Guides

How long does bankruptcy take?

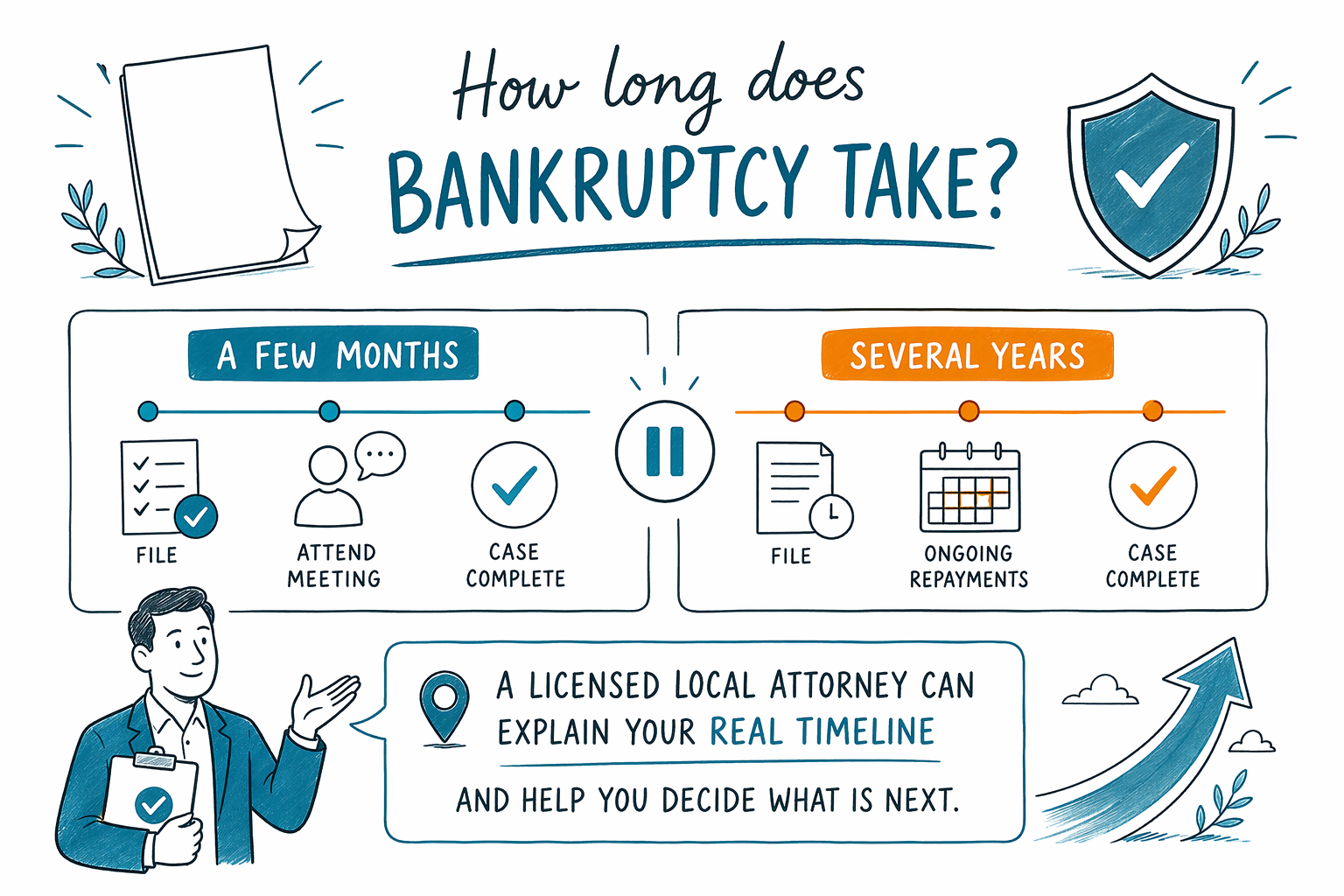

Bankruptcy can move faster than many people expect, but the exact timeline depends on the chapter, your court, and your case. The short answer: Chapter 7 is often over in a few months, while Chapter 13 usually lasts 3 to 5 years.

The short answer

If you are asking how long bankruptcy takes, the honest answer is: it depends on which kind you file and where you live. Bankruptcy rules, exemptions, and local court timing vary by state and federal district, so a licensed bankruptcy attorney in your area can tell you what is typical for your case.

In many consumer cases, Chapter 7 is the faster option. Chapter 13 takes longer because it is a repayment plan, not a quick case. In both chapters, some important steps happen before and after the filing, so the whole process is more than just one day in court.

CleanSlate Match is a free matching service, not a law firm and not your lawyer. We help people get connected with a licensed bankruptcy attorney near them so they can get clear, local guidance.

Typical timelines for Chapter 7 and Chapter 13

Most Chapter 7 cases take about 4 to 6 months from filing to discharge, if the case is straightforward. Some can move a little faster or slower depending on the court, missing paperwork, or questions from the trustee.

Chapter 13 usually takes 3 to 5 years because the court approves a repayment plan that lasts over time. Even after the plan is confirmed, you keep making payments until the plan ends.

A simple way to think about it is this: Chapter 7 is usually a shorter process, while Chapter 13 is a longer structured plan. A local attorney can help you compare which chapter may fit your situation.

What happens before and after filing

Before you can file, you usually need to complete a required credit-counseling course. After filing, the automatic stay usually starts right away. That means most collection calls, lawsuits, wage garnishments, and foreclosure actions must pause while the case moves forward.

Here is the basic sequence in plain English:

1. Gather the information your attorney needs.

2. Complete the required counseling course.

3. File the bankruptcy case.

4. The automatic stay starts in most cases.

5. Attend the meeting of creditors.

6. Complete any remaining court steps.

7. Receive a discharge if your case qualifies.

The meeting of creditors is often brief, but you still need to answer questions truthfully and attend when required. Your attorney can explain what documents to bring and what to expect.

What can make a bankruptcy case take longer

Some cases take longer because the paperwork is complicated, there is a house or car involved, there is a recent lawsuit or garnishment, or the trustee has follow-up questions. Chapter 13 can also take longer if the court requires changes to the repayment plan.

Timing can also be affected by local court backlogs, state exemption rules, and whether you need to respond to objections. If you are trying to stop foreclosure or wage garnishment, speaking with a lawyer quickly matters because filing at the right time can be important.

A good bankruptcy attorney will not promise a finish date they cannot control. They should explain the usual timeline in your district and what might slow your case down.

What bankruptcy can and cannot do

Bankruptcy can give many people a real fresh start, but it does not erase every debt. Some debts usually survive, including most student loans, recent income taxes, child support and alimony, many court fines, and debts tied to fraud. Results depend on the facts of your case and the law that applies where you file.

It can also help with urgent problems. In many cases, the automatic stay can stop most collections as soon as the case is filed, and many people are able to keep a home or car through exemptions or a Chapter 13 plan. But not every home, car, or debt is protected the same way.

That is why local legal advice matters. Bankruptcy law changes by state and district, and a licensed attorney can tell you what is realistic in your situation.

How to move forward without doing it alone

If you feel overwhelmed, the next best step is usually a short conversation with a licensed bankruptcy attorney near you. They can help you understand whether Chapter 7 or Chapter 13 may fit, how long the process may take in your court, and what documents you should gather.

A consumer bankruptcy lawyer usually charges a flat fee, plus the court filing fee and a small required credit-counseling fee. The total can vary by chapter, case complexity, and district, so any range is not a quote.

If you want a calm place to start, you can use our free matching service to share your name, phone number, optional email, state, general situation, and preferred language. We do not ask for Social Security numbers, bank numbers, or account details.

Bankruptcy can take a few months or several years, but a licensed local attorney can explain your real timeline and help you decide what is next.

Common questions

Can bankruptcy stop a wage garnishment right away?

Often, yes: the automatic stay usually starts when the case is filed and can pause most wage garnishments. There are exceptions, so a licensed attorney in your area should confirm how it works in your state and district.

Will I lose my house if I file bankruptcy?

Not always. Many people keep their home, especially if exemptions or a Chapter 13 plan protect the property, but the outcome depends on your mortgage, equity, and local law. A lawyer can explain the risks before you file.

Does Chapter 7 finish faster than Chapter 13?

Usually yes. Chapter 7 is often completed in about 4 to 6 months, while Chapter 13 generally lasts 3 to 5 years because it is a repayment plan.

What should I bring when I talk to a bankruptcy lawyer?

Bring a general list of your debts, a list of your monthly bills, and any court papers, foreclosure notices, or garnishment notices you have received. You do not need to share bank logins or full account numbers with CleanSlate Match.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →