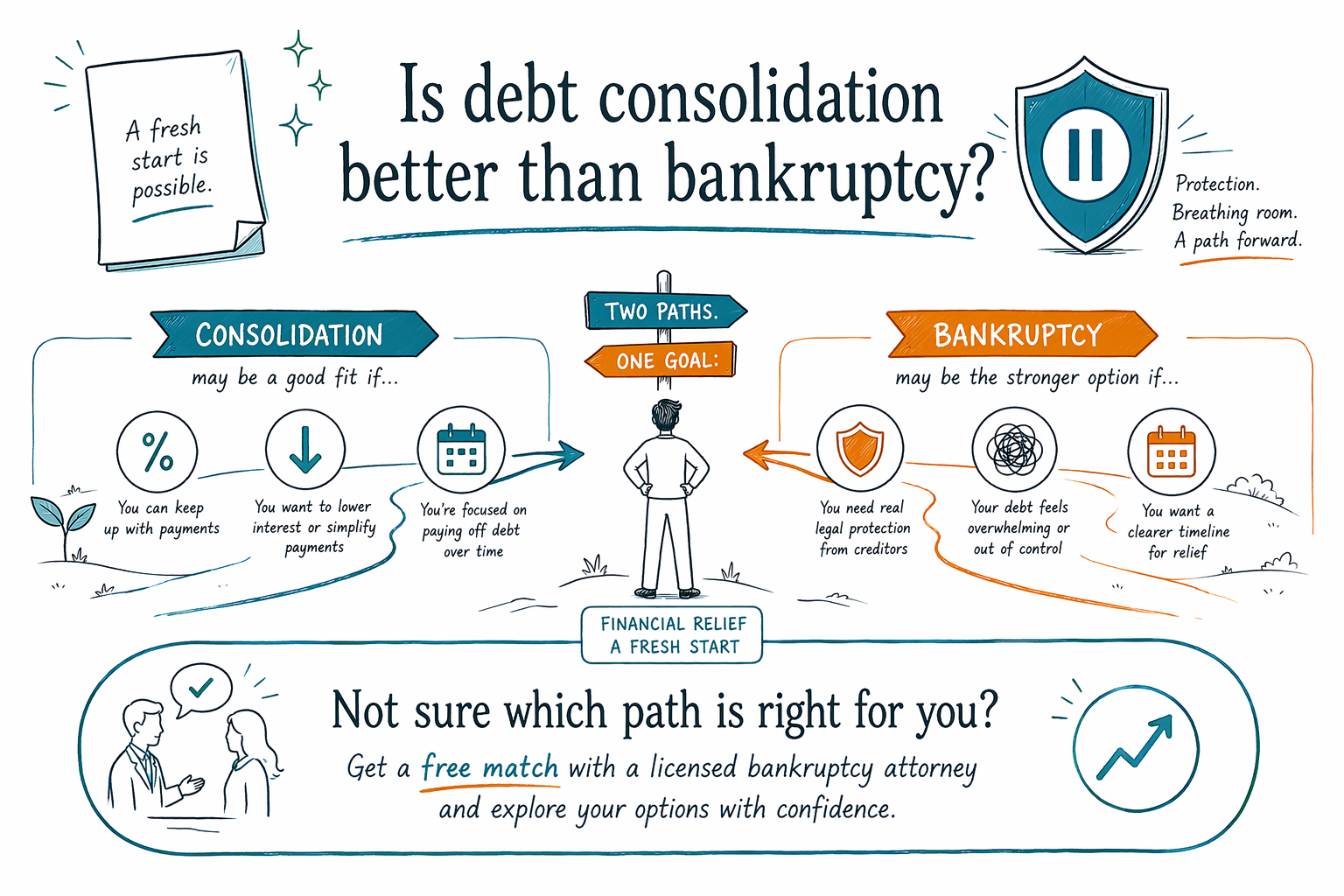

Debt consolidation can help some people, but it is not automatically “better” than bankruptcy. The right choice depends on your income, credit, the kind of debt you have, and whether you need fast protection from collections, garnishment, or foreclosure.

Short answer: it depends on your situation

If you still have enough income to make one new payment and qualify for a lower-rate loan or a repayment plan, debt consolidation may feel simpler. It can work best for people with mostly credit card debt and decent credit.

If you are behind on bills, being sued, facing wage garnishment, or trying to stop foreclosure, bankruptcy may offer stronger legal protection. In many cases, the automatic stay can pause most collection activity as soon as a bankruptcy case is filed.

Neither option is right for everyone. The safest next step is to compare both with a licensed bankruptcy attorney who knows the rules in your state and federal district.

What debt consolidation can do

Debt consolidation usually means combining several debts into one payment. That might happen through a personal loan, a balance transfer, or a debt-management program.

For the right person, consolidation can make bills easier to track and may lower interest. But it does not erase the debt. You still have to repay it, and if the new payment is too high, the plan can break down.

Consolidation also may not help if your credit is already damaged, your income is unstable, or creditors have already taken legal action. In those cases, it may not solve the core problem.

What bankruptcy can do

Bankruptcy is a legal process, not a loan. For some people, Chapter 7 may discharge qualifying unsecured debts. For others, Chapter 13 may create a court-approved repayment plan over time.

Bankruptcy can be especially helpful when you need immediate relief from lawsuits, garnishments, repossession, or foreclosure pressure. It can also help people who are too far behind to qualify for a realistic consolidation option.

That said, bankruptcy does not erase every debt. Some debts usually survive, such as most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud. Outcomes depend on the facts of the case.

How people often compare the two

A simple way to think about it is this: consolidation tries to reorganize debt you still plan to repay, while bankruptcy is a legal tool that may reduce, restructure, or discharge certain debts.

If you are current or only a little behind, consolidation may be worth exploring first. If you are overwhelmed, behind by months, or already being sued, bankruptcy may offer more protection and a clearer path forward.

Chapter 7 and Chapter 13 rules, the means test, and state exemptions vary by state and judicial district. A licensed bankruptcy attorney can explain which option fits your income, property, and debts.

What to check before you choose

Before you decide, look at a few practical questions:

- Can you realistically afford one new monthly payment?

- Are you behind on a mortgage, car loan, or taxes?

- Has a creditor already sued you or garnished your wages?

- Do you want to try to keep your home or car?

- Are you dealing mostly with unsecured debt, like cards or medical bills?

If you are unsure, you do not need to figure it out alone. You can learn more about bankruptcy basics, compare Chapter 7 and Chapter 13, or get matched with a licensed bankruptcy attorney near you.

Cost and next steps

CleanSlate Match is a FREE matching service, not a law firm and not your lawyer. We collect only contact details and general intent, such as your name, phone number, optional email, state, preferred language, and a brief description of your situation.

Most consumer bankruptcy attorneys charge a flat fee, plus the court filing fee and a small required credit-counseling fee. The total depends on the chapter, the complexity of the case, and the district. Those ranges are not quotes.

If you choose bankruptcy, it is wise to confirm the attorney is licensed and in good standing with the state bar where they practice. A free match can help you take that first step without pressure.

Consolidation helps some people, but if you need real legal protection or your debt is already out of control, bankruptcy may be the stronger option—so get a free match with a licensed bankruptcy attorney to compare your choices.

Common questions

Will debt consolidation stop collection calls or a lawsuit?

Not by itself. A new payment plan may reduce calls if creditors agree, but it does not create the same legal protection as a bankruptcy filing. If you already have a lawsuit, wage garnishment, or foreclosure risk, ask a licensed bankruptcy attorney about your options.

Is bankruptcy always worse for your credit than consolidation?

Not always. Both can affect credit, but the bigger issue is whether the option actually solves the debt problem. If consolidation fails and you miss payments, the damage can continue; if bankruptcy is the right fit, it may give you a real reset path over time.

Can bankruptcy erase all my debt?

No. Bankruptcy can help with many debts, but some usually survive, including most student loans, recent income taxes, child support and alimony, most court fines, and debts from fraud. A lawyer in your area can explain what may or may not be affected in your case.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →