Guides

Can i file bankruptcy without a lawyer?

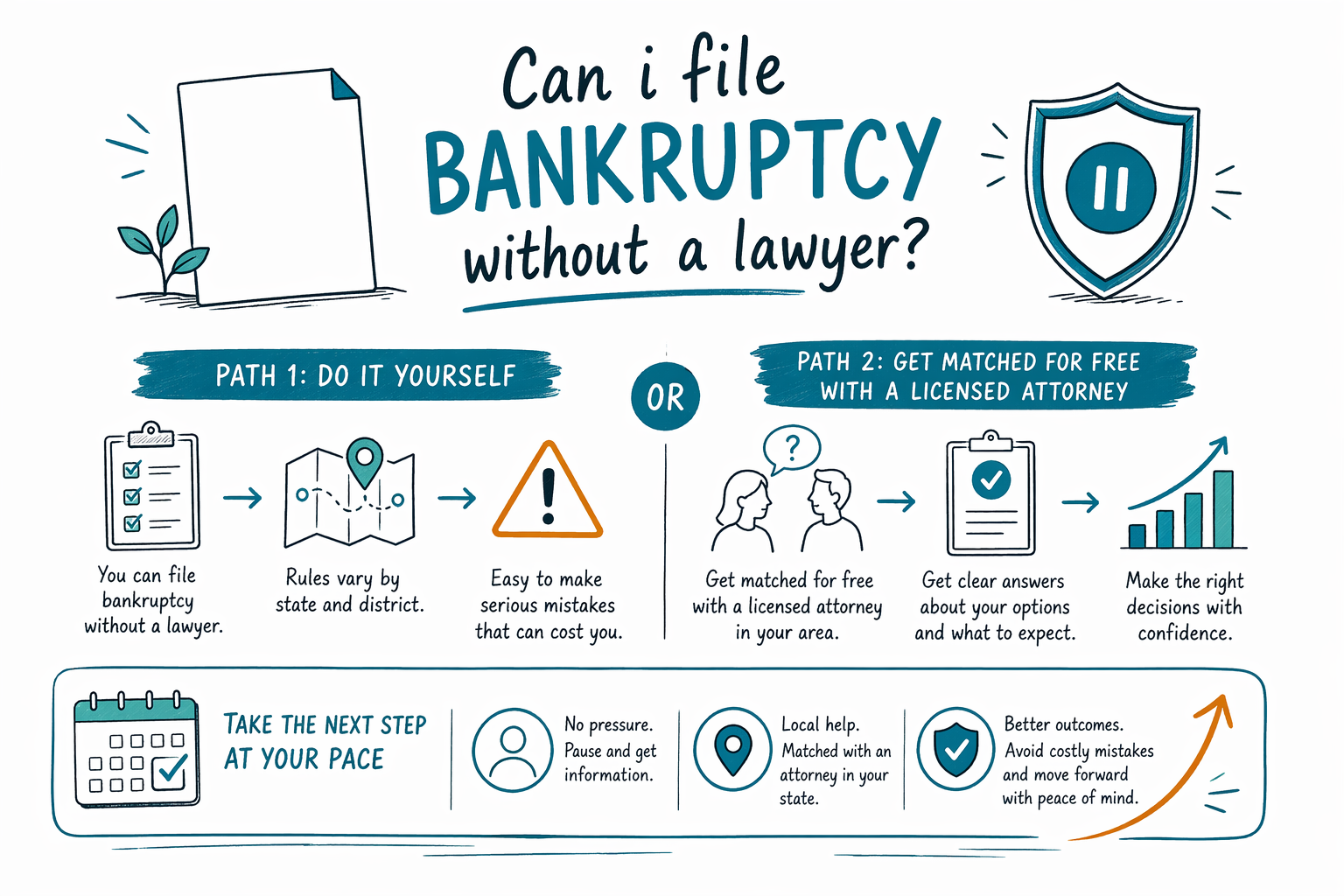

Yes, you can file bankruptcy without a lawyer in the US, but it’s not the easiest path. Bankruptcy forms, deadlines, and eligibility rules can be very specific, so most people get real help to avoid costly mistakes.

Short answer: you can, but it’s usually risky to go it alone

In many consumer cases, people are allowed to file bankruptcy without an attorney. But “allowed” doesn’t always mean “wise,” because one missed deadline or the wrong paperwork can hurt your chances or create problems later.

If you’re facing wage garnishment, foreclosure, or a lawsuit, the situation often changes quickly. A licensed bankruptcy attorney can help you understand which chapter fits your situation and what to do next.

CleanSlate Match is a FREE service that matches you with a licensed bankruptcy attorney near you. We’re not a law firm and we can’t file paperwork for you or promise outcomes.

- You can file pro se (without a lawyer), but mistakes can be expensive

- Attorney guidance is especially helpful with foreclosure, garnishments, or complex debts

Why people choose a lawyer (even if they think they can “do it themselves”)

Bankruptcy isn’t just filling out forms. It involves eligibility rules, correct schedules (listing creditors and debts), documents showing income and expenses, and sometimes special rules about what debts can be wiped out.

Chapter 7 and Chapter 13 work differently, and the “best” choice depends on your income, debts, and goals. For example, Chapter 13 can help some people catch up on a mortgage or stop certain collection actions by using a repayment plan.

Even when you qualify, the process can feel overwhelming—especially if you’re new to the US or English isn’t your first language. A lawyer can explain the process clearly and help you respond to court requests.

- Correct paperwork and deadlines matter a lot in bankruptcy court

- Different chapters fit different goals (like stopping foreclosure or reorganizing debts)

Chapter 7 vs. Chapter 13: a quick, practical difference

Chapter 7 is often called “liquidation,” though for many people it’s best described as a process to discharge eligible unsecured debts (like many credit card balances and many medical bills). It usually involves the court reviewing your case and, for many filers, you may not have to make ongoing plan payments.

Chapter 13 is a reorganization with a court-approved repayment plan. Instead of wiping out eligible unsecured debts all at once, it typically spreads payments over a period of time. It can be helpful if you want to keep property and catch up on certain debts through the plan.

Which one fits you depends on your situation. A licensed attorney in your area can explain how the rules apply where you live—remember, rules vary by state and judicial district.

- Chapter 7 may discharge many eligible unsecured debts

- Chapter 13 uses a repayment plan and can help with certain past-due amounts

What bankruptcy can—and usually cannot—erase

Bankruptcy may discharge (wipe out) many kinds of debts, but not everything. Some debts often survive bankruptcy, including most student loans, recent income taxes, child support and alimony, many court fines, and debts from fraud or certain misconduct.

Also, outcomes depend on the details of your case. Exemptions (what property you can keep) and which debts are dischargeable can vary by state and the local bankruptcy court.

The good news: once you file, the automatic stay generally pauses many collection actions—like most collection calls, many lawsuits, wage garnishment, and foreclosure efforts—while your case is pending. But the stay has limits and exceptions, so it’s still important to discuss your specific situation with a licensed bankruptcy attorney.

- Many unsecured debts may be dischargeable, but not all debts go away

- The automatic stay can pause many collections after you file

If you go without a lawyer (pro se), know the main hurdles

People who file without an attorney must still follow the same basic bankruptcy rules as everyone else. That includes meeting filing requirements, using correct forms, and complying with court procedures.

Here are practical issues that commonly trip people up:

1. Choosing the wrong chapter for their goals (or not qualifying for the intended chapter)

1. Missing documentation or making errors in schedules

1. Not understanding deadlines for required courses or paperwork

1. Not responding correctly to creditor filings or court notices

Because rules vary by state and judicial district—and bankruptcy law changes—getting local guidance is often the difference between a smooth filing and avoidable problems.

- Pro se requires strict compliance with forms, deadlines, and local court procedures

- Local rules vary, so “what worked for someone else” may not work for you

Cost and next step: get matched for free with a licensed attorney

Many consumer bankruptcy attorneys charge a flat fee for the legal work, plus the court filing fee and a small required credit-counseling fee. Typical total costs can vary, often ranging roughly from a few hundred dollars to several thousand dollars depending on the chapter (Chapter 7 vs. Chapter 13), the complexity of the case, and the district.

What can raise the cost includes more complicated income situations, multiple assets, prior filings, contested issues, or the need for additional plan work in Chapter 13. Ranges are not guarantees or quotes, and exact pricing depends on the attorney’s review of your case.

If you’re ready, you can get matched for FREE with a licensed bankruptcy attorney near you. This is just a starting point for a conversation—confirm the lawyer is licensed in your state before you proceed. If you want to learn more, browse guides and chapter basics to understand the differences first.

- Flat-fee legal services are common, plus court fees and a small required counseling fee

- Get matched FREE with a licensed attorney and confirm licensing before hiring

You can file bankruptcy without a lawyer, but it’s easy to make serious mistakes—rules vary by state and district, so consider getting matched for free with a licensed attorney who can explain your best next step.

Common questions

If I file without a lawyer, will my case definitely be denied?

Not necessarily. People do file pro se successfully sometimes. But denial or complications can happen if paperwork, eligibility, or deadlines are missed—so it’s worth getting local guidance from a licensed bankruptcy attorney.

Can I stop foreclosure or wage garnishment if I don’t have a lawyer?

Often, the automatic stay begins when you file and can pause many collections, including many foreclosure actions and wage garnishments. However, the stay has exceptions, and the details depend on your case, your chapter, and local rules.

What debts survive bankruptcy?

Many debts can be discharged, but some often survive, including most student loans, recent income taxes, child support and alimony, many fines/penalties, and debts tied to fraud or certain wrongdoing. Your situation matters, and a licensed attorney can explain what likely applies to you.

How do I find a bankruptcy lawyer near me if I’m overwhelmed?

You can use [get matched](/get-matched/) for FREE. We’ll connect you with a licensed bankruptcy attorney in your area to discuss your options. CleanSlate Match is not a law firm and can’t file for you—your consultation with the attorney is where legal advice happens.

Related help

A plain-language comparison of the two main consumer bankruptcies, when each makes sense, and how a lawyer helps you decide.

Open → What Debt Bankruptcy Can and Can't EraseWhich debts bankruptcy wipes out, which ones survive (like most student loans and child support), and why it matters.

Open → Will I Lose My House or Car in Bankruptcy?How exemptions and the two chapters affect your home and car — and why many people keep both.

Open →