Guides

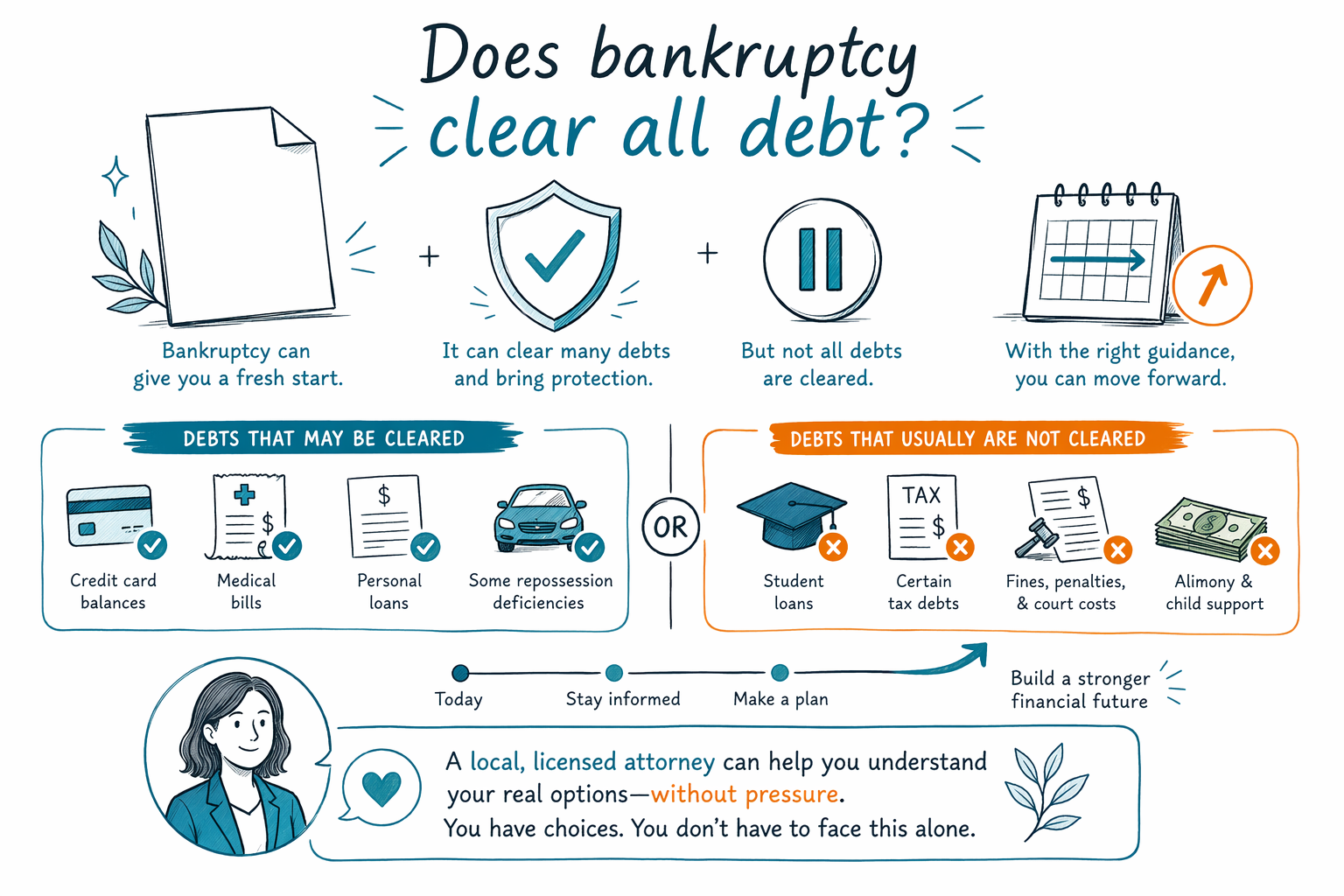

Does bankruptcy clear all debt?

No — bankruptcy does not clear every debt. But for many people, it can still provide real relief from credit cards, medical bills, and collection pressure, and a licensed bankruptcy attorney can explain what may or may not be discharged in your case.

The short answer

Bankruptcy can clear many common unsecured debts, but it usually does not erase everything. What is dischargeable depends on the chapter filed, your state, your district, and the facts of your case.

A good first step is to speak with a licensed bankruptcy attorney near you. CleanSlate Match is a free matching service, not a law firm and not your lawyer, and we do not file bankruptcy.

If you want a broader overview first, you can read our bankruptcy guides or compare the different chapters.

Debts bankruptcy often helps with

Many people file because they are struggling with unsecured debt. That usually includes things like:

- Credit cards

- Medical bills

- Personal loans

- Old utility bills in some cases

- Some lawsuit judgments

Bankruptcy can also trigger the automatic stay, which usually pauses most collection activity as soon as the case is filed. That may stop many calls, letters, lawsuits, garnishments, and foreclosure activity right away, though the details depend on the situation and the court.

Debts that often survive bankruptcy

Some debts are commonly harder to discharge, and some usually survive bankruptcy unless a court makes a specific ruling. Examples often include:

- Most student loans

- Recent income taxes

- Child support and alimony

- Most court fines and criminal restitution

- Debts from fraud or some intentional wrongdoing

This is one reason bankruptcy should be reviewed case by case. A licensed attorney can explain which debts may be discharged, which may not, and whether Chapter 7 or Chapter 13 may fit better.

Chapter 7 and Chapter 13 are not the same

Chapter 7 and Chapter 13 work differently. Chapter 7 is often called a liquidation case, but many people keep most or all of their property because exemptions may protect it. Chapter 13 uses a payment plan and can help people catch up on a mortgage, car loan, or other overdue debt over time.

Whether you qualify for Chapter 7 depends in part on the means test, which looks at income and certain other factors. Rules vary by state and federal district, and they change over time, so the safest answer always comes from a local bankruptcy lawyer who is licensed where you live.

What bankruptcy can and cannot do

Bankruptcy can be a fresh start, but it is not a magic eraser. It may reduce or discharge many debts, stop collection pressure, and give you a path forward.

It cannot promise to eliminate every debt, fix every money problem, or protect every asset in every case. It also may not remove debts that are tied to fraud, support, or certain taxes.

If you are worried about your home, wages, or car, talk with a lawyer quickly. Some people can keep a home through exemptions or a Chapter 13 plan, but the result depends on the facts and local rules.

What to do next if you are overwhelmed

You do not need to figure this out alone. A free match can connect you with a licensed bankruptcy attorney near you who can review your situation and explain your options in plain English.

- Share your contact information and general situation only.

- Tell us your state and preferred language.

- Get connected with a local attorney for a consultation.

You do not need to send a Social Security number, bank account number, credit card number, or account balances to use CleanSlate Match.

Bankruptcy can clear many debts, but not all of them, and a local licensed attorney can help you understand your real options without pressure.

Common questions

Will bankruptcy erase my credit cards and medical bills?

Often, yes, those are the kinds of debts bankruptcy may help with. But the result depends on the chapter, your case, and local rules, so a licensed bankruptcy attorney should confirm it for you.

What debts do not usually go away?

Most student loans, recent income taxes, child support, alimony, many court fines, and debts from fraud often survive bankruptcy. There are exceptions and special rules, so ask a local attorney.

Can bankruptcy stop wage garnishment or foreclosure?

Often it can pause many collection actions through the automatic stay when the case is filed. Whether it fully stops a garnishment or foreclosure long term depends on the case and the chapter filed.

Is CleanSlate Match a law firm?

No. CleanSlate Match is a free matching service, not a law firm and not your lawyer. We connect people with licensed bankruptcy attorneys near them.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →